National Security Reveals Challenges to Japan’s Fiscal Policy

December 12, 2022

R-2022-049E

Prime Minister Kishida has announced plans to raise defense spending to a level similar to the target for NATO member states, but creative financing solutions must be found in the light of Japan’s fiscal constraints. Motohiro Sato outlines what Japan must do to fiscally meet the challenges of rising geopolitical tensions.

* * *

Against the backdrop of growing concerns over national security, the just over ¥110 trillion yen in budget requests for fiscal 2023 included a record ¥5.6 trillion yen in defense expenditures. The requests also included 100 national defense items for which budget amounts were not specified, such as standoff missiles that can be launched from outside an enemy’s anti-aircraft missile range (Nikkei, August 31, 2022). Because the North Atlantic Treaty Organization (NATO) has a target for member states to allocate 2% of GDP to defense spending, many in Japan have been calling for similar levels of spending. Prime Minister Fumio Kishida has noted that he would consider all options in fundamentally strengthening the nation’s defense capabilities over the next five years, including acquiring “counterstrike capabilities” against the missile launch sites of adversarial countries.

The need to boost defense spending is understandable, but Japan’s public finances are severely strained. The ratio of national and local government debt to gross domestic product exceeds 250%—the highest of any developed country. And in addition to such immediate crises as the COVID-19 pandemic and rising prices, Japan confronts serious long-term challenges associated with an aging and dwindling population.

Despite the fiscal constraints, the government plans to move ahead to reinforce its defense capabilities, examining exactly what it needs, how much such upgrades will cost, and the means by which to secure necessary funds. It has established a new panel of private-sector experts in the Cabinet Secretariat to explore issues in increasing defense spending. The panel is expected to discuss concrete funding sources as the government draws up a new national security strategy and fiscal 2023 budget by the yearend.

The importance of fiscal consolidation in strengthening Japan’s defense capabilities has been discussed by Kazumasa Oguro in an article on this site (Japanese only). Here, I will therefore outline the economic and fiscal challenges revealed by the request for higher defense expenditures. I will focus on three topics, namely, how to balance a stronger defense and economic growth; the invisible debt that results from paying off defense bills in “installments”; and the difficulty of ascertaining a full view of defense spending due to the siloing of defense-related expenditures among various ministries and agencies. Another important issue is raising awareness among Japanese taxpayers of their role in securing the financial resources for an expanded defense budget.

Can Defense Spending Boost Economic Growth?

Enhancing national security must be balanced not just with restoring fiscal soundness but also with encouraging business activity. Some have advocated the issuance of “defense bonds” to pay for greater security—just as construction bonds are issued to help build roads, bridges, and other infrastructure—and protect our country for future generations. In terms of service life, though, there is a great difference between social infrastructure and such defense equipment as combat aircraft and naval vessels. And placing national defense on a par with public works might invite military Keynesianism, that is, the use of large-scale public expenditures on weapons and munitions—or even the waging of war itself—to boost demand, just as governments now turn to public works projects to generate jobs and fuel economic growth. Once this becomes the norm, reining in the defense budget could impact negatively on growth. Experience has shown that phasing out any large-scale outlays, whether they be to bolster national resilience after a major disaster or to provide pandemic relief for smaller business, can be very difficult.

To ensure longer-term economic benefits from higher defense spending, we should focus on dual-use of technology with both military and civilian applications—perhaps the best-known examples of such technology being the Internet and the Global Positioning System (GPS). This will not only trigger higher demand but could also lead to improved productivity among suppliers and potentially promote longer-term growth. This will have a positive impact on government finances and, in turn, contribute to the sustainability of national defense. Japan’s defense white paper (Defense of Japan 2019) cites an example of how the Ministry of Defense (MOD) has encouraged the use of defense-related aircraft technology in the civilian sector. The reverse is also possible if an environment can be created where businesses with advanced, non-military technologies are able to develop new defense applications, as proposed by Keidanren (Japan Business Federation). The distinction between defense and civilian technologies is becoming blurred, especially in the space sector. Even the Science Council of Japan, which had steadfastly rejected research for military purposes, recently concluded that it has become difficult to clearly differentiate between military and civilian applications.

Multiyear Payments for Defense Equipment

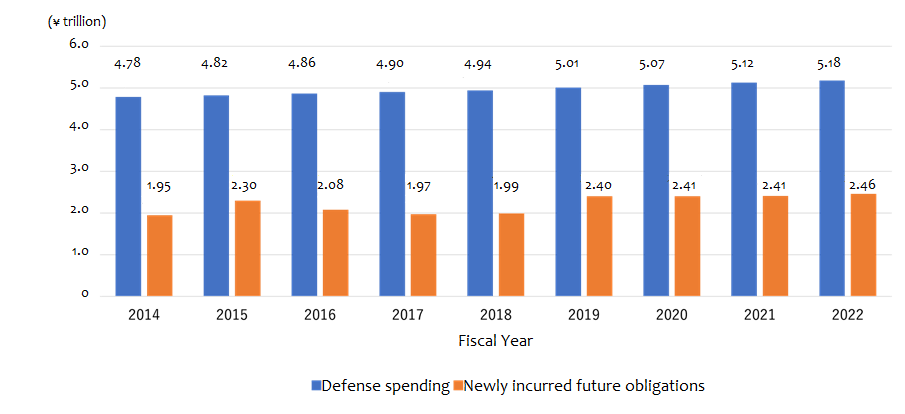

Although the national budget operates on a single-year basis in Japan, this principle does not apply to defense expenditures, and that is why it can be hard to get a full picture of how much the country spends on defense. After an order is placed for defense equipment (and itemized in that year’s budget), it is quite common for many years to pass before delivery (and full payment). For this reason, defense spending is granted an exception to the single-year rule, in effect allowing for payment in installments. But this gives rise to discrepancies between the amount budgeted as defense expenditures and total expenses paid to contractors, since the former will include not only the amount of the contract for the year in which an order is placed (any unpaid portion being carried over to the following year) but also the amount paid in subsequent years.

For example, the fiscal 2022 budget earmarks ¥5.4 trillion for defense, but this includes slightly over ¥2.9 trillion in newly contracted costs that will not be paid for during the fiscal year. In one respect, the figure represents debt that the government will need to “pay off” in future years. Unless contracts are cancelled due to nonperformance, this is a massive obligation that could shackle future defense allocations, making it difficult to accommodate new security-related budgetary requests. With a substantial share of the budget going to “repayment,” though, pressure for even bigger allocations will likely increase. The practice of such deferred payments, in short, creates “invisible debt.” In fiscal 2022, the total amount “owed” from previous years is ¥5.33 trillion, including ¥2.46 trillion in newly incurred obligations. This figure is in excess of the total fiscal 2022 defense budget, which, according to the Defense of Japan 2022, stands at ¥5.19 trillion (not including host-nation support for the US forces in Japan).

Payment over multiple years is not limited to defense expenditures; public work projects to build social infrastructure, for example, are also often itemized one year and completed over the course of several years—particularly in the face of the current labor shortage. And similar payment obligations are incurred under private finance initiatives, whereby the government enters into long-term contracts with private companies to build or manage public facilities.[1] There may be aspects of multiyear arrangements that help lower overall project costs, but such benefits are minimal for defense contracts, given the significantly higher price tags for military equipment.[2]

Defense-Related Spending and New Future Obligations

Note: Expenditures related to the Midterm Defense Program

Source: Ministry of Finance

Visualizing Payment Obligations

How can the dilemma posed by such “invisible debt” be resolved? One way is to make it more visible. A helpful guide in this regard is the future burden ratio, used to measure the fiscal health of local governments, with public debt being expressed as a share of each government’s fiscal scale. What is notable about this ratio is that debt includes not only the bonds issued by local governments but also any public works financed with debt instruments. The same can surely be done with defense-related spending to give a more accurate picture of its share in the national budget.

Specifically, this would involve including as expenditures not just the defense-related items to be paid for during the fiscal year but also any new contracts to be entered into that year. At the same time, the obligations for which payment is due in later years would be itemized as revenues. The new contracts totaling ¥2.9 trillion in the fiscal 2022 budget are not bonds, but they can be thought of as the principal and interest that must be repaid. Doing so would make people more aware of this “invisible debt” and view them more like construction bonds and deficit-financing bonds. Later, the amount disbursed as repayment should be itemized as expenditures in that year’s budget. The question this raises is whether financial resources will be available to cover these payments.

The portion of the ¥5.4 trillion fiscal 2022 defense budget that will be expended during the year can be thought of as repayment of principal and interest. The ¥2.9 trillion that will be paid in later years, meanwhile, represents new “debt,” [3] although it will be offset as expenditures in future budgets and thus does not result in additional defense spending. But how repayment of this new debt is itemized is a decision we can make today; in other words, the repayment of liabilities should be recognized as future costs, requiring thought on funding sources. Similar measures can be applied to public works and private finance initiatives, potentially prompting reconsideration of the cash-based budget system currently used in Japan.

Overcoming Budget Sectionalism

Each item in Japan’s budget is allocated to a specific ministry or agency, and policy initiatives undertaken across multiple organs, such as childcare assistance or regional revitalization, require that each ministry create and execute its own budget. For childcare assistance, for instance, cash allowances are implemented by the Cabinet Office; benefits in kind and nursery schools are under the jurisdiction of the Ministry of Health, Labor, and Welfare (MHLW); and kindergartens are administered by the Ministry of Education, Culture, Sports, Science, and Technology (MEXT). When it comes to local revitalization, subsidies are handled by the Cabinet Office; roads, bridges, and other infrastructure improvements are undertaken by the Ministry of Land, Infrastructure, Transport, and Tourism (MLIT), and the Ministry of Agriculture, Forestry, and Fisheries (MAFF) administers projects that encourage agricultural producers to expand into food processing and retailing in an attempt add value to their products—an economic strategy known as senary industrialization.

This compartmentalization not only obscures the overall picture of a policy area but also invites complications when choices must be made, such as between in kind and cash childcare benefits, and hampers the streamlining of overlapping projects (where the same organization may receive subsidies from multiple ministries or agencies).

Such opacity characterizes defense spending as well. The Liberal Democratic Party has resolved to achieve a budget level necessary to fundamentally strengthen the nation’s defense capabilities over the next five years in line with NATO’s 2% target, as described above. But “defense spending” is not simply the amount earmarked for the MOD. Using NATO’s criteria, it may include the budget for the Japan Coast Guard, which is under the jurisdiction of the MLIT—in which case Japan’s defense spending as a share of GDP would rise to 1.24%. Expanded applications of dual-use technologies may result in some research funded by MEXT also being classified as defense-related. And the same would apply to MLIT projects for tunnels and basements of public buildings that are designed with national security in mind and could serve as shelters during wartime.

Cyber defense is another area where the civilian-military distinction can be blurred, as budgets are allocated not only to the MOD but also to the Cabinet Office and the Ministry of Internal Affairs and Communications (MIC). There may be cases where civilian cybersecurity technologies are needed to meet national security needs or where defense equipment is used to protect critical private infrastructure (Nikkei, September 1, 2022). The government also plans to study the feasibility of including space-related expenditures that are not allocated to the MOD as defense-related spending (Yomiuri Shimbun, September 10, 2022). The challenge of accurately ascertaining the size of Japan’s defense budget is not just a matter of defining what “defense spending” means, moreover. It raises questions about the very nature of the sectionalized budget-making process. This, as I have described above, hampers efforts to weigh policy options and assess outcomes. Greater flexibility in budget formulation may be called for so that allocations can be made by policy area, not just by ministry.

Financing a More Robust Defense

If defense spending is to be expanded in the coming years, then there is a need to secure a reliable source of funding. Given Japan’s already massive public debt, issuing additional bonds—which must eventually be repaid with interest—could seriously jeopardize fiscal sustainability. The only other option, then, is to raise taxes. Any new levy would have to be characterized by fairness for all taxpayers, though, and stringent mechanisms must be in place to prevent defense spending from spiraling out of control. One solution may be to impose a limited-term surtax on the amount paid in income tax, modeled on the special income tax created in the wake of the March 2011 Great East Japan Earthquake. In addition to issuing reconstruction bonds, the government created a 2.1% surtax, levied on the amount paid in income tax; implemented in 2013, the special tax is scheduled to be abolished after a period of 25 years.

The globalization and digitization of the economy have widened income disparities, so it is now more important than ever for our tax system to maintain the ability-to-pay principle, especially in the case of income tax. Given that the purpose of national security is to protect people’s lives and property, then it stands to reason that the wealthy—who would benefit the most from having their extensive property and assets protected—should pay more. A surtax on the amount paid in income tax would thus be in keeping with the benefit principle, that is, that taxpayers should be charged according to the benefits they receive.[4] Income tax revenues in fiscal 2022 are expected to reach ¥20 trillion, so a 5% surtax would generate an additional ¥1 trillion. (If we are serious about achieving truly equitable burden sharing, of course, we would also need to address issues in the income tax system itself, such as deductions and taxes on financial income.) The surtax should be framed as a special-purpose tax linked directly to defense spending beyond 1% of GDP. In other words, increases in the defense budget toward the 2% goal would result in automatic hikes in the rate of the surtax. The government will need to be fully accountable in the use of extra revenue, and taxpayers, for their part, should give greater thought to how much they are willing to contribute to enhancing national security.

[1] See Ryoji Fujii, “Saishutsu no fukusu-nendoka ga susumu yosan: Fueru keizokuhi, kokko saimu futan koi” (Multiple-Year Budgetary Appropriations: Growth in Continuing Expenditures and Deferred Payments), Keizai no Purizumu, no. 181, 2019.

[2] According to Takashi Asaba’s “Kokko saimu futan koi no saimusei to jittai bunseki” (Multiyear Payments as Liabilities and Analysis of Current Conditions) in Shoken Keizai Kenkyu, no. 113, 2021, in fiscal 2020 the MOD accounted for more than 50% of all multiyear payments in the national budget, while the MLIT accounted for just under 30%. Together, these two ministries accounted for over three-fourths of the total.

[3] To maintain long-term fiscal consistency, new liabilities may be entered at the present value of future expenditures. For example, if the interest rate is 2% and next year’s payment is to be ¥10.2 billion, the obligation can be itemized as ¥10 billion in this year’s budget.

[4] Another idea is to impose the same kind of surtax on corporate taxes based on the notion that national defense is needed to protect economic activity. Even better would be to introduce an asset tax, as this would require low-income but high-wealth households (such as the elderly with significant financial assets) to make commensurate contributions, but this would require a fundamental reform of Japan’s tax system.

-

-

- Nonresident Senior Fellow

- Motohiro Sato

- Motohiro Sato

- Areas of Expertise

-

- Local public finance

- Optimal taxation theory, tax reform

- Social security, health economics

- Research Project

-

Featured Content

-

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

Can Japanese Corporations Change?

Can Japanese Corporations Change?

-

Japanese Honeybee

Japanese Honeybee

-

The Perilous Decline of Japanese Agriculture

The Perilous Decline of Japanese Agriculture