- Review

The Future Outlook of the Chinese Economy at a Turning Point

December 17, 2025

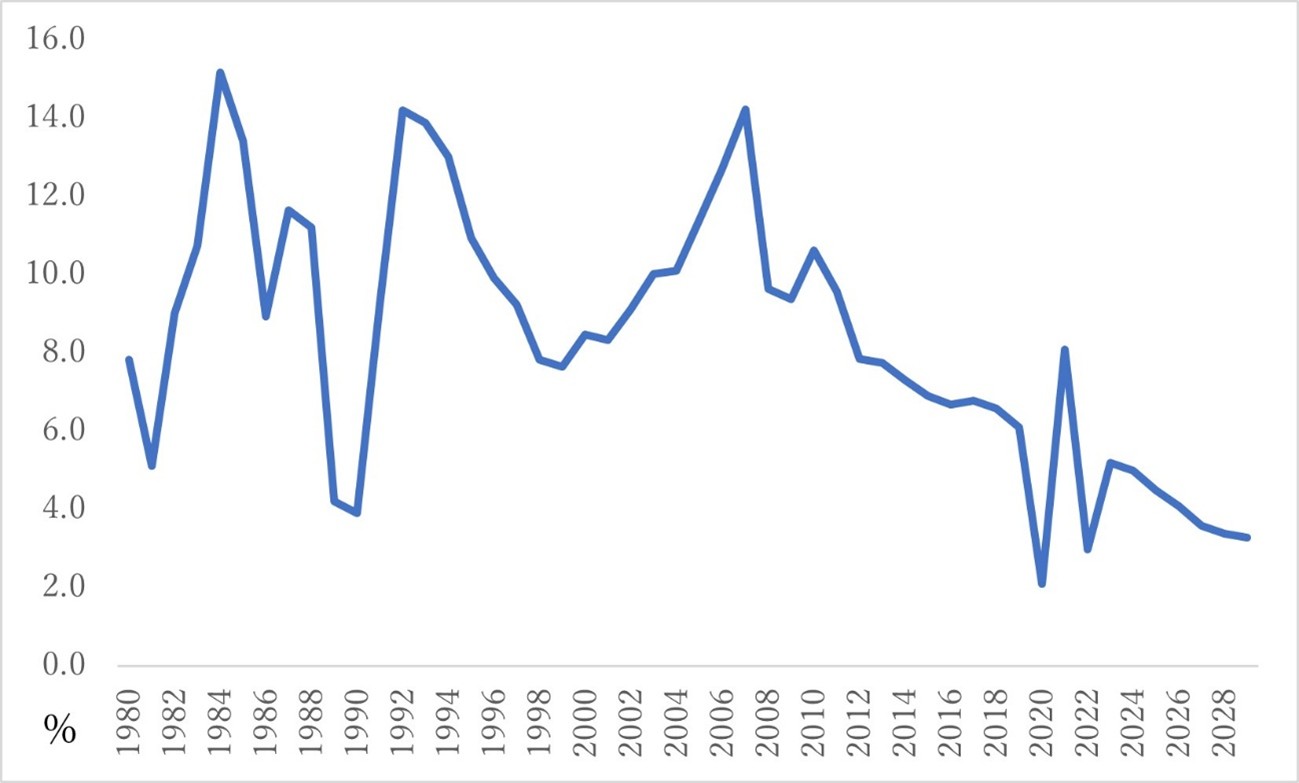

Under the Xi Jinping administration, the Chinese economy has come to a turning point. Xi Jinping was elected General Secretary of the Communist Party in 2012, and the Xi administration officially began at the National People's Congress (NPC) in March 2013. Since then, the growth of the Chinese economy has continued to slow (see Figure 1). The three-year COVID-19 pandemic from 2020 to 2022, in particular, accelerated this slowdown.

Figure 1: Trend in China’s Real GDP Growth Rate

Note: Figures from 2025 onward are based on the IMF’s Outlook.

Source: Prepared by the author based on data from the National Bureau of Statistics of China and CEIC.

This inability of the Chinese economy to return to a recovery trajectory is largely due to a "triple whammy": 1) the aftereffects of the COVID-19 pandemic, 2) the prolonged real estate downturn, and 3) the Trump-era tariff war. More fundamentally, however, the decline in economic growth was triggered by the Xi administration’s emphasis on state-owned enterprises—its so-called guojin mintui policies: advancing the public sector at the expense of the private sector—and stronger state control over the economy.

