C-2021-001-5-WE

Less than 10 years remain until 2030, the target year for achieving the Sustainable Development Goals (SDGs). In moving toward the realization of a sustainable society, the corporate sector needs to raise its engagement in CSR activities to a higher level through “goods and services that address social issues,” “business processes that have less impact on society,” and “donations, volunteering, and other social contribution activities.” These initiatives should also be spontaneously undertaken by individual businesses to enhance their own sustainability and competitive advantage.

In the 2019 CSR White Paper published by the Tokyo Foundation for Policy Research, I introduced the notion of an “SDG loop” that links five interrelated concepts: SDGs, ESG, CSR, creating shared value (CSV), and sustainability. I believe a broad understanding of these five concepts will help build consensus and facilitate decision-making among stakeholders toward the realization of a sustainable society. In the following, I will clarify the SDG loop concept by elucidating the meaning and roles of ESG, CSR, and CSV. In addition, as awareness of “social contribution activities” as a management issue gains momentum—alongside “goods and services” and “business processes”—I will discuss the notion of “digital philanthropy” that is emerging from the confluence of the SDGs and digital transformation.

1. SDG Loop

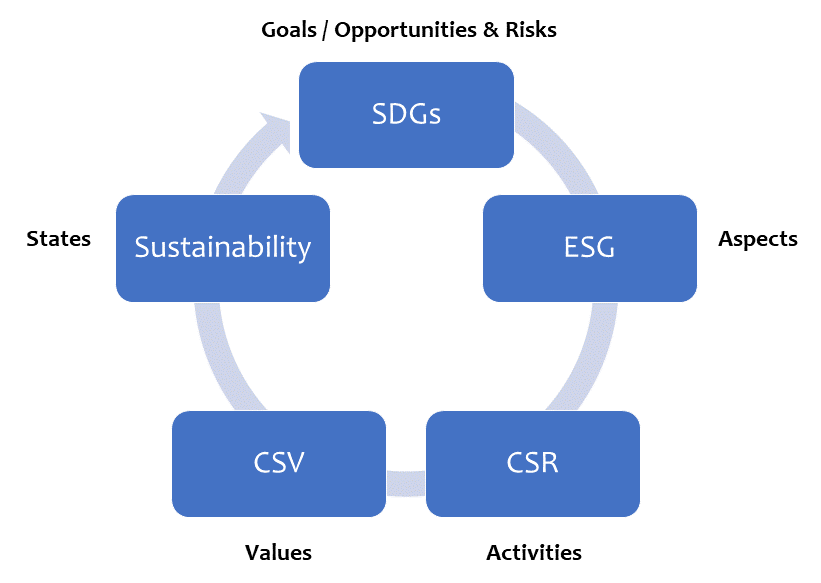

The SDG loop represents companies’ efforts to achieve sustainability for both society and themselves, starting from and returning to the SDGs and then progressing to the next stage. It is a tool that can help identify the respective aims and roles of various interrelated concepts so businesses can undertake ESG management and CSR activities in a consistent manner (Figure 1).

Figure 1. SDG Loop

Source: Created by the author.

Companies can use the loop as follows: Refer to the SDGs to ascertain risks and opportunities: undertake management that addresses environmental, social, and governance concerns; fulfill their corporate social responsibilities to stakeholders; thus creating social and corporate value; enhance social and their own sustainability; and thereby contribute to the achievement of the SDGs.

Main Issues

Issue 1: “ESG-Conscious Business Process” and “ESG-Oriented Business”

ESG originally referred to the three criteria (environmental, social, and governance) that financial institutions used to determine where to place their assets. It should be noted that rather than ESG-conscious business processes or using ESG criteria to minimize business process risks, financial institutions look to the opportunities that ESG-oriented businesses offer in generating profits.[1] In advancing ESG management, therefore, companies must keep the interests of financial institutions in mind and adopt strategies that are conducive to generating profits. Many surveys by global ESG research organizations are structured so that the narratives, scenarios, and evidence can be used to identify the degree of corporate value a company creates through ESG management over the short, medium, and long term. Japanese companies have a tendency, though, to focus on the risk-averting aspects of ESG, rather than the opportunities it offers for profit generation.

