Digital platforms are making it easy for companies to access the services of independent contractors and freelancers, often on a project-by-project basis. While the Japanese government applauds this trend as consistent with its own vision of “work-style reform,” tax expert Shigeki Morinobu stresses the need to adjust Japan’s tax and social security systems and offers some concrete proposals to enhance fairness and compliance.

* * *

One of the planks of Prime Minister Shinzo Abe’s economic revitalization policy is a plan to boost productivity and ensure adequate labor supplies through workplace and labor-market reforms. After a slow start, the government is making significant progress in this direction. On June 29, 2018, the Diet enacted legislation that tackles longstanding problems of excessively long hours, poor work-life balance, and employment inequality, imposing the first hard limits on overtime (including penalties for violators) and embracing the principle of equal pay for equal work.

On another front, the government hopes to encourage the adoption of flexible “work styles.” In its Action Plan for the Realization of Work-Style Reform (June 2017), it advocates telework as “an effective means of balancing childcare and nursing care with work and enabling various people to show their abilities” and argues that “side jobs and multiple jobs [held concurrently] are effective means for development of new technologies . . . [and] preparation for a new life after retirement”( https://www.kantei.go.jp/jp/headline/pdf/20170328/07.pdf ). It also makes note of the rapid growth in “crowdsourcing,” whereby businesses make use of digital platforms to tap into communities of “crowdworkers”ーregistered freelancers and contractors who are able to provide services remotely, often on a project-by-project basis.

Downsides to Teleworking and Crowdworking

Unfortunately, Japan’s current systems are not ideally equipped to deal with these new modes of work. People working in the new economy are vulnerable to unfair labor practices and can slip through gaps in the safety net. When it comes to paying taxes, they confront complexities and ambiguities that threaten to undermine compliance and fairness.

The United States and Europe have already taken steps toward a comprehensive policy response to the challenges of the digital gig economy. But the Japanese governmentーnotwithstanding its enthusiasm for “work-style reform”ーhas been slow to act.

In the aforementioned action plan, the Council for the Realization of Work-Style Reform distinguishes between “employment-type telework” as a flexible workplace arrangement offered to payroll employees and “non-employment-type telework,” carried out by freelancers and independent contractors from home, often with Internet crowdsourcing services (platforms) as intermediaries.

It also notes that teleworkers in the second category (that is, crowdworkers) frequently run into such labor issues as unreasonable deadlines, last-minute assignment changes, low pay, and late payment. Yet instead of drafting measures to address those issues, the council kicked the can down the road by pledging to set up expert panels to deliberate the need for new protections, legal and otherwise, on a medium-to-long-term basis.

Blurred Boundaries between Employment and Business Income

From the standpoint of taxation, telework has the effect of blurring the distinction between employees and independent contractors, making it more difficult to classify individual income under Japan’s system. This turns out to be a major issue.

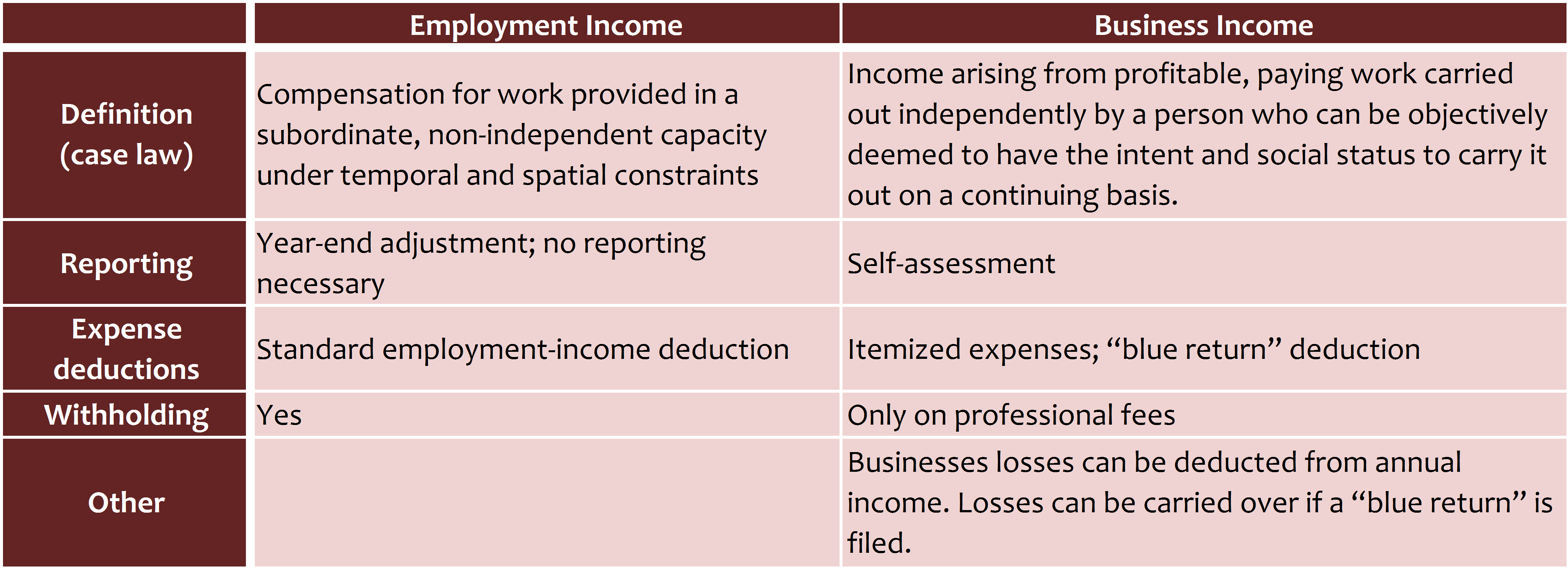

Japan’s individual income tax divides income from compensation into 10 distinct categories, clearly differentiating between employment income, business income, and miscellaneous income (applying to compensation beneath a certain threshold). The rate, method, and rules of taxation vary considerably depending on the income category.

Tax on employment income is withheld at the source, with any under- or overpayment adjusted at year-end. Employees automatically receive a relatively generous standard deduction for necessary expenses. In most cases, there is no need to file a tax return. By contrast, individuals who earn business income are required to file a return. In most cases, they must itemize their business expenses, which typically amount to less than the standard deduction for employment income. In addition, estimated income tax prepayment is required of all individual taxpayers unless their taxes are withheld. (A withholding tax is applied to the fees paid to certain professionals, such as tax accountants, attorneys, and judicial scriveners.)

The distinction between business and miscellaneous income is important as well. In the case of business income, it is possible to declare a loss if expenses exceed income and use that loss to offset other income, thus reducing one’s tax liability. Business losses can also be carried to the next year if one files the required “blue return.” None of this is possible with miscellaneous income.

Taxation of Employment and Business Income

In the case of telework (broadly defined), logic would suggest that compensation an employee receives from his or her regular employer would be classified as employment income, while that received by a networking freelancer or independent contractor would be business income. However, the Supreme Court has ruled that the decisive criterion for judging whether compensation is employment or business income is not the content of the work contract but the actual conditions in which the work is carried outーspecifically, “the presence or absence of spatial and temporal constraints.” As working arrangements diversify and become more flexible, it is becoming increasingly difficult to apply this distinction.

Toward a Standard Deduction for Crowdworkers

Given the growth in crowdworking, it seems to me that the time has come to make it easier for those engaged in such work to calculate and file their income taxes, as we have long done for company employees. To this end, I would make the following recommendations.

First, let us establish a standard deduction for crowdworkers using a simple formula. This could be done by expanding the scope of Article 27 of the Act on Special Measures Concerning Taxation, which creates special rules for calculating taxable business income from such home-based business activities as door-to-door sales of Yakult products and Yamaha music lessons. That would allow freelance teleworkers and others with qualifying income to take an automatic 650,000 yen deduction for business expenses in addition to the 480,000 yen basic exemption. The “blue return” deduction (either 100,000 yen or 650,000 yen) would also be available to qualified taxpayers. Such a system would greatly simplify tax filing while reducing the tax burden, leading to better tax compliance. In 2017, Britain adopted a simplified tax allowance geared to the “sharing economy.” Japan should consider something similar.

