The Cycle of Failure in Japanese Fiscal Policy (2): Unproductive Allocation of Resources

December 21, 2021

R-2021-015E

Japanese fiscal policy is trapped in a vicious cycle, as public mistrust of government breeds ever-intensifying resistance to taxes. In part 2 of his analysis, Hideo Hayakawa explores the relationship between Japan’s low potential growth rate and its dwindling investments in intangible and human capital.

* * *

In part 1 of this article, I discussed the fiscal constraints imposed by unavoidable increases in social security costs driven by demographic aging, highlighting Japan’s low level of public expenditure on education, scientific research, and active labor-market policies. My focus on those three budget categories is motivated by a suspicion that cutbacks in those areas have contributed to the decline in the Japanese economy’s potential growth rate. Let us now explore that hypothesis.

Japan’s Declining Potential Growth Rate

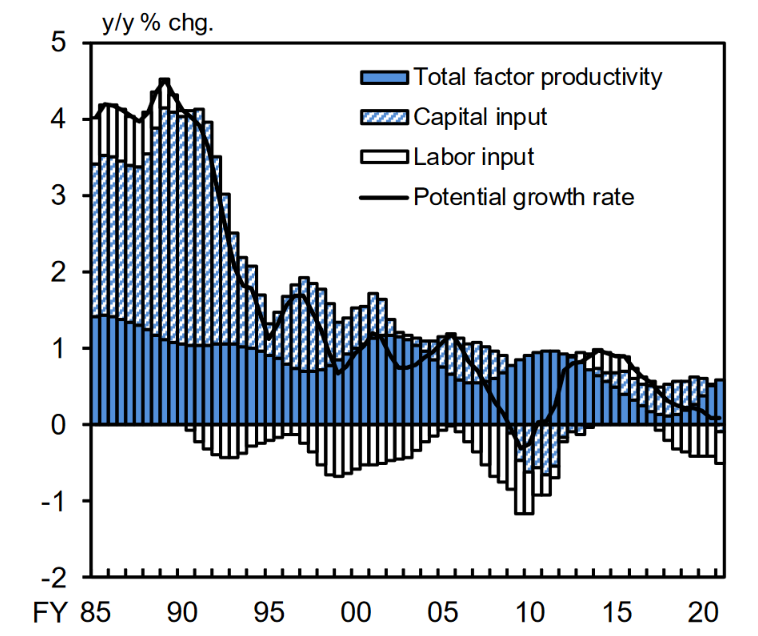

Japan’s potential growth rate, a measure of the economy’s capacity for sustained growth, has fallen sharply since the collapse of the 1980s asset-price bubble, which ushered in a long era of stagnation and deflation. The expansionary policies adopted by Prime Minister Shinzo Abe after 2012 nudged Japan out of its deflationary quagmire, but the PGR quickly resumed its downward trend (Figure 1). The Bank of Japan’s latest estimate puts the PGR at a dismal 0.1%, while the Cabinet Office proposes 0.5%. While BOJ’s estimate is probably too low, it seems safe to assume that Japan’s current potential growth rate is less than 1%.[1]

Figure 1. Japan’s Potential Growth Rate, 1985–2020 (BOJ estimates)

Source: Bank of Japan, Outlook for Economic Activity and Prices, October 2021, https://www.boj.or.jp/en/mopo/outlook/index.htm/#p01.

A variety of circumstances can be adduced to explain the decline in PGR, particularly Japan’s dwindling working-age population and the lingering effect of the nonperforming loans that piled up after the collapse of the 1980s asset-price bubble. But the manner in which fiscal resources have been allocated could be a contributing factor as well. Proponents of endogenous growth theory have developed economic models linking long-term growth to sound government investment (in infrastructure, for example), providing a theoretical basis for the notion of “wise spending” as a means of boosting growth potential.[2] In Japan, the British-born economist David Atkinson, who advised former Prime Minister Yoshihide Suga on economic policy, has stressed the need to expand the kind of “productive government spending” that nurtures long-term growth.[3]

But what kinds of expenditure qualify as “productive” in today’s Japan?

There is no doubt that large-scale public investment in “hard” infrastructure, such as public transportation and roads, contributed substantially to Japan’s high-paced growth in the 1960s and early 1970s, and it doubtless serves much the same purpose in many developing countries today. But Japan can no longer expect a very high return on public investment in expressways or high-speed rail, especially given the continuing decline in usership.

Instead of physical capital, today’s economists have begun looking to intangible assets and human resources as the keys to sustained growth in our post-industrial digital era.

Building Intangible Assets

In Japan, interest in the subject of intangible assets has surged since the appearance of two books in January 2020, just before the COVID-19 pandemic hit: a Japanese translation of Capitalism without Capital by Jonathan Haskel and Stian Westlake (originally published in English in 2018) and Toru Morotomi’s Shihonshugi no atarashii katachi (The New Shape of Capitalism). Both books argue that intangible assets—not physical capital—are the main drivers of growth in today’s economy. The thesis has found a receptive audience among Japanese economists and business leaders alike, given the manifest success of tech companies like Google, Apple, Facebook, and Amazon (or GAFA, as they are collectively known).

What, then, do we mean by intangible assets? Carol Corrado, Charles Hulten, and Daniel Sichel have proposed three broad categories of intangible corporate assets: (1) computerized information, including software and databases; (2) innovative property, including information generated by R&D, copyrights, and designs; and (3) economic competencies, including brand equity, firm-specific human capital, and organizational structure.[4]

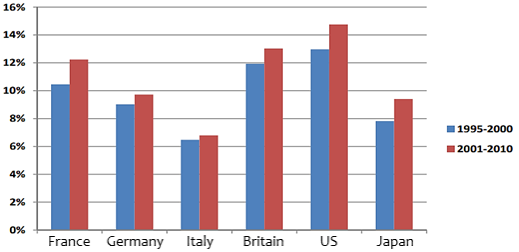

In Japan, meanwhile, a research team led by Tsutomu Miyakawa of Gakushuin University has been using similar methodology to estimate formation of intangible assets in Japan and analyze the economic effect of investment in such assets.[5] According to the team’s findings, Japan has lagged behind countries like the United States, Britain, Germany, and France in its investment in intangible assets (Figure 2), and its annual investment in intangibles has fallen since peaking at around ¥40 trillion in 2010.[6]

Figure 2. Investment in Intangible Assets as a Percentage of GDP

Source: Miyakawa et al., “Mukei shisan toshi to Nihon no keizai seicho” (Intangible Assets and Japan’s Economic Growth), RIETI Police Discussion Paper Series 15-P-010, June 2015.

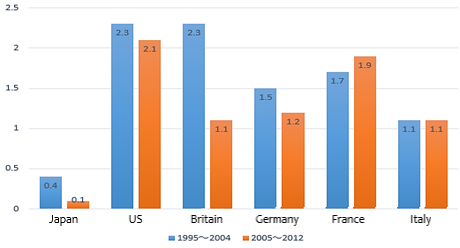

Another focus of research in recent years has been the relationship between investment in human resources and long-term economic growth. Human resources, of course, are inseparable from such intangible business assets as firm-specific human capital, and they also give rise to much of the knowledge embedded in such assets as software, copyrights, and designs. According to estimates generated by Miyakawa’s team, Japanese investment in human resources has fallen off dramatically since 2005 (Figure 3). While it is important to recognize that these estimates do not factor in on-the-job training, the sharp drop in investment nevertheless suggests that the human-resource budgets of Japanese corporations have taken a major hit during the years of economic stagnation.[7]

Figure 3. Investment in Human Resources as a Percentage of GDP

Source: Tsutomu Miyakawa, Seisansei to wa nani ka (What Is Productivity?), Chikuma Shinsho, 2018.

The Role of Government

As we have seen, Japan lags behind other leading industrial countries when it comes to investment in intangible assets and human resources—the very areas economists have highlighted as keys to productivity and long-term growth—and it is highly probable that this has contributed to the decline in Japan’s PGR. Of course, some may counter that it is up to businesses—not government—to make the necessary investments in their own intangible and human capital. But intangible assets have a spillover effect that benefits the economy as a whole, much as public goods do.[8] From this standpoint, it is easy to make the case for government investment in education, technology, and career training as quasi-public goods. Let us explore the impact of inadequate government spending in these areas.

One influential index of educational achievement at the secondary level is the OECD’s Program for International Student Assessment (PISA), which assesses the reading, math, and science skills of 15-year-olds in OECD countries around the world. In the latest (2018) PISA survey, Japanese students ranked eleventh out of 37 countries in reading, an area in which achievement appears to be declining slightly. In mathematics and science, they continue to perform well, ranking first and second, respectively. These results suggest that Japan continues to do an admirable job educating students at the primary and secondary levels (although credit for that should probably go to the nation’s dedicated and overworked school teachers).

When it comes to higher education and scientific research, however, a more troubling picture emerges. For example, Japan is being overtaken by other countries in the production of scientific papers, according to the 2021 Indicators of Science and Technology, published by the Ministry of Education, Culture, Sports, Science, and Technology. Between the 2006–8 and 2016–18 periods, Japan dropped from fifth to tenth place with respect to the top 10% of the most cited papers and from seventh to ninth with respect to the top 1%—despite the fact that the overall number of papers saw just a slight decline from third to fourth place. These worrying statistics add weight to the yearly lamentations of our Nobel prize–winning scientists, who warn that Japan is unlikely to maintain its Nobel track record if government support for scientific research continues to languish.

Another area of spending that deserves a closer look is active labor-market policies. The preferred approach of the Japanese government—on full display during the COVID-19 crisis—is to protect businesses from downswings via such measures as employment adjustment subsidies, which keep workers on the payroll by subsidizing leave allowances to furloughed employees. Unfortunately, such assistance often has the effect of propping up uncompetitive companies. Research carried out over many years by Professor Kyoji Fukao, head of the Institute of Developing Economies, has revealed that firm entry and exit have contributed very little to productivity increases in Japan. These findings support the theory that employment policies geared to protecting businesses have helped to drag down the Japanese economy’s potential growth rate.[9]

Scandinavian countries, by contrast, allow companies to fail when they are uncompetitive and focus government resources on the retraining and reemployment of workers who have lost their jobs. In this way, government functions as an actor in the “reskilling” of the labor force.[10]