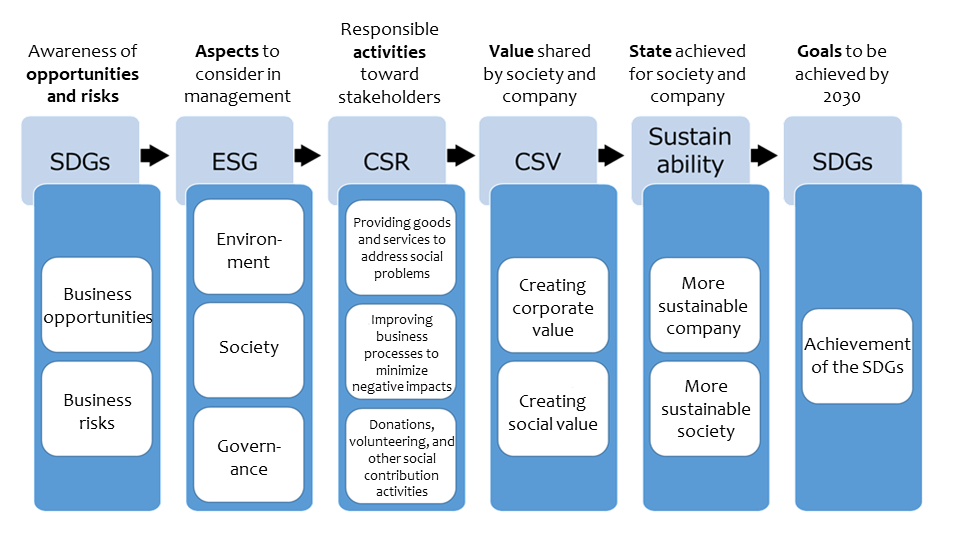

Figure 2. Goods and Services, Business Processes, and Social Contribution Activities

Source: Created by the author.

Issue 2: “Broad Definition of CSR” and “Narrow Definition of CSR”

As mentioned above, CSR consists of “providing goods and services that address social issues” as part of the company’s core operations; “improving business processes to reduce the company’s negative impact on society,” thereby internalizing external diseconomies; and “making donations, volunteering, providing resources for civil initiatives, and doing other social contribution activities” that can result in increased corporate value (Figure 2).

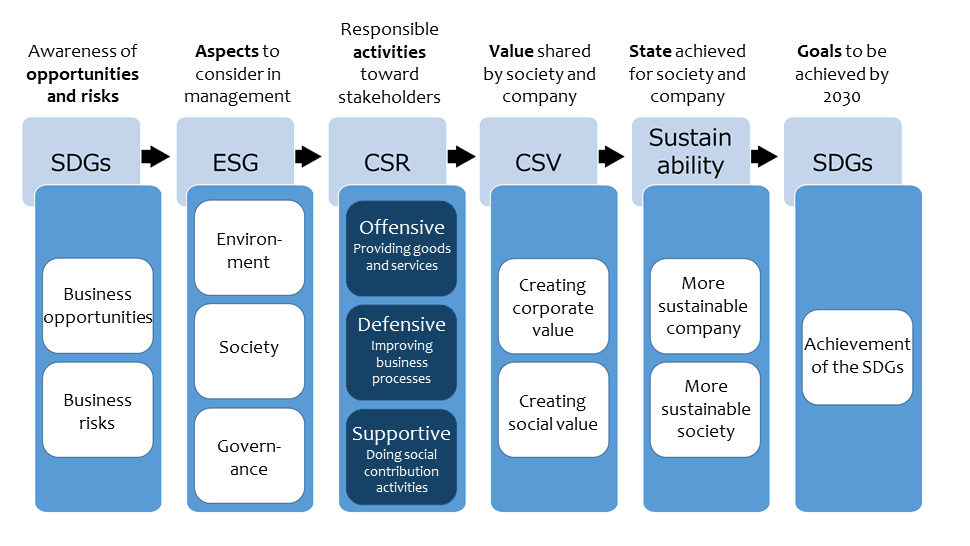

Until 2010, addressing social issues through the provision of goods and services was considered offensive CSR, while reducing a company’s negative impact was seen as defensive CSR.[2] Social contribution activities, meanwhile, were sometimes called supportive CSR, since they were aimed at assisting socially vulnerable groups or promoting cultural and artistic endeavors (Figure 3).[3]

Figure 3. Offensive, Defensive, and Supportive CSR

Source: Created by the author.

