- Article

- Tax & Social Security Reform

Dissecting the Tax Schemes of Japan's "Third Force" (1)

November 5, 2012

At the end of August, the reform movement led by Osaka Mayor Toru Hashimoto released the final draft of its official platform preparatory to the national launch of Nippon Ishin no Kai (Japan Restoration Party). If the party makes a strong showing in the coming general election, as many predict it will, its reforms could have a profound impact on Japan's domestic economy and the lives of its people. And while Hashimoto has indicated that the Ishin Hassaku ("Eight-Point Restoration Plan") is not an election manifesto, it is all we have at this point to judge the economic policies advocated by a group that hopes to emerge as a "third force" in national politics.

Unfortunately, while the platform is long on such neoliberal principles as small government and individual self-reliance, it offers neither a clear economic vision nor specific measures for meeting Japan's immediate challenges. Nonetheless, my hope is to make use of the material available to shed some light on the substance and merit of the party's economic platform as it stands.

Overview

The Ishin Hassaku is strangely silent when it comes to numerical goals and concrete strategies for economic growth. The platform does call for boosting competitiveness on the supply side and promoting participation in free trade agreements, such as the Trans-Pacific Partnership. But the largest economic impact would doubtless come from the decentralization of public administration through a new regional system that would replace the 47 prefectures with about a dozen fiscally autonomous doshu jurisdictions.

Like the two major mainstream groups (one centered on the ruling Democratic Party of Japan and the other on the Liberal Democratic Party and its longtime partner, the New Komeito), the JRP seeks to set a timetable for achieving primary balance in the budget, to correct inequities in the tax burden between and within generations, to clarify the relationship between the burdens and benefits of public programs, and to rationalize and streamline social security disbursements. None of these ideas are particularly novel.

However, the platform does put forth some tax ideas that deserve closer scrutiny.

First, it calls for an "accurate tracking of personal income and assets (flow and stock) through a comprehensive national identification number system" to facilitate a new "emphasis on taxation of assets, not just flow." Under the heading of social security, it calls for "a guaranteed minimum calculated by income and assets combined" and "a limit on social security payments to individuals with income and assets." In these proposals the party sets itself apart with a commitment to rebuild the tax and social security systems with the help of a mechanism for accurately determining the value of each citizen's assets.

Also noteworthy under the categories of taxation and social security are its calls for "a negative income tax/basic income approach" and a "radically simplified tax system, i.e., a flat tax."

Finally, the document speaks of "turning the national consumption tax into a local tax and instituting an interregional fiscal adjustment system," while "abolishing the distribution of national tax revenues to local governments." The last two items are clearly oriented to the eventual adoption of a decentralized doshu system of regional administration.

These tax reforms, while not fully fleshed out, are by far the most concrete economic proposals the JRP offers. This reflects the basic thrust of the party's platform, which focuses on the adoption of a decentralized doshu system and the construction of a new tax system to raise the revenues required for such a system. In the following, I will examine these proposals one by one.

Negative Income Tax/Basic Income Approach

The term "basic income" calls to mind welfare systems that guarantee each individual a sum of money deemed necessary to maintain a basic standard of living. However, in the latest version of the Ishin Hassaku, the party makes clear that it is not proposing a new benefit but rather a system guaranteeing a minimum after-tax earned income.

The term "negative income tax" is potentially misleading as well. In its pure form, the negative income tax—as advocated by US economist Milton Friedman in conjunction with a flat tax—offers cash benefits to all those who earn less than the minimum taxable income, with the benefits calculated by applying the same tax rate to the shortfall. However, by inserting the qualification "income according to effort" in parentheses, the platform seems to suggest that this cash benefit would be available only to those who are gainfully employed. This suggests the party envisions a refundable tax credit, such as the US Earned Income Tax Credit (EITC) or the British Working Tax Credit (WTC).