Despite this significant slowdown in the growth of the Chinese economy, the Xi administration shows no sign of steering toward liberalization, suggesting little prospect of a recovery in the near term. The Xi administration must maintain economic growth to underpin its legitimacy. In this sense, it is crucial for China to shift policies back toward liberalization to return the economy to a growth trajectory. Yet the Xi administration continues to strengthen economic control. As a consequence, market mechanisms do not function properly, and the macroeconomy appears to be becoming increasingly inefficient. This has led to concern that the Xi administration will face a serious dilemma if this situation continues.

In this article, I will clarify the substance of the three factors weighing on China’s economic growth and forecast the outlook for the Chinese economy as it approaches this critical turning point.

History of the Chinese Economy under the Xi Administration[i]

The gradual liberalization of private entrepreneurship after the launch of the Reform and Opening Up policy in 1978 was a key factor that enabled the Chinese economy to progressively recover from the brink of collapse after the death of Mao Zedong in 1976. Additionally, the boost from allowing foreign companies to invest directly in China, albeit with conditions attached, cannot be overlooked. In another important move, the government effectively lifted the previously strict restrictions on rural residents working in urban areas. In summary, the combination of China’s abundant surplus labor and foreign capital-driven manufacturing led to significant improvements in total factor productivity (TFP), including labor productivity, which in turn boosted the economic growth rate.

Institutional reforms were also evident in this process. First, the previously existing people's communes were effectively dismantled to increase agricultural production. In their place, the Household Responsibility System was introduced, giving farmers, in principle, the freedom to decide which crops to cultivate. Moreover, farmers were allowed to freely sell any of their produce that was not required to be delivered to the government. These reforms dramatically increased farmers’ motivation.

As part of the reform of state-owned enterprises, government functions and enterprise management were separated to reduce government intervention in management, thereby expanding the managerial autonomy of state-owned enterprises. For the first time since the founding of the People's Republic of China, bonuses were paid to the employees of state-owned enterprises, boosting worker initiative. This served as a catalyst for improvements to the management of state-owned enterprises.

During this time (the 1980s), many young people in China who had been sent down to the countryside during the Mao era returned to urban areas. However, some of these returnees had lost their urban household registration and were unable to restore it, which prevented them from finding employment in urban areas. At that time, local governments conditionally allowed these young people to start their own businesses. Most of them were restaurants or clothing stores.

Economic growth surged in the early 1980s with the launch of the Reform and Opening Up policy. Later, growth temporarily declined due to economic sanctions imposed by Western countries following the Tiananmen Square incident (1989) and the impact of the Asian financial crisis (1997), but it quickly recovered. Overall, during the 30 years from 1980 to 2010, the year of the Shanghai Expo, China’s economy achieved an extraordinary average annual growth rate of around 10%. Since 2013, however, China’s economic growth has progressively deteriorated and has yet to recover.

Damage to the Chinese Economy from the COVID-19 Pandemic[ii]

The novel coronavirus disease (COVID-19) devastated the global economy. Especially in the initial stages of the pandemic, the nature of the virus was unknown, and no effective vaccines or treatments were available. Early on, countries that claim to uphold liberalism or democracy were unable to impose blanket lockdowns because restricting people’s activities required legislative action or directives from judicial authorities. This allowed the outbreak to spread rapidly. In contrast, countries like China, where strong leadership can be exercised, were able to impose city-wide lockdowns solely based on directives from the central government, effectively controlling the spread of the virus.

Over time, the virus became more contagious, but its virulence weakened. Meanwhile, pharmaceutical companies in Europe and the United States succeeded in developing vaccines and treatments. As a result, people gradually recovered from the shock of COVID-19, and the restrictions imposed on activities were slowly lifted, subject to the requirement to wear masks. It is thought that greater freedom of movement also led to a recovery in immunity.

On the other hand, despite this decrease in the virulence of the virus, the Xi administration proceeded to mandate daily PCR tests and the use of domestically produced vaccines for the population. It was later revealed that at the time, in many local areas, although PCR test samples could be collected, the testing infrastructure was insufficient, and proper analysis could not be conducted. Under these circumstances, the requirement for PCR testing created crowded conditions, which in many reported cases actually facilitated the spread of infection.