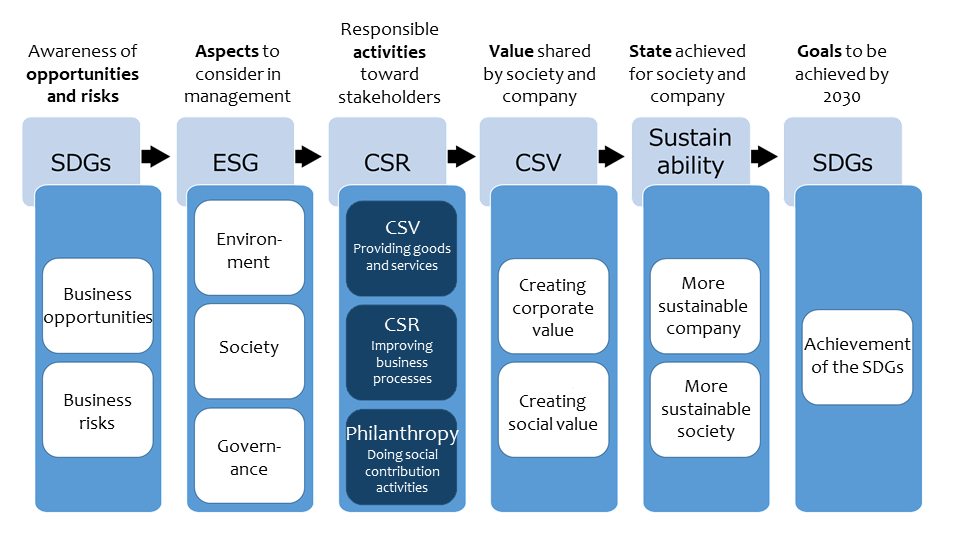

However, after Michael Porter and Mark Kramer published “Creating Shared Value” in the January/February 2011 issue of the Harvard Business Review,[4] the provision of goods and services that contribute to resolving social issues came to be described as CSV—an offensive form of CSR. Activities to improve business processes and mitigate any negative impacts were denoted as defensive CSR. And donations, employee volunteering, resource provision, and other supportive activities were referred to as social contribution activities or—depending on the preferred terminology of each company—philanthropy, corporate citizenship, community relations, or social support activities. As a result, CSR came to take on two meanings: In the broad sense, it referred to the original collection of these three activities, while in the narrow sense, it described only the defensive CSR, including respect for human rights, environmental protection, corporate governance, ethics and compliance, and risk management (Figure 4). Some Japanese managers failed to distinguish between the broad and narrow definitions of CSR, however, embracing CSV while deprioritizing social contribution activities.

Figure 4. CSV, CSR, and Philanthropy: Three Dimensions of Corporate Social Responsibility

Source: Created by the author.

Issue 3: “CSV as an Activity” and “CSV as a Value”

In discussing CSV as both an activity and as a value, I would like to relate two personal anecdotes. Concerning the former, allow me to share Michael Porter’s responses to a question I posed to the Harvard Business School professor during the May 2013 Global Shared Value Leadership Summit in Boston, as follows:

• The advent of CSV will not diminish the importance of CSR and social contribution activities .

• Until then, though, companies did not have sufficient interest in addressing social issues through their profit-making operations, which presumably are their biggest strengths.

• The idea of CSV was thus introduced to focus the attention of private companies on the goods and services with the greatest impact on the creation of social and corporate value.

This gave me new insights into the importance of CSV as an activity. In addition to offering donations and having employees volunteer their time, companies can address social issues by reviewing their products and markets, utilizing CSV to gain an edge as part of their competitive strategy.[5]

As for CSV as a value, I was a member of a pilot program for the International Integrated Reporting Framework from 2011 to 2013 and also helped the International Integrated Reporting Council (IIRC) create a Japanese translation of the framework (issued in March 2014). Our discussions led to the inclusion of the notion of “value creation . . . for the organization and for others” in the Fundamental Concepts—“others” here referring to stakeholders and society as a whole.[6] CSV is thus embedded at the heart of the value creation process of integrated reporting.

2. Digital Philanthropy

The Keidanren (Japan Business Federation) One-Percent Club plays a central role in promoting the social contribution activities of Japanese companies. In its latest questionnaire of corporate members, the club defines social contribution activities as follows:[7]

Activities undertaken by the company that are not directly linked to profit generation in the short term but contribute to the resolution of social issues.

This pertinently expresses the ideal form of social contribution in the era of the SDGs, when companies are expected to create positive social impact. Notably, the definition states that social contribution activities and profit generation are “not directly linked . . . in the short term,” the implication being that the two may be linked in the long term if value creation for the company (in the form of profits) contributes to value creation for society (through the resolution of social issues).

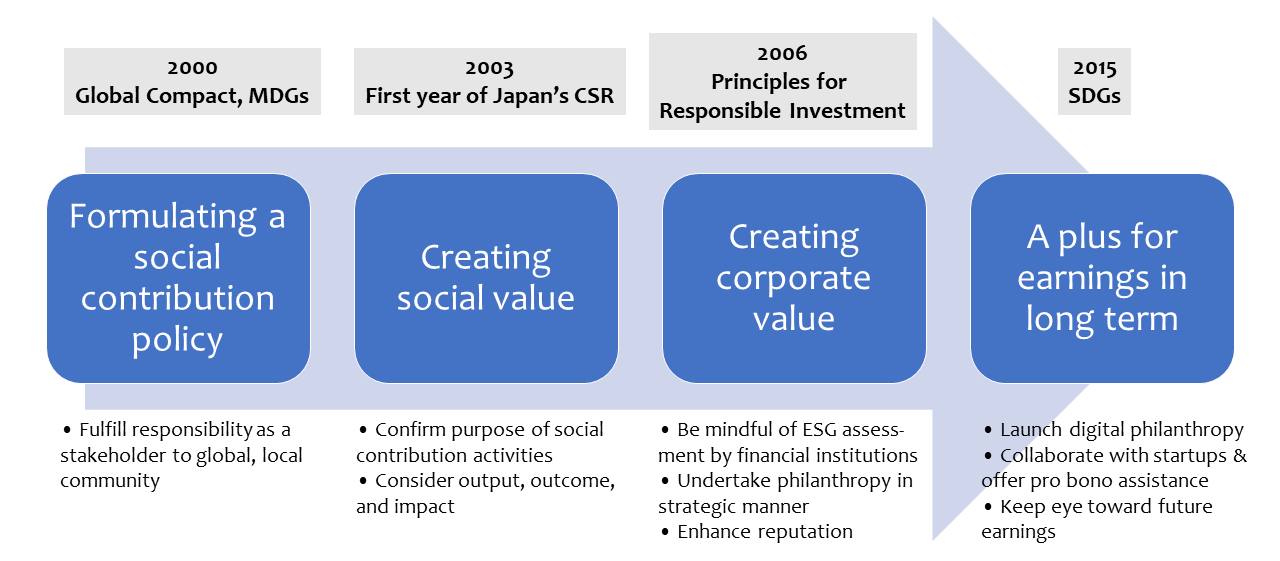

The current definition is the product of substantial discussions both inside and outside the corporate community. In the following, I will trace the main issues that have been debated since the launch of the UN Global Compact in 2000, with a focus on the meaning and features of the idea of “digital philanthropy,” which has emerged to become part of the current definition (Figure 5).

Figure 5: Changes in the Main Issues Surrounding Social Contribution Activities

Source: Created by the author.

Main Issues

Issue 1: Formulating a Social Contribution Policy

The first point was the formulation of clear policies on social contribution activities. Before 2000, many businesses implemented such activities in a passive, fixed, and ad hoc manner. For example, companies made donations only after being asked to do so; donations were often limited to well-known causes or charities; and when profits fell, contributions also decreased. Donations of money, goods, people (employee volunteers), technology, information, networks, and other corporate assets were automatically regarded as input of social contribution activities, according to management’s logic tree framework, and would have positive repercussions for social contribution statistics and rankings. Since the launch of the UN Global Compact and the adoption of the Millennium Development Goals in 2000, though, some Japanese companies, especially multinationals operating in compliance with global initiatives, began calling for an end to such conformist practices and the formulation of social contribution policies from the perspective of CSR.