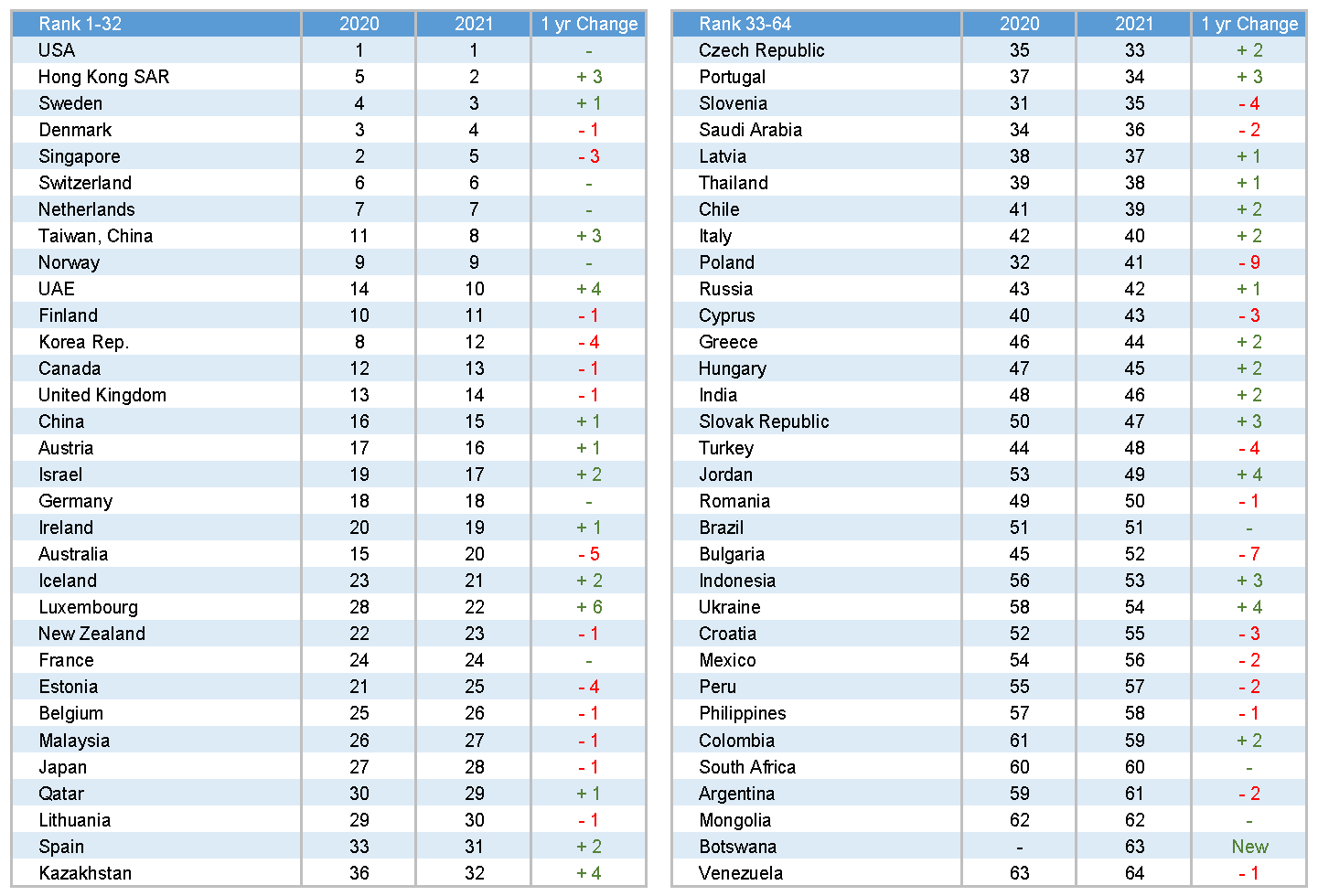

Active labor-market policies are all the more vital today, with digital technology transforming business processes, the industrial structure, and the skill sets demanded of workers. It can scarcely be a coincidence that the Scandinavian countries all rank high in the World Digital Competitiveness Ranking compiled yearly by the IMD World Competitiveness Center. (Japan is number 28 out of 64; see Figure 4.)

Figure 4. World Digital Competitiveness Ranking

Source: IMD World Competitiveness Center, World Digital Competitiveness Ranking 2021, https://www.imd.org/centers/world-competitiveness-center/rankings/world-digital-competitiveness/.

The Vicious Cycle of Mistrust in Government

Although a direct cause-and-effect relationship is extremely difficult to establish, circumstantial evidence strongly suggests that the squeeze on government expenditure on education, scientific research, and active labor-market policies has contributed to Japan’s economic stagnation by depressing the potential growth rate. As noted earlier, these budget constraints are the result of the government’s inability to win public support for tax hikes needed to fully finance Japan’s swelling social security budget. But as households struggle to make ends meet, the government’s failure to stimulate long-term growth can only strengthen their resistance to paying higher taxes, creating a vicious cycle. The mistrust and resistance is bound to be strongest among younger adults, who pay into the health insurance and pension systems without seeing substantial benefits. A lack of faith in the government and the future of the pension system may be one factor behind the rising savings rate among people in their twenties over the past decade.[11]

Suspicion of the government is also one reason for Japan’s glacial progress toward a fuller embrace of the My Number taxpayer identification system; the Japanese people simply do not trust the government to store and protect their personal information. That lack of confidence is bound to have repercussions for the recently launched Digital Agency and its mission to accelerate and integrate digitalization of public administration.

Here, too, Japan stands in sharp contrast to the Scandinavian countries. According to the United Nations’ 2020 E-Government Survey, the world’s top performer in e-government development is Denmark, while Finland and Sweden rank fourth and sixth, respectively. These are also countries whose citizens do not balk at high taxes to finance generous social benefits. The common denominator is undoubtedly a high level of public trust in government.

It is, after all, the job of our political leaders to convince voters of the importance of government programs and call on them to shoulder the burden, with the understanding that their tax money is supporting the “wise spending” needed to nurture sustained economic growth. Unfortunately, the Japanese government has failed in this task, and to all appearances the pandemic has only deepened the public’s mistrust.

Our political leaders are now resorting to deficit-financed cash handouts to buy back the trust they have forfeited. It is a woefully short-sighted strategy that can only perpetuate the cycle of failure.

[1] Although calculations of potential growth rate are supposed to exclude the effects of cyclic fluctuations, this is not actually possible in practice; growth in capital stocks for example, is affected by cyclic fluctuations in plant and equipment investment. It seems likely that factors linked to the economic slowdown that began in 2018 and the COVID-19 recession have depressed recent estimates by the Japanese government and the BOJ. With this in mind, I would propose a figure between 0.5% and 0.9% as a more accurate estimation of Japan’s potential growth rate.

[2] See, for example, Robert Barro, “Government Spending in a Simple Model of Endogenous Growth,” Journal of Political Economy, vol. 98, no. 5 (October 1990). Many economists have criticized the stimulus approved by the Kishida cabinet, with its emphasis on cash benefits, as an example of unwise spending.

[3] See David Atkinson, “Seicho no tame ni honto ni yarubeki koto” (What We Really Need to Do to Foster Growth), Nihon Keizai Shimbun, November 5, 2021.

[4] See Carol Corrado, Charles Hulten, and Daniel Sichel, “Intangible Capital and U.S. Economic Growth,” Review of Income and Wealth, series 55, no. 3 (September 2009).

[5] See, for example, Tsutomu Miyakawa et al., Intanjiburuzu ekonomi: Mukei shisan toshi to Nihon no seisansei (Intangibles Economy: Investment in Intangible Assets and the Productivity of the Japanese Economy), University of Tokyo Press, 2016.

[6] See Tsutomu Miyakawa and Shoichi Hisa, “Sangyo-betsu mukei shisan toshi to Nihon no keizai seicho” (Japan’s Economic Growth and Investment in Intangible Assets by Industry), Financial Review, no. 112 (January 2013). This study compares labor productivity growth accounting results for multiple countries between 1995 to 2007 and finds that the contribution of intangible assets to labor productivity growth in Japan is low compared with Western countries.

[7] Miyakawa believes that Japanese corporate investment in human resources peaked in 1991, just before the collapse of the asset-price bubble, and plunged to 16% of that peak level by 2015.

[8] Laws protecting private entities’ intellectual property rights exist precisely because without such protection, the incentive to create quasi-public goods through research and innovation would be lost.

[9] Kyoji Fukao, Ushinawareta 20-nen to Nihon keizai (The Japanese Economy and the Lost Two Decades), Nihon Keizai Shimbun Shuppan Sha, 2012.

[10] For a discussion of Sweden as an example of economic vitality in a welfare state, see Kenji Yumoto and Yoshimune Sato, Suweden paradokkusu (The Swedish Paradox), Nihon Keizai Shimbun Shuppan Sha, 2010.

[11] One factor is undoubtedly the rise of non-regular employment, which offers scant job security and less generous benefits than permanent employment. However, the employment situation has actually improved for younger workers over the past decade as Japan’s baby-boomers have reached retirement age.

-

-

- SENIOR FELLOW(–FY2024)

- Hideo Hayakawa

- Hideo Hayakawa

- Areas of Expertise

-

- Japanese economy

- monetary and fiscal policy

- economic thought

-

Featured Content

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

The Perilous Decline of Japanese Agriculture

The Perilous Decline of Japanese Agriculture

-

Can Japanese Corporations Change?

Can Japanese Corporations Change?

-

Turning Waste into Wealth: Japan’s ¥13 Trillion Opportunity

Turning Waste into Wealth: Japan’s ¥13 Trillion Opportunity

-

In Japan, Men Have Complicated Views about Gender and Equality

In Japan, Men Have Complicated Views about Gender and Equality