It is also claimed that domestically produced vaccines were not sufficiently effective. Above all, repeated urban lockdowns caused severe damage to the economy. In China, lockdowns were finally lifted at the end of December 2022. It is said that a total of 4 million small and medium-sized enterprises went bankrupt during the three-year COVID-19 pandemic. As a result, youth unemployment rates remain high even today, in an example of economic “long covid.”

The Collapse of the Real Estate Bubble and the Prolonged Real Estate Recession[iii]

Real estate development is the most important engine driving economic growth for the Chinese economy. This is because urban redevelopment centered on real estate development is an economic activity with substantial ripple effects. It underpins not only the construction industry but also many other industries, such as materials, home appliances, and furniture, boosting the overall economy.

The Chinese government was also fully aware of the importance of such development. Real estate development provided a lifeline for local governments, especially. Allocating land for real estate development provided local governments with access to their own financial resources. In China, land is publicly owned. During the Hu administration (2003-2012), Premier Wen Jiabao decided that the revenue obtained from allocating land use rights would belong to the respective local governments. As a result, local governments were able to inject part of this revenue into social security funds, such as pensions, to implement measures to address the aging population.

There is certainly a strong demand for home-buying among the 30–50 age group in China, especially given the trend in Chinese society to see men’s purchase of a house as a prerequisite for marriage: if a man does not purchase a house, the woman will not agree to marry him. Because of this trend and the associated demand for housing, many Communist Party officials and domestic economists did not acknowledge the bubble in the Chinese real estate market, even though it was already evident before the COVID-19 pandemic, or confidently asserted that the bubble would not collapse.

However, it is the nature of a bubble to collapse. When the COVID-19 pandemic hit the real estate market, demand suddenly shrank. Chinese real estate developers already carried massive debts due to excessive leverage. The first player to go out was Evergrande, one of the largest developers, which defaulted in 2021. As a result, Evergrande was delisted in August 2025, and effectively went bankrupt. This is only the beginning of the collapse of China’s real estate bubble.

Accelerating Supply Chain Diversification Due to Trump’s Tariff War[iv]

It is a well-known fact that the Xi Jinping administration, established in 2013, finds it easier to deal with the U.S. under a Democratic administration than a Republican one. In particular, the sanctions targeting Chinese companies and the punitive tariffs imposed on China by the first Trump administration (Trump 1.0) must have been traumatic for the Xi administration. There is little doubt, therefore, that the outcome of the 2024 U.S. presidential election, which resulted in a second Trump administration (Trump 2.0), would have seemed like a nightmare scenario.

The Xi administration was aware that the return of a Trump administration could trigger additional sanctions and had likely made some preparations for them. As it turned out, however, the sanctions imposed under Trump 2.0 were far more drastic than anticipated, with a tariff of 145% on imports from China. After several rounds of negotiations, the tariffs were significantly reduced, but a provisional 30% tariff remains. Although the U.S. and Chinese governments continue to negotiate, no agreement has been reached. Meanwhile, of course, the 25% tariff imposed on China by Trump 1.0 also remains in force. Taken together, the U.S. government is effectively imposing a 55% tariff on China. The second Trump administration has also strengthened its sanctions against Chinese high-tech companies.

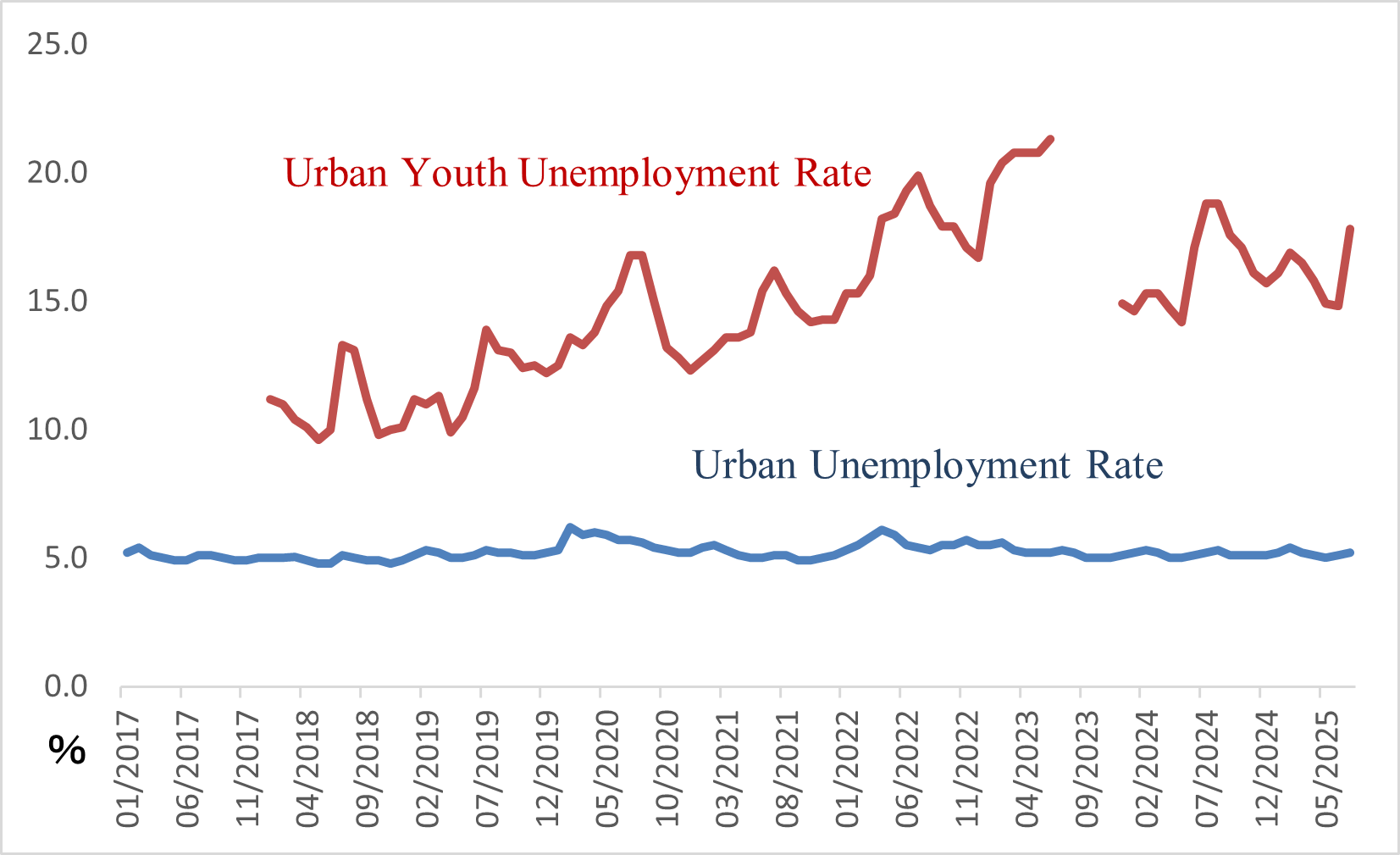

Based on these trends, China faces weakening domestic demand due to the lingering effects of the COVID-19 pandemic and the prolonged real estate slump, while external demand for its products is fettered by the Trump-era tariff war. Combined, these factors have pushed the Chinese economy into deflation, with persistently high youth unemployment (see Figure 2). At this rate, the Chinese economy is likely to experience a significant slowdown. In other words, the forces retarding economic growth are stronger than anticipated. Monetary and fiscal measures alone are insufficient to stave off a slowdown: a bold policy shift is urgently required.

Figure 2: Trends in China’s Surveyed Urban Unemployment Rate and Urban Youth Unemployment Rate

Note: The youth unemployment rate is the unemployment rate for the 16–24 age group.

Source: Prepared by the author based on data from the National Bureau of Statistics of China.

Liberalization or Tighter Control? The Dilemma Facing the Xi Administration

The Xi administration was officially launched in March 2013. With a weak power base, Xi embarked on an anti-corruption campaign to oust officials involved in corruption, systematically toppled his political rivals, and rapidly consolidated his hold on power. What is less well-known is that this period also created a fault line in Chinese politics. Because long-time leaders such as former President Jiang Zemin and former Premier Zhu Rongji had long retired, there was effectively no force within the party capable of keeping Xi’s maneuvering in check. Seeing this, Xi, to realize his own ambitions, had the National People’s Congress amend the Constitution of the People’s Republic of China in March 2018, abolishing the term limits for the presidency. Now, unless Xi voluntarily resigns as president, he can remain in power for life.