Issue 2: Creating Social Value

In the face of evolving international demands, companies began focusing on how their social contribution activities could create social value. This was around 2003, which many identify as the first year of Japan’s CSR.

Social contribution activities should be undertaken to make a positive impact on society and not as an end in themselves. In reality, though, many companies that provided corporate assets simply assumed that the civil society organizations to which those assets were input would use them for the benefit of society or that the assets were helping parties overcome social challenges. From around this time, however, businesses began being called to extend their logic tree and consider output, outcome, and impact, confirming and evaluating the creation of social value through closer monitoring and disclosing their findings to society. The following indicators could be used, for example, to assess output, outcome, and impact in the healthcare and education sectors:

• Output: Information on outreach activities, such as the number of participants at a health awareness event and the number of textbooks distributed or children receiving the books

• Outcome: Indications of behavioral change or the resolution/mitigation of a social problem, such as the number of people who have undergone a health examination and begun receiving outpatient treatment and the degree of improvement in academic ability or the number of children who have shown improvement

• Impact: Degree of social penetration or changes produced, as measured by the launch of comparable initiatives by others and the introduction of similar support services by the government

Issue 3: Creating Corporate Value

In 2006, the Principles for Responsible Investment (PRI) were developed by an international group of ESG-oriented institutional investors to assess how the use of management resources for social contribution activities was leading to the creation of corporate value.[8] This fueled discussions on whether social contribution activities can actually create corporate value, for at the time, claims by companies to be enhancing their corporate value through their social contribution activities were still sometimes subject to ridicule. There was no hiding the fact, though, that donations, gifts, and volunteer support were highly appreciated by the civil society and community organizations that received them and that the company’s reputation, along with its standing in the community, improved as a result. Since social contribution activities can create both social value and corporate value, and with investors welcoming such activities, companies have begun to voluntarily and systematically undertake social contribution activities in a more strategic manner, such as by:

• Selecting priority areas to leverage the strengths of core business operations

• Focusing on the effective branding and ethical marketing of goods and services

• Selecting partners with complementary strengths

• Undertaking effective communication, including through advertising

Issue 4: A Plus for Earnings in the Long Term

Inherently, though, shareholders and investors tend to see greater value in a company’s ability to provide goods and services to the market and generate profits from sales, more so than in its reputation, motivated workforce, recruiting skills, or broad financing options. It was not until the adoption of the SDGs in 2015 that the focus shifted to social contribution activities that were linked to long-term profits. Until then, companies were “expected” to provide goods and services that addressed social problems as part of their profit-making operations; but now they were more or less “obliged” to implement measures to help build a sustainable society. Given the many threats to the sustainability of human society—global warming, a crippling pandemic, pervasive poverty, and growing inequality—it would be naïve to position social contribution activities merely as goodwill gestures made without thought to profit. The key here is to consider long-term implications. Through their social contribution activities, companies may be able to enhance their ability to discover, understand, and address societal challenges, as well as to develop networks of civil society partners. Such assets will no doubt greatly facilitate the development and marketing of goods and services that mitigate social problems for years to come. Such goods and services may first be provided for free on an experimental basis and later brought to market with enhanced quality and problem-solving features within a few years.

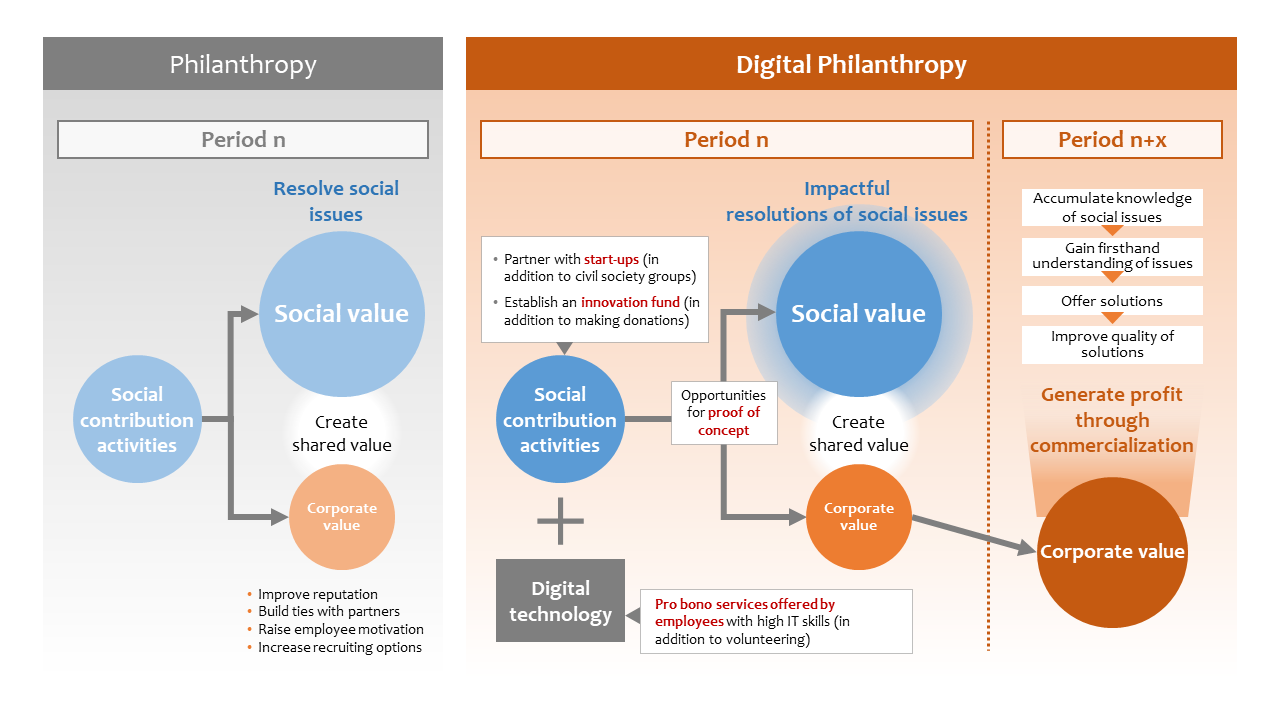

Figure 6: Conventional versus Digital Philanthropy

Source: Created by the author.

What is “Digital Philanthropy”?

The latest manifestation of social contribution activities in the era of the SDGs and digital transformation (which in Japan is sometimes referred to as Society 5.0) is “digital philanthropy.” Here, I will use the term to mean “social contribution activities that aim to maximize social and corporate value through the use of digital technology.” Digitalization is expected to play an increasingly important role in implementing SDG-related initiatives aimed at “leaving no one behind” and creating “social impact” (Figure 6).

In the abovementioned Keidanren questionnaire conducted in 2020, 112 out of 178 companies said that they were using digital technology for their social contribution activities. Although digital philanthropy is an evolving concept, real-world examples point to the following features:[9]

Main Features

Feature 1: Partnering with Start-Ups

Until now, companies generally provided management assets to civil society groups addressing a variety of community issues and working toward their resolution, either helping with specific projects or furnishing general organizational support. Start-ups aiming to tackle social challenges through the use of digital technology are now being launched around the world, and they are fast emerging as key partners for the corporate sector in its digital philanthropy initiatives.

Feature 2: Subsidizing Digital Solutions

Corporate foundations and other organizations have traditionally provided nonrepayable financial assistance in the form of research and development grants and have played a major role in addressing society’s needs through the promotion of technology. Today, innovation funds are providing nonrepayable subsidies for initiatives that require the use of AI and other digital technologies to help resolve societal challenges. Typical of such initiatives is Microsoft’s AI for Good[10] project, which supports innovative civil society groups and start-ups with a budget of $165 million over five years.[11]

Feature 3: Supporting Proof of Concept

Companies that make social contributions to civil society organizations in the form of grants generally expect the recipient to produce an output of some kind or achieve a level of outcome that enhances social value, such as by resolving or alleviating problems faced by certain groups, within a certain timeframe. In the case of digital philanthropy, however, many companies regard their contributions to civil society and start-ups as opportunities for those groups to try out new technologies, products, and services. Even if a grant does not lead to tangible results, the knowledge gained from running proof of concept (PoC), including their failures, will become an asset for those involved that may bear fruit in future endeavors. In the 2020 Keidanren questionnaire, 37 out of 178 respondents stated that they were “implementing PoC with an eye toward commercialization”[12]—a result not seen in the 2017 survey.

Feature 4: IT-Related Pro Bono Services by Employees

Leading sustainable companies encourage their employees to volunteer their time at civil society organizations,[13] a strategy that could prove valuable to the long-term growth of those companies as it enables them to accumulate firsthand knowledge of social issues. Of particular importance in digital philanthropy are the pro bono services offered by employees with high IT skills. Such services have also been offered virtually since the outbreak of COVID-19. NTT DATA, for example, has been supporting the development of “social technology officers”[14] since fiscal 2019 to provide IT advice to civil society groups and to promote fuller IT utilization. To date, about 20 NTT DATA employees have offered their expertise under this project on a pro bono basis.

When considered from a broad, dynamic, and long-term perspective, the boundaries between corporate activities aimed at generating profits and those undertaken as social contribution activities become quite blurred. In the era of Society 5.0, when the use of digital technology is expected to become the norm, companies hoping to achieve sustainable development by being part of the solution to societal challenges will increasingly need to partner with civil society groups and start-ups to implement digital philanthropy as part of their social contribution activities.

Translated from “SDGs rupu to dejitaru firansoropi,” CSR hakusho 2021, Tokyo Foundation for Policy Research.

[1] Especially for B2B companies, this can take the form of a business that supports client governance, such as offering a comprehensive ESG information management system or undertaking consulting services for strengthening governance.

[2] Keizai Doyukai (2007), Social Responsibility Management Promotion Committee Report, “CSR Innovation: Creating New Value through CSR through Business Activities,” p. 6.

[3] Other classifications also exist. One is to incorporate social contributions into the domain of “dynamic CSR” and to contrast these activities with “preventive CSR.” A second is to split “preventive” measures into those aimed at complying with hard law and those adhering to soft law, giving a total of four CSR categories.

[4] Michael E. Porter and Mark R. Kramer (2011), “Creating Shared Value,” Harvard Business Review, January/February 2011, pp. 62–77.

[5] One session at the summit featured a dialogue between Nestlé’s chairman, who successfully promoted CSV as a competitive strategy, and Michael Porter. See Takehiko Mizukami’s blog, “Shared Value Summit,” May 27, 2013, https://www.cre-en.jp/mizukami-blog/?p=849#.YVVrcjHP1so (accessed October 5, 2021).

[6] “International Integrated Reporting Framework: Japanese Translation,” p. 11, https://integratedreporting.org/wp-content/uploads/2015/03/International_IR_Framework_JP.pdf (accessed October 5, 2021).

[7] Keidanren, “e Survey Results on Social Contribution Activities,” September 15, 2020, p. 1, http://www.keidanren.or.jp/policy/2020/078_honbun.pdf (accessed October 5, 2021).

[8] See Principle 3: “We will seek appropriate disclosure on ESG issues by the entities in which we invest,” Principles for Responsible Investment, p. 6, https://www.unpri.org/download?ac=10948 (accessed February 25, 2022).

[9] For details regarding NTT DATA’s tuberculosis AI diagnostic imaging access project, see the Nikkei ESG website, https://project.nikkeibp.co.jp/ESG/atcl/column/00007/092700033/ (accessed October 28, 2021).

[10] https://www.microsoft.com/ja-jp/ai/ai-for-good (accessed October 5, 2021).

[11] NTT DATA INSIGHT website, Digital Philosophy: AI Social Strategy for Creating Corporate Value, April 7, 2021, https://www.nttdata.com/jp/ja/data-insight/2021/0407/ (accessed October 5, 2021).

[12] Keidanren, “Questionnaire Survey Results on Social Contribution Activities,” September 15, 2020, p. 3, http://www.keidanren.or.jp/policy/2020/078_honbun.pdf (accessed October 5, 2021).

[13] IBM Corporate Service Corps, https://www.ibm.com/ibm/history/ibm100/jp/ja/icons/corporateservicecorps/, GSK PULSE, https://jp.gsk.com/jp/responsibility/our-people/employee-volunteering/, etc. (accessed October 5, 2021).

[14] The project’s three owners are the Japan NPO Center, Code for Japan, and ETIC. See https://www.jnpoc.ne.jp/?p=19357 (accessed October 5, 2021).