Leveraging the New Taxpayer ID System

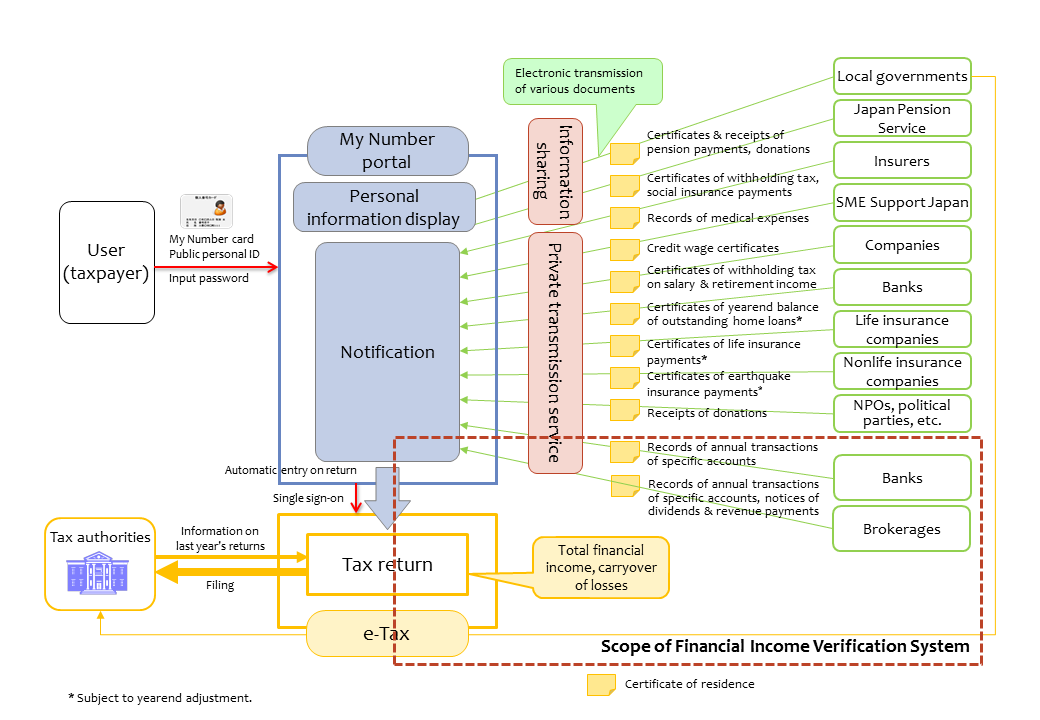

My second recommendation is to take advantage of the My Number taxpayer identification system to create a mechanism for partial prepopulating of electronic tax returns, thereby simplifying tax filing for the growing ranks of crowdworkers.

A System of Prepopulated Tax Returns

Today many European countries provide prepopulated tax returns as a service to individual taxpayers. Using the information that employers and financial institutions are legally required to submit, the tax office enters the appropriate values for income and standard deductions into each individual’s income tax return and sends the prepopulated form electronically to the taxpayer, who can correct or supplement the entered information as necessary before signing and filing the return.

Instituting a comprehensive system like this will take some time. In the meantime, however, the National Tax Agency could leverage the My Number system to make tax filing considerably simpler for crowdworkers and others in the digital gig economy. The Internet platform businesses that connect the services of freelancers and contractors to clients naturally keep records of the payments they make to their registered members. The government should require those companies to keep each member’s My Number on file and use it to transmit income information to the corresponding My Number account, where it can be easily accessed by the individual via his or her My Number portal. In addition, it should facilitate transfer of that information to the individual’s electronic tax return via the My Number portal. This would almost certainly improve tax compliance by making it easier for such individuals to file.

“Work-style reform” calls for corresponding changes in the tax system. It is time for our policymakers to begin deliberating concrete ideas for leveraging information technology to simplify income tax filing in the digital gig economy.

-

-

- SENIOR POLICY RESEARCH OFFICER

- Shigeki Morinobu

- Shigeki Morinobu

- Areas of Expertise

-

- Tax and fiscal policy

- local finances

- Past Research

-

- The History of Japan’s Consumption Tax: An Archive of Key Events and Documents ( –2021)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan (2021–2022)

- Digitalization of the Economy and International Taxation(-2024)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan 2(-2025)

-

Featured Content

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

-

Rice Grown in Rice Terraces

Rice Grown in Rice Terraces

-

Abalone

Abalone

-

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga