- Article

- Tax & Social Security Reform

To Revive the Economy, Empower the Middle Class: Redistribution as the Key to Revitalization

August 25, 2016

In a recent piece in the Nihon Keizai Shimbun, Shigeki Morinobu call s for a working tax credit and other measures to reduce economic inequality and empower the middle class, arguing that the trickle-down approach of Abenomics has been tried and found wanting.

* * *

Three years have passed since the government of Prime Minister Shinzo Abe launched the expansionist economic program known as Abenomics. In that time, real economic growth has averaged 0.6%, well below the 2% achieved under the Democratic Party of Japan (2009-12). The basic reason for this failure to grow is lackluster consumer spending.

Some analysts blame the consumption tax hike of 2014 for this state of affairs. But a full two years after the tax rate went from 5% to 8%, consumption has yet to rebound. This suggests we should look elsewhere for an explanation.

From statistics on household income and expenditures, we can identify two probable culprits: minimal gains in real family income and a decline in the average propensity to consume, reflecting financial anxieties about the future.

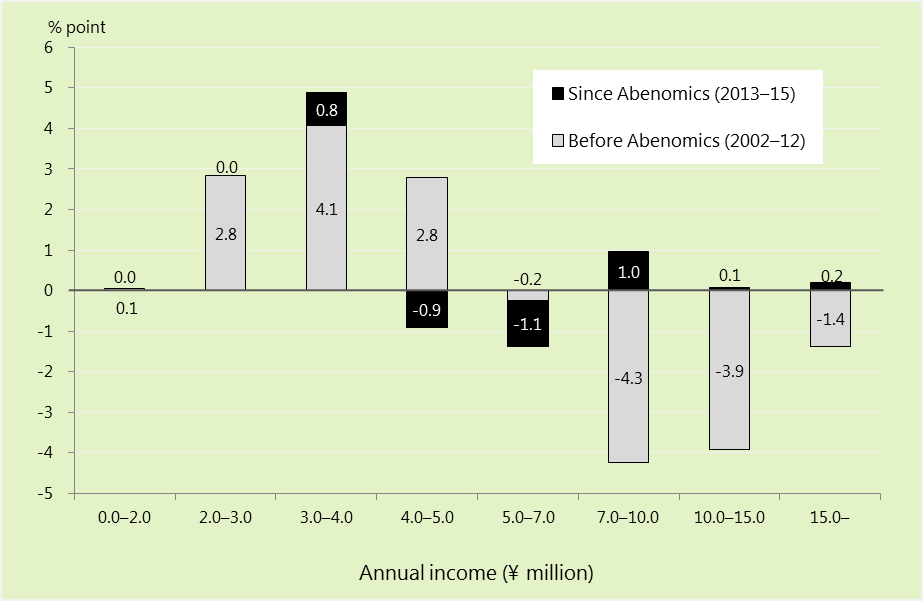

In 2015, Hitotsubashi University economist Takashi Oshio used data from the government’s Survey of Household Economy to compare the distribution of income and wealth among Japanese households before and after the advent of Abenomics. He found that the percentage of households in the ¥4 million to ¥7 million income bracket dwindled after the policies went into effect, while those in the higher and lower brackets grew, indicating an increasingly bipolar income distribution and a pronounced erosion of the middle class.

Figure 1. Changes in the Distribution of Personal Income

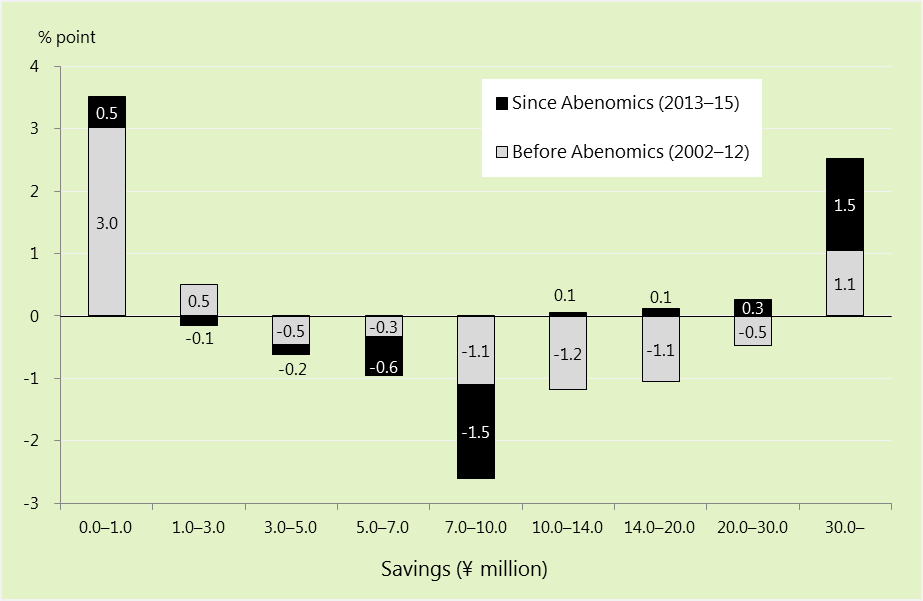

The same trend can be seen in the distribution of assets in the form of savings. Since the start of Abenomics, the percentage of households with a moderate savings balance has decreased, while the segment consisting of those with ¥30 million or more in savings has grown.

Figure 2. Changes in the Distribution of Personal Savings

One important factor behind the growth in income inequality is the increasing percentage of jobs classified as nonregular employment, which typically pays less than the kind of permanent, full-time employment that was once considered the norm. At the same time, the rise in stock prices fueled by Abe’s economic policies has benefited the wealthy and contributed to the bipolar distribution of assets.

The promise of Abenomics was that a weaker yen would boost the profits of businesses reliant on exports, resulting in higher wages and more capital investment, and that these benefits would then trickle down to smaller businesses and regional economies. As the foregoing suggests, this “virtuous circle of growth and prosperity for all” has failed to materialize.

Permanent Policies for Income Redistributi on

The Organization for Economic Cooperation and Development uses the Gini coefficient to compare economic inequality in the advanced economies before and after taxes (including social insurance contributions) and transfers (social security benefits). According to the OECD, Japan has a relatively equitable income distribution before taxes and transfers but ranks among the more unequal countries once taxes and transfers are factored in. What this tells us is that the income-redistribution effect of Japan’s tax and social security systems is among the weakest in the advanced industrial world.

The sluggish consumer spending of recent years reflects the erosion of the middle class in the midst of growing income disparities, compounded by a declining propensity to consume owing to material anxieties. This is a long-term structural problem that cannot be addressed effectively through occasional handouts, such as the distribution of shopping vouchers or supplemental payments to low-income pensioners. Such isolated measures are a waste of the taxpayers’ money.

What the Japanese economy needs is permanent policies for redistributing income and wealth to prevent further economic polarization. Multiple studies by the International Monetary Fund, the OECD, and others have demonstrated that reducing disparities in wealth by redistributing income from those with surplus contributing capacity to those without has a positive effect on economic growth. From a common-sense perspective, it stands to reason that consumer spending would benefit from the transfer of income from the wealthy to lower-income households that devote a much greater portion of their income to consumption.

What, then, is the best way to go about redistributing income and assets?

As we have seen, Japan’s income redistribution mechanisms are weak, and social insurance contributions are at the heart of the problem. The National Pension system is regressive in that it collects the same monthly contribution from everyone regardless of income. Contributions to Employees’ Pension Insurance are adjusted according to income, but the system uses pay-as-you-go financing, which has the effect of transferring income from younger workers with lower incomes to wealthy retirees. We need to reverse the flow and redistribute income from wealthy seniors with surplus contributing capacity to middle- and low-income working people and their families.

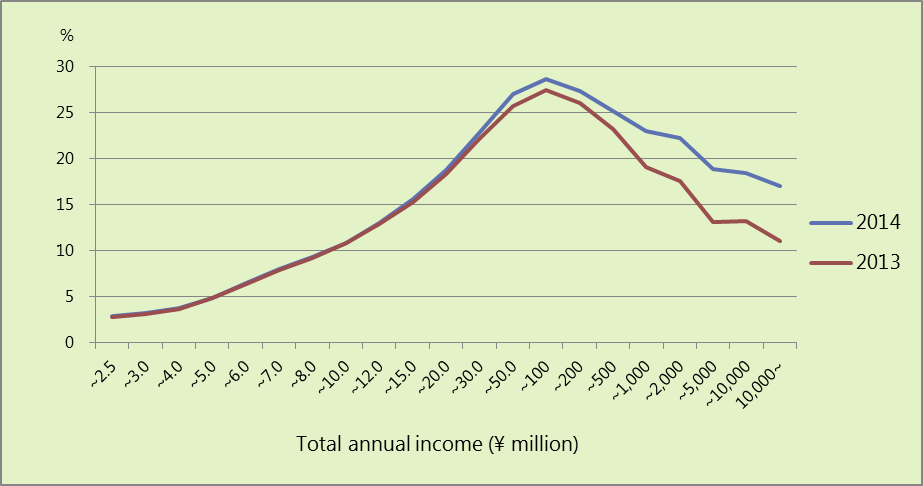

A key source of income among wealthy seniors is capital gains and dividends. In Japan, such investment income is taxed separately from earned income at a fixed rate, which rose from 10% to 20% in 2014. The graph below charts the effective tax rates (all national income taxes combined) for taxpayers at different levels of income (earned and unearned) in 2013 and 2014. In both years, the burden peaked at ¥100 million and declined for those in higher income brackets. The reason is that the tax rate on investment income, which figures prominently in the income of wealthier taxpayers, is substantially lower than the top rate for earned income: 40% (45% since 2015). This disparity causes the effective tax rate to decline when a household’s combined income exceeds ¥100 million.

Figure 3. Effective Tax Rates According to Income Level

Taxing Investment Income

Raising the tax rate on investment income another 5 points is one obvious solution. Abenomics has fueled a rise in stock prices that has further padded the assets of the well-to-do. Increasing the tax burden on investment income from those assets would result in a more equal distribution of income and assets alike.

Raising the tax rate on investment income also makes sense from the standpoint of tax theory. The source of investment income is corporate profits, which have risen as a result of a corporate tax cut of more than 7 points under Abe’s economic policy. It would be appropriate to make up this shortfall through taxes on investment income at the individual level. At the current rate of 20%, tax revenues from investment income come to slightly more than ¥4 trillion. All other things being equal, a 5-point increase would generate almost ¥1 trillion in additional revenues.

The main concern is that the impact of such a tax increase on the stock market could eat into working people’s retirement savings or jeopardize their pension funds. With this in mind, the government should simultaneously expand the system of tax-free individual savings accounts (NISA), including Junior NISA for minors, and extend the tax-free period.

Next, we need to consider ways of reducing the burden on middle- and low-income working-age taxpayers. Disposable income for such households (income minus taxes and social insurance contributions) has been stagnant for more than a decade. The biggest factor here is not the consumption tax hike but the rising cost of social insurance—specifically, health insurance premiums and pension contributions.

According to estimates released by Keidanren (Japan Business Federation), average earned income rose ¥110,000 to ¥5.64 million between 2012 and 2014. But during the same time, social insurance contributions rose ¥50,000, yielding a net increase of just ¥60,000. Meanwhile, the annual social insurance burden for working people is expected to rise another ¥150,000 or so by 2020. Clearly, we need to consider the social insurance burden along with the tax burden when redistributing income.

One promising option is something along the lines of the working tax credit adopted in the Netherlands. This system has the advantage of being relatively cheap to administer, since it deducts a fixed percentage from an individual’s total tax and social insurance bill without requiring a refund. For Japan to adopt such a system, it would need to integrate the collection of taxes and social insurance contributions and make use of My Number—the new national social security/taxpayer identification system—to ensure accurate reporting of total income. In addition to reducing government outlays for livelihood assistance, a working tax credit provides an economic incentive to work. In Japan’s case, it could help tear down the so-called ¥1.3 million barrier, which discourages married women from working full-time by exempting those making under that amount from social security contributions.

Empowering the Middle Class

Planning and introducing a new system like this takes time. I suggest that the government begin with credits to reduce the burden of taxes and social insurance contributions on middle- and low-income working people with household incomes between around ¥4 million and ¥5 million. As the My Number system becomes firmly entrenched, credits can be added based on the number of children in the household.

Because redistribution inevitably yields losers as well as winners, politicians are usually reluctant to rock the boat. But redistribution of income via the tax and social security systems is among the government’s most important responsibilities. It should be clear by now, moreover, that simply calling on industry to boost capital investment and wages will not get Japan back on the path to sustainable growth—nor will further delays in consumption tax increases that have been mandated by law to finance a stronger social security system (another important redistribution mechanism).

What the Japanese economy needs now is policies to expand and empower the middle class by shifting the burden from low- and middle-income earners, including the working poor, to high-income taxpayers (especially well-to-do seniors), while strengthening incentives to work.

Translated from “Arubeki keizai taisaku to wa: Shotoku, shisan no saihaibun susumeyo,” Nihon Keizai Shimbun , April 21, 2016. (Courtesy of Nikkei Inc.)

-

-

- SENIOR POLICY RESEARCH OFFICER

- Shigeki Morinobu

- Shigeki Morinobu

- Areas of Expertise

-

- Tax and fiscal policy

- local finances

- Past Research

-

- The History of Japan’s Consumption Tax: An Archive of Key Events and Documents ( –2021)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan (2021–2022)

- Digitalization of the Economy and International Taxation(-2024)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan 2(-2025)

-

Featured Content

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

Japanese Honeybee

Japanese Honeybee

-

Cracking Down on Digital Tax Avoidance

Cracking Down on Digital Tax Avoidance

-

The Perilous Decline of Japanese Agriculture

The Perilous Decline of Japanese Agriculture

-

Abalone

Abalone