As it happens, I have studied refundable tax credits, including the earned income tax credit, for over 10 years, and in 2010 I drew up a Tokyo Foundation policy proposal recommending the adoption such a tax credit. (See " From Cash Handouts to Refundable Tax Credits .") Today, with the working poor posing a growing problem for Japanese society, the nation must begin replacing its safety net with something akin to a springboard. When people slip and fall out of the market economy, we must not merely catch them but provide vocational and job training to return them to the economy again. Tax and welfare policies should also be instituted that provide incentives to work and ensure that those who do work can live decent lives (the workfare concept).

Flat Tax

While the term flat tax is sometimes used to refer to a single-rate income tax, scholars usually reserve it for something similar to the Hall-Rabushka flat tax. This system, which had a considerable influence on the US tax reforms implemented during the second term of President Ronald Reagan (1986–90) and continues to attract many proponents, is basically a single-rate consumption-based tax computed on the basis of value added. Since the Ishin Hassaku equates its "flat tax" with "a radically simplified tax system," it seems reasonable to assume that it is envisioning something along the lines of the Hall-Rabushka flat tax, rather than a single-rate income tax.

Let us examine how such a system works. Tax is levied on two types of added value generated by capital—individual wages (generated by human capital) on the one hand and corporate profits and interest income on the other. At the personal level, wages are taxed at a single rate, and at the corporate level, that same rate is applied to interest income and profits. Advocates claim that the system is simple enough to allow each American taxpayer to file a return using a single postcard.

Under this system, individuals are not taxed on interest income, dividends, or capital gains. This eliminates the "double taxation" of the same earnings at the corporate level (as profits) and the personal level (as dividends). Exemptions based on household structure, together with a minimum taxable income, give it a degree of progressivity.

At the corporate level, businesses would compute their taxes by deducting employee wages and benefits, allowable purchases, and capital investment from business revenue. The system encourages capital investment by allowing businesses to deduct the full cost of plant and equipment purchases, doing away with complicated annual depreciation schedules. On the other hand, it does not treat interest payments as a deductible expense.

The basic objection to a flat tax is that a single tax rate can exacerbate income and wealth disparities. This is the rationale for pairing such a tax with a refundable tax credit that offers cash benefits for low-income individuals or households.

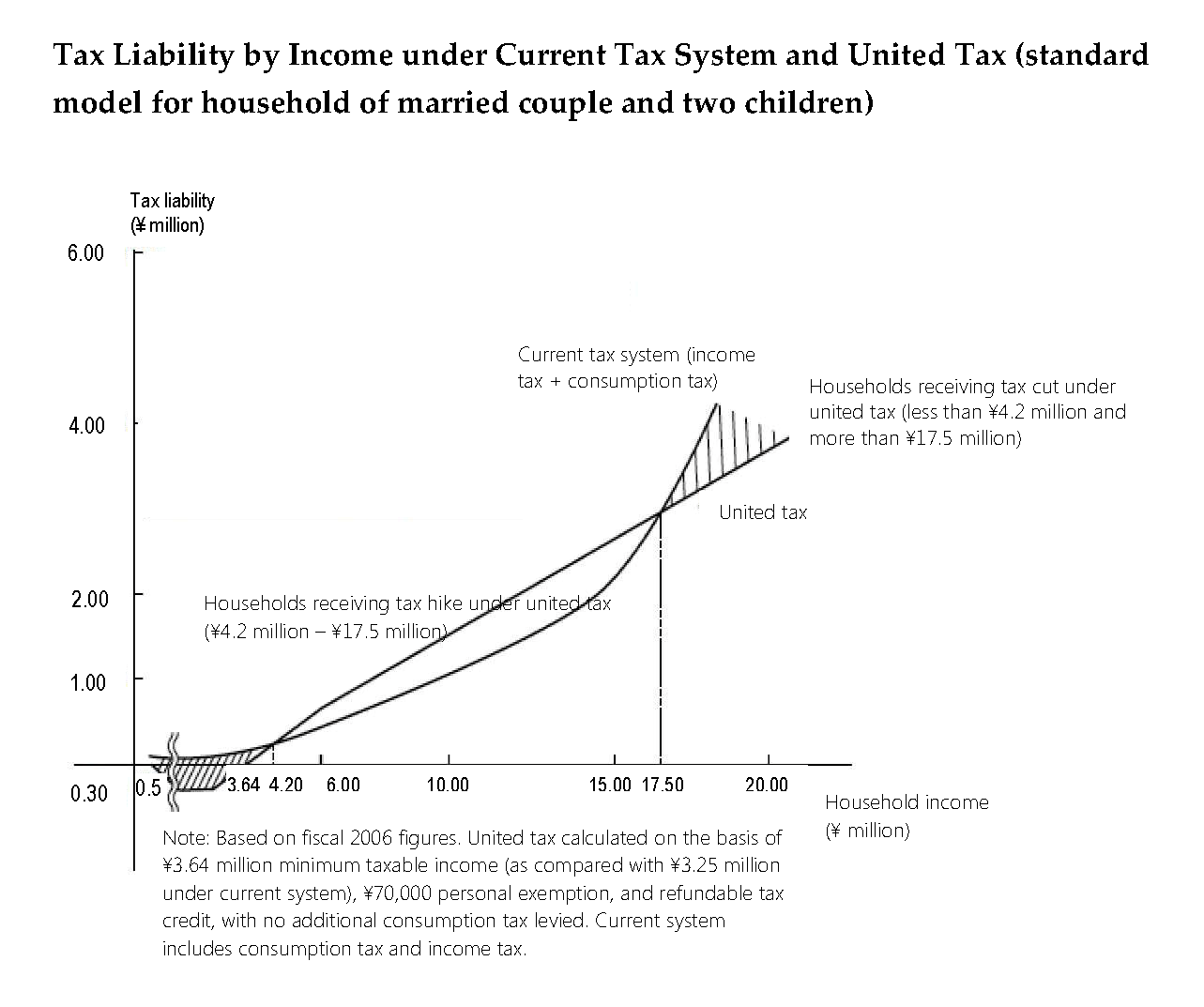

In 2008, I put forth just such a proposal, combining a flat tax with a refundable tax credit. I dubbed my tax system a "united tax," since it integrates the income and consumption taxes. The accompanying figure compares the annual taxes owed by households at different income levels under the current system and under the proposed united tax with the rate set so as to maintain the same level of tax revenues.

As the figure indicates, the united tax would reduce the overall tax bill for families with incomes up to 4.2 million yen (two-parent, two-child household), offering an incentive to work, even at lower income levels. Households earning more than 17.5 million yen annually would also benefit by a substantial reduction in the marginal tax rate, increasing their incentive to earn. However, families earning between 4.2 million yen and 17.5 million yen would see an increase in taxes. It can be anticipated that much of this added burden would be offset by the tax system's stimulatory effect on the economy. However, since the immediate result would be a tax increase for large numbers of middle-income households, winning support for such a reform could take some time.

Be that as it may, at a time of persistent economic stagnation, the JRP should be applauded for inserting a new perspective into the discussion.

-

-

- SENIOR POLICY RESEARCH OFFICER

- Shigeki Morinobu

- Shigeki Morinobu

- Areas of Expertise

-

- Tax and fiscal policy

- local finances

- Past Research

-

- The History of Japan’s Consumption Tax: An Archive of Key Events and Documents ( –2021)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan (2021–2022)

- Digitalization of the Economy and International Taxation(-2024)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan 2(-2025)

-

Featured Content

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

Japanese Honeybee

Japanese Honeybee

-

The Perilous Decline of Japanese Agriculture

The Perilous Decline of Japanese Agriculture

-

Addressing Japan’s “drug loss – drug lag”: An analysis and proposals for revamp

Addressing Japan’s “drug loss – drug lag”: An analysis and proposals for revamp

-

Cracking Down on Digital Tax Avoidance

Cracking Down on Digital Tax Avoidance