For Xi Jinping, anti-corruption campaigns have been the most effective means of ousting political rivals. Today, only seven years since the constitution was amended, it seems that Xi’s rise to complete one-man dominance has been achieved. There is now no one in the leadership of the Chinese Communist Party who can say no to Xi Jinping. Many liberal intellectuals critical of the Xi administration have also become unable to speak out within China. Moreover, the official media in China only report propaganda glorifying President Xi. These factors have led to concerns that the Xi era marks the end of around four decades of China’s Reform and Opening Up, and is dragging the country back to the era of Mao Zedong.

About 40 years ago, Deng Xiaoping and other leaders known as the Eight Elders, wary of a return to the Mao era, banned the cult of personality previously attached to China’s leaders. Deng himself was the most powerful figure at the time, but he refused to accept any personal idolization. A cult of personality surrounding a leader can lead to the deification of that leader. Looking back at the situation at the time, Mao Zedong was perceived more like a god than a human leader. In contrast, Deng Xiaoping portrayed himself not as a god, but simply as a leader.

In this historical context, can Xi Jinping ever become a god? The answer is no. Xi encourages worship of himself to strengthen his power base. However, he does not possess the same level of authority as Mao Zedong, and therefore will never be idolized in the same way. Moreover, present-day China is vastly different from the Mao era, and a large amount of information flows in from overseas—an inconvenience that has led the Xi administration to strengthen the firewall and strictly control undesirable information.

Certainly, there are several political scenarios in which strong leadership is required. One of these was responding to the COVID-19 pandemic. The problem is that in a market economy, information symmetry is essential for the market mechanism to allocate resources efficiently. Strict information control by the central government has led to inefficiencies in resource allocation, which is dragging on China’s economic growth rate. Meanwhile, this decline in economic growth undermines the legitimacy of the Xi administration, and concern over this issue has led the administration to attempt to tighten information control even further. This is the dilemma that the administration faces.

Outlook for the Chinese Economy

The internal structure of China’s economy has undergone significant changes over the past twelve years since the Xi administration came to power. First, the credit order in society has collapsed. This is because trust in the government has become untenable. A social order based on trust is the foundation of any market economy: when this financial order based on trust collapses, the economy ceases to grow. At the same time, Xi Jinping himself has repeatedly emphasized the government’s policy to enlarge and strengthen state-owned enterprises. Meanwhile, the government is enforcing ever-tighter regulations on private enterprises, which are likely to become increasingly weakened under this pressure. If it were really possible to strengthen state-owned enterprises, then there would have been no need for the Reform and Opening Up policy four decades ago. Today, China is already the world’s second-largest economy, and it needs to upgrade its industrial structure. Currently, government-led innovation is being reinforced, but bottom-up innovation by the private sector is becoming increasingly anemic. This focus on government-led, top-down innovation risks causing a mismatch in resource allocation.

In the short term, returning to growth requires overcoming the “triple whammy”: the aftereffects of COVID-19, the prolonged real estate downturn, and the Trump-era tariff war. The Xi administration has provided massive financial subsidies, but most of these are aimed at supporting producers. There has been a dearth of policies to boost the income of low-income groups, leaving personal consumption weak. This is likely because, unlike Western countries with democratic electoral systems, China’s government does not feel compelled to rescue the people in the low-income bracket, who it should theoretically represent. In a sense, this government stance is due to China’s political system.

The Chinese economy is huge, and it is unlikely that its collapse is imminent. However, because of this, there is a strong concern that those in power may not fully see where the problems lie. In summary, the Chinese economy is broken, but it will likely take time for it to collapse.

[i] Ke, Long (2021) Neo-China Risk Research, Keio University Press.

[ii] Haiqiang Chen, Wenlan Qian, Qiang Wen “The Impact of the COVID-19 Pandemic on Consumption: Learning from High-Frequency Transaction Data” AEA Papers and Proceedings vol.111, May 2021 (pp. 307–311).

[iii] Ke, Long (2024) China’s Real Estate Bubble, Bunshun shinsho.

[iv] Ke, Long (2025) Trump’s Tariffs Will Damage the World Economy…! Now is the Time for Japan to Look Ahead to the “Post-Trump” World, Modern Business.

-

-

- RESIDENT FELLOW

- Long Ke

- Long Ke

- Areas of Expertise

-

- Development finance

- Chinese economy

- Research Project

-

Featured Content

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

-

Rice Grown in Rice Terraces

Rice Grown in Rice Terraces

-

Abalone

Abalone

-

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga