Can Japanese Corporations Change?

August 16, 2023

R-2023-027E

Substantial wage hikes and sustained growth in capital spending by Japanese companies have fueled hope for an industrial renaissance and an end to the country’s economic stagnation. But change will not come overnight.

* * *

The media has been reporting some encouraging developments in Japanese industry since the beginning of this year, and foreign investors are eyeing the Japanese stock market with renewed interest. But it will take time and effort to regain the ground lost through three decades of inadequate capital investment.

Steepest Wage Hike in Three Decades

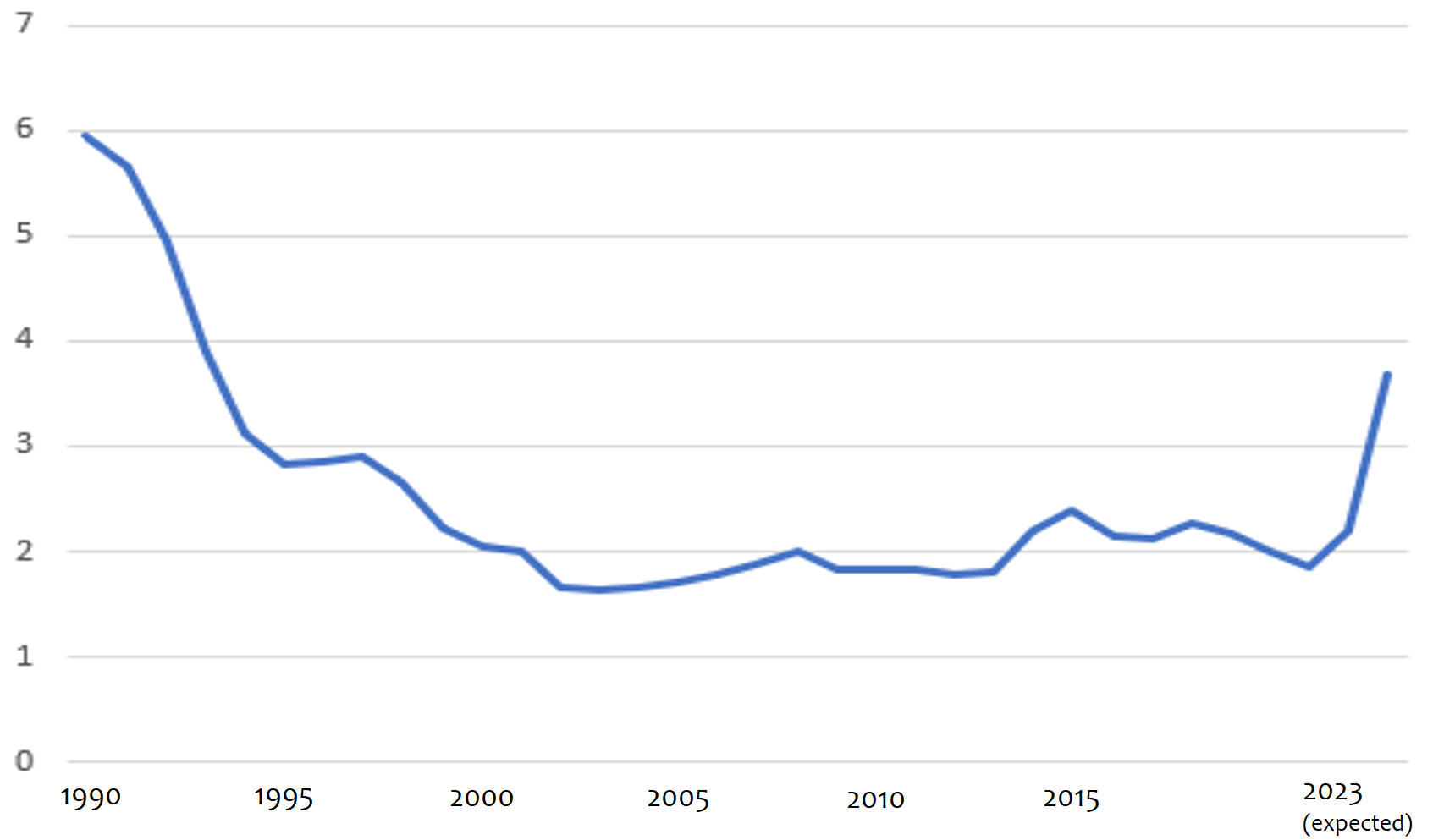

The most heartening news on the business front this year was the unexpectedly large annual wage increases coming out of the 2023 “spring labor offensive,” or shunto.

According to the final tally released by Rengo (Japanese Trade Union Confederation) on July 5, the average wage increase among its member unions was 3.58%, the largest hike in three decades. Dwarfing the biggest increase of the second Shinzo Abe administration (2.38% in 2015), when the government intervened in negotiations, the latest wage hike was also well above the 2.85% predicted by economists in January this year in the special ESP Forecast.[1] Even excluding scheduled seniority raises, it still amounts to a 2% increase in base pay.[2] Back in spring, when major corporations began announcing substantial increases, many analysts doubted that small and medium-sized companies could follow their lead. But the Rengo survey found that even companies with fewer than 300 employees were raising wages by 3.23% on average—somewhat less than the big corporations but still considerably more than anticipated.

Figure 1. Shunto Wage Increases, 1990–2023

(%)

Moreover, management seems to have moved more or less of its own volition this year, as opposed to succumbing to intense pressure from organized labor. As I noted back in February, Japanese business leaders reacted more positively than expected to Prime Minister Fumio Kishida’s January call for wage increases in excess of price inflation; some even responded with specific targets higher than 3%.[3] Inflation was obviously an important factor. With rising prices cutting into real wages, managers clearly recognized that pay hikes were needed to maintain employee morale.

Moreover, for two or three years now, the realization has been dawning that Japanese companies will ultimately have to pay more to secure high-caliber employees in today’s tight labor market. (Even so, there were few signs of movement until this year, possibly because no one wanted to be the first to break ranks.) Another factor seems to have been a growing awareness among Japan’s multinationals that their Japanese employees were making too little, especially with the yen falling against the dollar and other currencies.

Government figures published in April 2023, though, showed that regular wages were a mere 0.8% higher than a year earlier in nominal terms and 3.3% lower in real terms, prompting some economists to call the wage increases insufficient.[4] But wages will likely continue rising as the year progresses, as they generally have in years when the shunto pay hikes were substantial. Meanwhile, price inflation continues apace: The year-on-year increase in the Bank of Japan’s so called core-core Consumer Price Index (excluding fresh foods and energy) jumped from 3.0% in December 2022 to 4.3% this past May. (The BOJ’s forecast that inflation will fall below 2% in the second half of fiscal year 2023 is beginning to look rather doubtful.) Under these circumstances, one can reasonably expect a comparable round of wage increases next spring.[5]

Shifting Corporate Mindset

Wage hikes are not the only cause for optimism. We are also seeing signs of aggressive and sustained fixed investment, a welcome development for Japanese industry. According to the Tankan quarterly survey of business sentiment published in June by the BOJ, fixed investment (including land purchases) rose 9.2% in fiscal 2022 and is projected to rise 11.8% this fiscal year (5.5 points higher than the figure reported in March). Particularly encouraging are ongoing signs of robust investment in software (up 11.5% in fiscal 2022 and projected to increase 14.6% in 2023) and in research and development (up 8.5% in 2022 and projected to increase 4.1% in 2023).[6]

The BOJ’s Flow of Funds figures have attracted notice as well. Generally speaking, private nonfinancial companies have been accumulating financial surpluses ever since the Japanese financial crisis of 1997–98, but they registered a deficit in the second half of 2022—no doubt reflecting the growth in fixed investment. This does not signal an extended shortage of funds, as the sector again saw a surplus in the first quarter of 2023. But it may well indicate a changing mindset. One of the most salient trends in Japanese business over the past 25 years has been the tendency of big firms—having seen how a financial crisis can leave firms on the brink of bankruptcy—to save up for a rainy day. Even when making profits, they have squirreled them away as retained earnings instead of using them to boost wages or invest in the future. In fact, Waseda University economics professor Shin’ichi Hirota has marshaled empirical data to argue that the capital-raising behavior of Japan’s listed companies is more about optimizing their chances of survival than maximizing corporate value.[7]

Some have countered that a bigger reason for the dearth of domestic investment among big businesses has been Japan’s shrinking population and, accordingly, a smaller market. It is true that a sizable portion of Japanese companies’ retained earnings have been invested in shares of foreign subsidiaries and other overseas assets. However, as professor emeritus of the University of Tokyo Hiroshi Yoshikawa has pointed out again and again, Japan’s shrinking population is just one, relatively small, factor behind the economy’s slow growth. Big business’s reluctance to invest and to raise wages has had a much greater impact, as is clear when one analyzes the relative contributions of different factors to the potential growth rate. The most likely reason big Japanese firms have channeled most of their new business investment overseas instead of domestically is that, in the event of failure, it is easier to shut down a foreign subsidiary than to lay off permanent employees working in Japan.

It is not entirely clear why Japanese corporations are behaving differently now, but one senses that they may finally be recovering from the trauma of the financial crisis.[8] No doubt that perception has helped to drive a surge in the Japanese stock market, with overseas investors jumping in to push the Nikkei average to a 33-year high in June. Of course, this is partly because Japan offers a more attractive choice at the moment than either the United States and Europe, where interest rates continue to rise in response to inflation concerns, or China, which has become the target of stricter economic security policies. But the trend no doubt also reflects an awareness of the abovementioned signs of change in Japanese corporate behavior.

A Long Road to Revitalization

I believe that Japanese corporations are making a real effort to change, but whether they can actually do so is a different question. Three decades of inadequate investment in physical and human capital have significantly eroded the core strengths of domestic industry and the Japanese economy. This is reflected in businesses’ own expectations for economic growth, as tabulated in the fiscal 2022 Annual Survey of Corporate Behavior released by the Cabinet Office in March. Both the three-year and five-year forecasts averaged a mere 1.2%. While this is a slight improvement from the forecasts of the previous two years (at the height of the pandemic), it is essentially unchanged from the pre-pandemic outlook. Without solid growth expectations, one must question whether recent changes in corporate behavior can be sustained.

There are other, more substantive, causes for concern. One is the declining competitiveness of Japanese capital goods.

Capital goods are a crucial component of Japan’s export structure. The impact of the 2008 Wall Street meltdown on the Japanese economy—which was largely insulated from financial losses—resulted primarily from a sharp drop in capital-goods exports as global investment in capital and equipment plummeted. In other words, Japan was a victim of its own success in this domain.

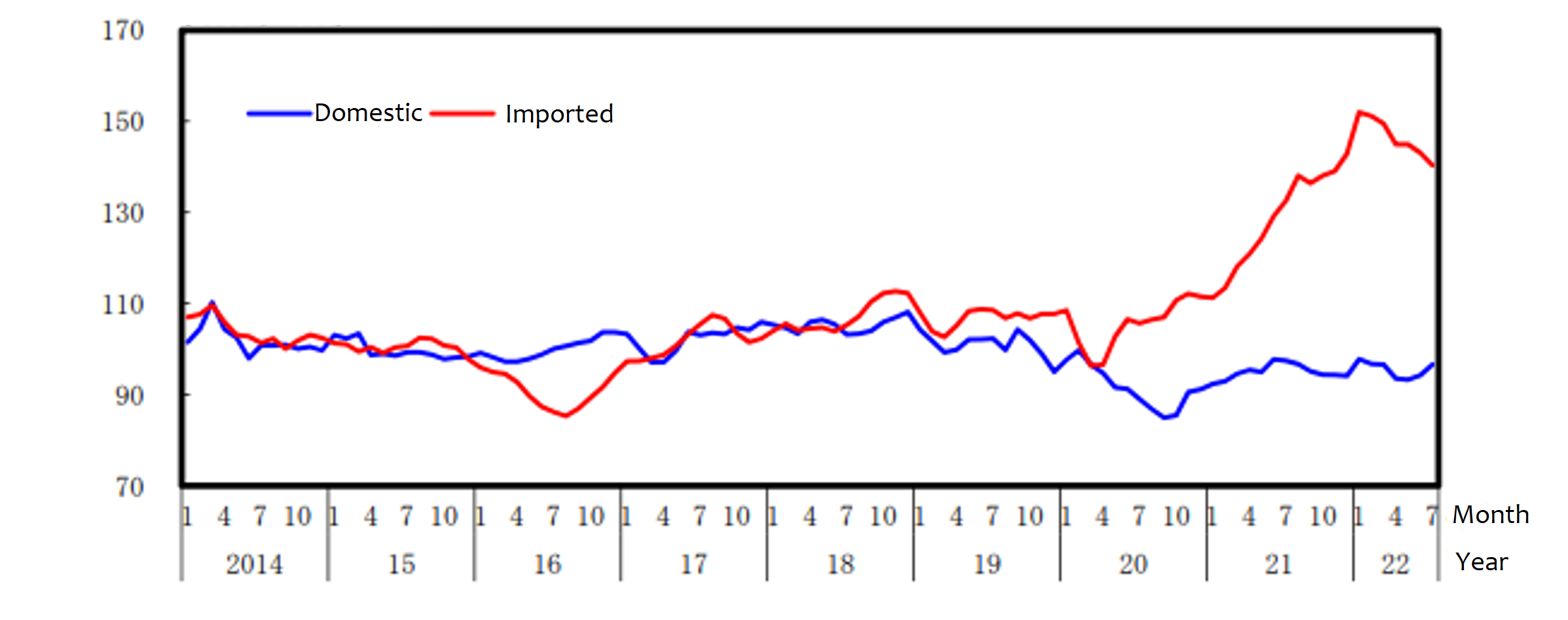

Now there are indications of a long-term decline amid the transition to a digital, low-carbon economy. Figure 2 shows a sharp increase in Japanese imports of capital goods.[9] Moreover, a large share of those imports are in the areas of digital and decarbonization technology. More specifically, there has been a substantial increase in imports from China of notebook PCs and other remote-work devices and renewable-energy equipment, such as solar panels. In the semiconductor manufacturing sector, Japan has been importing more front-end equipment from Europe and the United States. Even as Japanese businesses trumpet their digital-transformation and decarbonization initiatives, they are depending heavily foreign equipment for both transitions.

Meanwhile, in fiscal 2022, the combination of growth in capital goods imports and a weaker yen led to a 4% increase in the fixed investment deflator, which rarely rises. This no doubt contributed to the strength of the Tankan projections for fixed investment, which are nominal values.[10]

Figure 2. Aggregate Supply of Capital Goods

(Index: 2015=100)

Source: Cabinet Office, Monthly Topics on Economic Affairs, October 2022. https://www5.cao.go.jp/keizai3/monthly_topics/2022/1005/topics_068.pdf.

Note: Data plotted using three-month backward moving averages, based on industrial-sector aggregate-supply data published by the Ministry of Economy, Trade, and Industry.

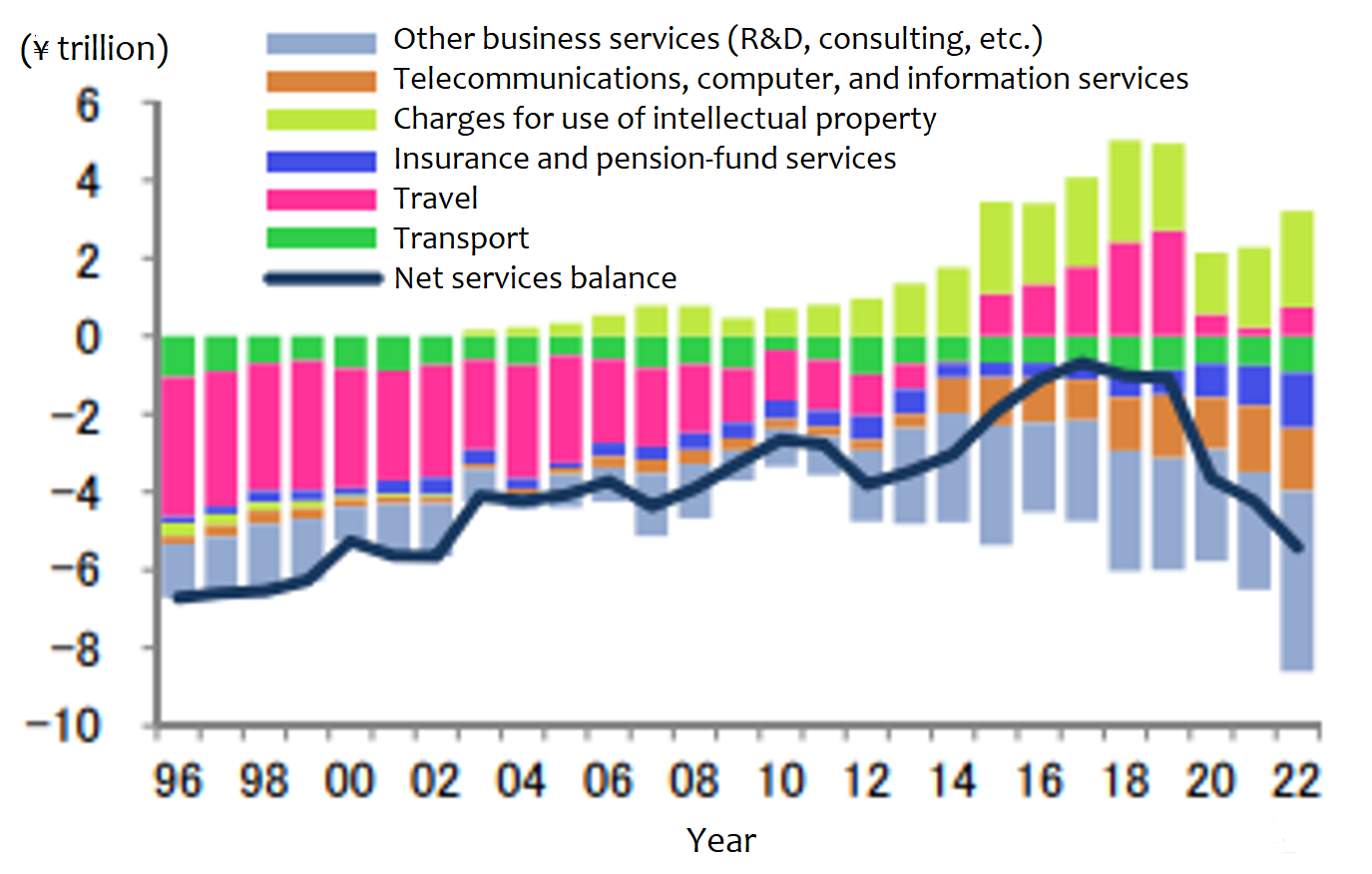

Another source of concern is Japan’s growing trade deficit in “other services” (Figure 3). This category, which excludes travel, encompasses telecommunications, computer, and information services; professional and management consulting services; R&D services; and charges for the use of intellectual property. Japan’s swelling deficit in these high-tech and knowledge-intensive areas is another indication of declining competitiveness.[11] To be sure, Japan is registering a net surplus in usage fees for intellectual property, but this is mainly due to intragroup transactions—that is, payments from overseas manufacturing subsidiaries for the use of “industrial property,” such as blueprints and production technology. In terms of transactions for copyrighted material, particularly in the digital domain, Japan’s deficit has been rising. Because of the burgeoning deficit in “other services,” the overall service deficit has been slow to shrink despite the dramatic increase in inbound tourism following the lifting of pandemic-related border measures.

Figure 3. Services Balance by Component

Source: Mizuho Research & Technologies, “Omotenashi wa ‘takai Nippon’ de—Mezashitai kyosoryoku no fukkatsu,” Momma Kazuo no keizai fukayomi, May 23, 2023.

Note: Compiled from BOJ data.

Finally, there is no denying that Japan’s auto industry, a symbol of the country’s manufacturing prowess and the mainstay of its export-driven economy, has lagged behind both the United States and China in the development and production of electric vehicles. Not long ago, people in the industry would contend that hybrids would continue to dominate the market for some time to come, but one rarely hears that argument anymore.

It may well be that Japanese businesses have turned a corner in terms of their general outlook. But it will take time to regain competitiveness through improvements in productivity and technical innovation. The revitalization of the Japanese economy must be viewed as a long-term undertaking.

[1] The 2015 results and ESP forecasts are both based on data published by the Ministry of Health, Labor, and Welfare, while the 2023 results cited here are based on Rengo’s survey. However, in the past, no major discrepancies have been observed between the two sources.

[2] According to Rengo, the average increase in base pay (excluding scheduled raises) among all members was 2.12%; among small and medium-sized firms it was 1.96%.

[3] See “Chin’age o unagasu futatsu no chikara—Kozoteki hitode-busoku ni mukau Nihon keizai” (Two Forces for Higher Wage—Japanese Economy Facing Structural Labor Shortages), Tokyo Foundation for Policy Research, February 6, 2023, https://www.tkfd.or.jp/research/detail.php?id=4178.

[4] Note, moreover, that real wages are calculated using the CPI of “all items less imputed rent” rather than “all items less fresh food.” In May this year, the year-on-year increase was 3.8% for the former and 3.2% for the latter, resulting in lower figures for real wages.

[5] A significant number of analysts continue to maintain that this year’s big wage increase was a one-time event. However, in a Nikkei survey of 100 CEOs, published on July 3, 2023, among companies that had already adopted a basic stance on wage hikes in fiscal 2024, the largest share indicated that they were prepared to grant an increase in excess of 4%.

[6] Taken alone, the projected growth for R&D investment in fiscal 2023 may not seem that high. However, labor costs make up a large share of R&D spending, thus tending to minimize year-to-year fluctuations. Even in years when R&D spending is relatively unchanged, therefore, there can be substantial increases in investment. What is important here is that R&D spending appears to be growing steadily as a long-term trend. For more on this topic, see Ayako Masujima and Kazuaki Washimi, “Fast Facts on Japan’s R&D Investment in the Tankan,” Bank of Japan Review, January 25, 2023, https://www.boj.or.jp/en/research/wps_rev/rev_2023/data/rev23e01.pdf.

[7] Shin’ichi Hirota, “Nihon no daikigyo no shikin chotatsu kodo: Seicho ka sonzoku ka” (Capital Raising among Large Japanese Corporations: Growth or Survival?), in Hideaki Miyajima, ed., Nihon no kigyo tochi (Corporate Governance in Japan), Toyo Keizai, 2011.

[8] One likely explanation is a generational change in senior management. When the 1997–98 crisis occurred, a full 25 years ago, today’s executives did not yet occupy the sort of positions that would have forced them to confront the crisis in a managerial capacity. Another reason might be that corporations have accumulated enough of their own capital to feel financially secure. Given that almost all of them survived the pandemic (albeit with generous government assistance in some cases), they may have concluded that they have accumulated all the retained earnings they need. A third possibility is that the growing calls for digital and green transformation have clarified where they should direct their investment. In addition, an increase in mid-career hiring, part of a general shift toward job-based recruitment, may be helping to drive up wages.

[9] For more on this subject, see Cabinet Office, “Shihonzai no yunyu zoka no haikei ni tsuite” (Behind the Increase in Imports of Capital Goods), Monthly Topics no. 68 (October 5, 2022), https://www5.cao.go.jp/keizai3/monthly_topics/2022/1005/topics_068.pdf.

[10] Most recently, weak exports of capital goods, a consequence of monetary tightening overseas, have emerged as a drag on economic growth. In October–December 2022, January–March 2023, and April–May 2023, exports of capital goods fell by 2.0%, 8.8%, and 3.8%, respectively, from the previous period.

[11] This issue has attracted the attention of several economists since it was addressed by the BOJ in the summer of 2022 in the report “Japan’s Balance of Payments and International Investment Position for 2021.”

-

-

- SENIOR FELLOW(–FY2024)

- Hideo Hayakawa

- Hideo Hayakawa

- Areas of Expertise

-

- Japanese economy

- monetary and fiscal policy

- economic thought

-

Featured Content

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

Japanese Honeybee

Japanese Honeybee

-

The Perilous Decline of Japanese Agriculture

The Perilous Decline of Japanese Agriculture

-

Addressing Japan’s “drug loss – drug lag”: An analysis and proposals for revamp

Addressing Japan’s “drug loss – drug lag”: An analysis and proposals for revamp

-

Cracking Down on Digital Tax Avoidance

Cracking Down on Digital Tax Avoidance