- Article

- Industry, Business, Technology

Integrating CSR into Strategic Management: A Practitioner’s Perspective

March 12, 2015

Koichi Kaneda

CSR Head, Corporate Communications & Public Affairs, Takeda Pharmaceutical Co. Ltd.

How extensively have Japanese companies integrated CSR into corporate management? Koichi Kaneda, senior director for CSR at Takeda Pharmaceutical, examines the evolution of CSR in Japan as it relates to three key categories of corporate social responsibility: the provision of goods and services, enhancement of business-process integrity, and corporate philanthropy.

* * *

Pinning down the meaning and substance of “corporate social responsibility” is no easy task. Expectations vary from one locale to another and evolve over time. Indeed, even at any given time and place, society (the object of social responsibility) is apt to interpret CSR differently from businesses (the practitioners). Companies may modify their CSR programs and policies as they become cognizant of these discrepancies, but by the time the changes go into effect, society’s concept of CSR is likely to have evolved further. Closing the gap is an ongoing challenge—which helps explain why CSR has been described as an “endless journey.” Still, striving continuously to meet that challenge is an important key to gaining a “ticket to operate” over the long term. Moreover, by further integrating CSR policy into strategic management, companies can enhance their sustainability.

In the following, I survey the process by which Japanese companies have integrated CSR into corporate management, drawing from my own experience as a CSR officer at Takeda Pharmaceutical and other private companies. I examine this process as it pertains to the three key categories of corporate social responsibility—the provision of goods and services, enhancement of business-process integrity, and corporate philanthropy (referred to as “corporate citizenship activities” at Takeda)—as well as to the disclosure and reporting of CSR information (see Figure 1). In this way, I hope to provide a broad overview of the evolution of CSR in Japan from 1999 to the present.

Figure 1. Relationship between CSR and Sustainability at Takeda

Provision of Goods and Services

The business community takes the position that the provision of goods and services (the first category of CSR) is a social responsibility unique to the private sector, a responsibility that neither the government nor the nonprofit sector can perform.

As the business community sees it, the pursuit of core business activities in itself fulfills an important responsibility to society, most especially to clients and consumers, who are among the diverse stakeholder groups that make up society. Some in the civil sector take issue with this view, questioning the logic of equating day-to-day business operations with social responsibility and dismissing it as a way of justifying profit-driven behavior. Here the gap between the two sectors’ concept of responsibility appears in sharp relief.

Regardless of one’s position on this issue, there is no doubt that the provision of goods and services lies at the very heart of business activity. Since this is the case, one might argue that there is no need to discuss its integration into strategic management, since it is an integral part of strategic management to start with.

But one important way in which Japanese companies have integrated CSR into strategic management in recent years is by exploring ways of enhancing the social value of their commercial goods and services. This trend has received a major push from the “creating shared value” (CSV) movement pioneered by Harvard University Professors Michael Porter and Mark Kramer. Porter and Kramer have made the case that corporations can simultaneously create business value and social value by treating social challenges as latent market needs that present business opportunities. I think, however, that profit-making activity must have a positive social impact—that is, make a significant contribution to the mitigation of some social problem—in order to qualify as CSV.

In 2012 and 2013, I attended a number of major international CSR conferences, including events sponsored by the United Nations Global Compact, BSR (Business for Social Responsibility), CSR Europe, and CSR Asia, with the aim of identifying material issues pertaining to social responsibility (Figure 2). The key message of all these conferences was the growing expectation that the business sector—with its ideas, technology, and capital—use these resources to exert a positive impact on society.

Figure 2. International CSR Conferences, 2012–13

Business-Process Integrity

Whatever the positive social impact of a company’s commercial goods and services, however, it counts for little if the company imposes new burdens and generates new social problems in the process of supplying them. The second category of CSR is the maintenance and enhancement of business-process integrity with an emphasis on corporate ethics and compliance with laws and standards, which constitute the heart and soul of CSR.

In 1999, UN Secretary General Kofi Annan, speaking at the World Economic Forum in Davos, called attention to the negative externalities of global business activity with respect to human rights and the environment. This marked a turning point, as global corporations, Japanese companies included, gradually realized that ethical business practices, particularly as they pertain to human rights and the environment, are integral to any effective strategy for managing risk and maintaining long-term corporate value. The trend quickly gathered momentum after 2003—often referred to in Japan as “year one of the CSR era”—with the establishment of various groups devoted to CSR and the development of global sustainability guidelines and standards.

With the recent spread of social media, expectations for business-process transparency have risen, and society’s concept of CSR has expanded dramatically in scope. Corporations have come under pressure to conduct their own value-chain analyses to measure the impact of their businesses on human rights, the environment, and other parameters and to draw up measures to prevent, correct, or counteract negative externalities. At the same time, it is fast becoming the norm to hold global corporations responsible not only for their own behavior but also for that of their external supply chains—that is, independent business entities that provide them with raw materials and parts and business partners that produce, distribute, or sell their products under contract. Lax oversight of the supply chain has cost some global corporations billions of dollars as a consequence of boycotts, strikes, and lawsuits. Such developments have accelerated the trend toward integrating business-process integrity into strategic management as a means of maintaining (that is, averting the loss of) corporate value (Figure 3).

Figure 3. Promotion of CSR Activities across the Entire Value Chain

Corporate Philanthropy

The third key area of CSR policy is corporate philanthropy, which includes direct corporate donations to charitable and social causes, programs to encourage employee volunteerism, and philanthropic activities by corporate foundations.

The face of Japanese corporate philanthropy has changed significantly in the past 15 years. In 1999, the typical Japanese corporation spent a negligible portion of its budget on such activities, and few made any active effort to target their programs to the specific needs of the community. Outside of Japan, the bulk of corporate giving was channeled into UN agencies. Within Japan, the main beneficiaries were organizations with close government ties. While some corporations communicated their contributions to the public as an integral aspect of brand management, others chose the path of “doing good by stealth.” At many companies, corporate executives and officers in charge of corporate philanthropy were reluctant to sully the “purity” of their charitable programs by treating them as an aspect of business strategy. There was still considerable debate over such questions as the propriety of seeking recognition or reward for charitable giving, the incongruity of having company programs to “encourage” volunteerism, and the pluses and minuses of maintaining separate corporate foundations. In short, the degree to which management integrated philanthropy into business strategy varied substantially from one company to the next.

Since then, however, due to pressure from shareholders and investors, more and more Japanese companies have accepted the need to explain the necessity of corporate philanthropy with a view to creating corporate value and, of course, social value as well. In recent years many companies have begun grappling with such topics as criteria for priority setting (for efficient operation of program and brand building), partnerships with nongovernmental and nonprofit organizations (with a view to gaining a fuller understanding of social issues and boosting the impact of corporate initiatives), the value of employee involvement in community affairs (from such standpoints as diversity training and employee satisfaction), and corporate philanthropy as a marketing tool (for enhancing corporate image and name recognition and cultivating future customers). In these ways, corporate philanthropy is increasingly becoming a key consideration in business management.

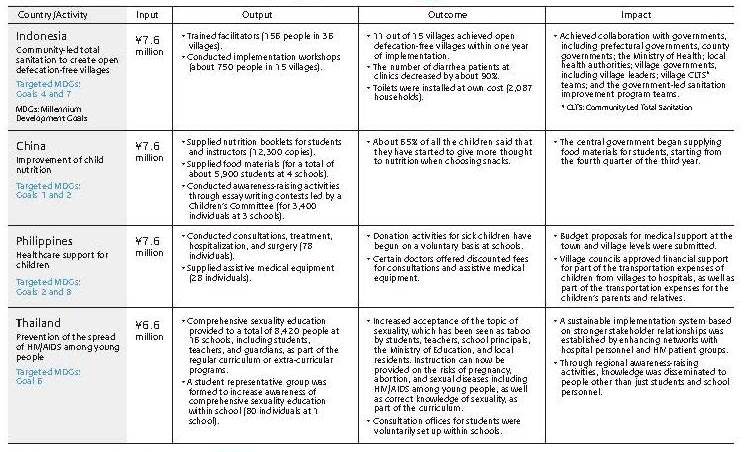

The latest trend on this front may be a new emphasis on program evaluation. Not content merely to pursue philanthropic activities, some companies have undertaken to assess the value of their programs through such methods as input-output-outcome-impact analysis, used to evaluate administrative performance and official development assistance (Table 1), and social return on investment, which translates social benefit into monetary terms.

Table 1. Progress on the Takeda-Plan Healthcare Access Program (July 2009–June 2012)

Another development that has attracted attention in Japan is the advent of financing schemes using “social impact bonds.” SIBs are issued to raise funds from private investors to support social projects that NPOs or other groups carry out in place of government agencies, and the government promises to pay returns commensurate with program efficiency and social outcomes. Britain has pioneered the use of SIBs in a program aimed at reducing prisoner recidivism. Now some Japanese companies are looking at the possibility of contributing to society via the SIB mechanism, not in expectation of financial gain but as a way to enhance the impact of their corporate philanthropy.

CSR Reporting

Three major milestones in the development of CSR reporting came with the successive release of the Global Reporting Initiative Sustainability Reporting Guidelines (2000), the ISO 26000 international CSR standard (2010), and the International Integrated Reporting Framework (2013).

Among Japanese companies, the appearance of the GRI Guidelines in 2000 provided the impetus for a gradual shift from the publication of separate reports in areas like the environment and philanthropy to comprehensive CSR disclosure and reporting. In terms of content, the sheer number and variety of indicators in the guidelines galvanized Japanese companies, stimulating fresh approaches to CSR and sustainability reporting.

While ISO 26000, issued by the International Organization for Standardization, established guidelines for the implementation of CSR activities, it has also had a major impact on CSR reporting. The standard’s seven “core subjects” of social responsibility—organization, human rights, labor practices, the environment, fair operating practices, consumer issues, and community involvement and development—have already begun to appear as the headings of full-page sections in Japanese CSR reports. This has created the physical framework for material disclosure, particularly noticeable in the field of human rights, an area on which many Japanese companies have been reluctant to report. In this way ISO 26000 has encouraged more detailed disclosure regarding the human-rights impact of corporate activity on various stakeholder groups, including employees, consumers, and local community members.

The International Integrated Reporting Framework, drawn up by the International Integrated Reporting Council, was conceived from the start as a means of promoting the integration of CSR into strategic management in the context of reporting. It encourages companies and investors to disclose the impact of CSR-oriented management on the creation of corporate value over the medium and long term.

The foregoing summarizes the process by which Japanese companies have integrated CSR into business management in four key areas of CSR activity. However, such an overview would be incomplete without some mention of the impact that the Tohoku earthquake and tsunami of March 2011 had on CSR integration in all four areas. Examples in the first category of activity—provision of goods and services—are efforts aimed at the rapid resumption of operations in the disaster’s immediate aftermath and initiatives to stimulate economic activity during reconstruction. In the category of business-process integrity, companies created shared value during reconstruction by providing decent employment. In the area of corporate philanthropy, they developed systems for the delivery of emergency support in the form of goods and services, adopted systems to budget funds for long-term disaster relief during recovery and reconstruction, and instituted programs to support employee volunteer activities. In the area of disclosure and reporting, one major result was a trend toward the public release of business continuity plans.

As the foregoing suggests, the relationship between CSR and corporate management is undergoing important changes; rather than CSR advocates trying to influence management, management is taking the initiatives to embrace CSR. Today, all eyes are on the post-2015 UN development agenda currently under preparation. By simultaneously outlining social priorities and highlighting latent market needs, the post-2015 agenda is poised to become another powerful driver for the integration of CSR and business management.