- Article

- Macroeconomics, Economic Policy

Monetary Policy in the Abe Era: A Summative Assessment

September 29, 2020

Senior Fellow Hideo Hayakawa, a former BOJ executive director, evaluates the central bank’s changing policies during Prime Minister Shinzo Abe’s record-setting tenure, from the experimental shock therapy of QQE to the recent COVID-19 response.

* * *

Prime Minister Shinzo Abe’s surprise resignation has sparked renewed debate over the efficacy of the ultra-loose monetary policies pursued in support of Abenomics. In the following, I offer my own updated assessment, highlighting the little-publicized trend toward monetary normalization over the past four years and the lingering impact of reflationism on the Bank of Japan.

The Failed Experiment of QQE

In April 2013, the Bank of Japan launched its aggressive program of “quantitative and qualitative monetary easing” (QQE), a bold effort to boost Japan’s chronically low inflation rate to 2% within two years by doubling the monetary base.

QQE was an experimental policy whose inflationary mechanism was never very well understood. The somewhat simplistic understanding of the media and the financial markets was that by expanding the monetary base through aggressive purchases of Japanese government bonds (JGBs), the BOJ would increase the amount of money in circulation, causing prices to rise, in line with the quantity theory of money.

The problem is that this theory only applies when interest rates are above the zero bound, and BOJ Governor Haruhiko Kuroda and his staff surely understood this basic economic logic. Given Japan’s ultra-low interest rates, how did the BOJ expect to achieve 2% inflation within two years’ time?

In my 2016 book Kin’yu seisaku no gokai (“Misunderstandings” of Monetary Policy), I offered a comprehensive analysis of the merits and limits of this unconventional monetary policy (which, as I explain below, has since metamorphosed into something very different). At that time, I posited that “the Bank of Japan, working from a multiple-equilibrium model, was betting on the possibility that a major shock in the form of a sudden expansion of the monetary base would jolt the Japanese economy out of its deflationary equilibrium and into a healthier equilibrium.” Another possibility is that Kuroda believed he could raise inflation expectations simply by convincing the markets of the BOJ’s commitment to a 2% target, under the neo-Keynesian principle that, under a rational expectations equilibrium, inflation expectations must coincide with the central bank’s inflation target.

Whichever the case, the core mechanism by which the BOJ hoped to achieve 2% inflation was undoubtedly depreciation of the yen. Given how overvalued the yen was prior to the launch of Abenomics (at ¥80 to the dollar), it was not unreasonable to imagine that a monetary base shock would bring it down to earth. A weaker yen would raise prices on imports, and, more important, would strengthen Japanese industry by stimulating sales of exports. If rising corporate profits led in turn to wage hikes, then the transient import inflation ushered in by yen depreciation should give way to sustained price increases.

Unfortunately, the experiment did not bear fruit. To be sure, the value of the yen fell, and stock market prices rose. But the yen’s depreciation did not trigger a substantial boom in exports, and—more critically—the growth in corporate profits did not result in wage increases. In the spring of 2014, the consumer price index registered a 1.5% increase, thanks to import inflation, and that turned out to be the peak. The expected inflation rate, as measured by the yield on CPI-indexed bonds, rose briefly but soon fell to around zero, where it remains.

Undeterred, the BOJ stepped up its quantitative easing in October 2014. Once again, the currency and stock markets welcomed the “Kuroda bazooka II,” but the impact on the real economy was disappointing. Meanwhile, concerns were mounting that if the BOJ’s purchase of long-term JGBs continued at a rate of ¥80 trillion a year, the central bank’s swollen share of outstanding bonds would lead to distortions and dysfunction in the financial markets, as through a scarcity of collateral.

Normalization by Stealth

By 2015, it must have been fairly obvious to the BOJ that it had wrung all it could from QQE. In January 2016, as concerns about the Chinese economy triggered a spike in the yen and a decline in share prices, the BOJ made the decision to adopt a negative interest rate policy. Counterintuitive though it may seem, it is in fact possible to apply an interest rate slightly below zero to a central bank’s current account deposits.[1] The BOJ doubtless thought that doing so would bring down the value of the yen, but with the markets rushing to unload risky investments, the BOJ made the mistake of announcing its negative rate policy at the last moment after repeatedly denying such plans. As a result, the yen surged even higher, and stock prices plunged further. The negative rate policy was consequently branded a failure.

Confronted with the limitations of quantitative easing and the recent failure of negative interest rates, the BOJ privately concluded that its short-term 2% inflation target was out of reach in the short run. At this point, it decided to play the long game and wait for conditions to improve. Of course, it could hardly come straight out and admit that its 2% target was a lost cause. Instead the BOJ announced that it was conducting a comprehensive assessment of its monetary policy and would draw up a new policy framework on the basis of the conclusions.

The most significant conclusion of the assessment, released in September 2016, was the recognition that inflation expectations in Japan had become backward-looking instead of forward-looking. What this meant was that, regardless of the BOJ’s target and the strength of its commitment, it was going to take time for price growth to take hold. This was tantamount to an admission of the need to abandon short-term targets and settle in to play the long game.

The new policy framework adopted around this time embraced the idea of “yield curve control” (YCC), which focuses on controlling long-term interest rates (as opposed to QQE, which targeted the size of the monetary base). It also incorporated an inflation overshooting commitment, under which the BOJ pledged to continue expanding the monetary base until inflation was stabilized at a rate in excess of 2%.[2] Pointing to this commitment, the BOJ portrayed the new policy as a further escalation of its quantitative easing program (ostensibly incorporating a “third dimension,” beyond quantitative and qualitative easing). But that was misleading. After all, there should be no need to expand the scale of bond purchases if long-term interest rates remained under control. Furthermore, the goal set forth in the guidelines published at that time was to maintain yields on 10-year JGBs at “about zero,” and since the yields were already in negative territory, the new policy framework clearly did not call for additional quantitative easing.

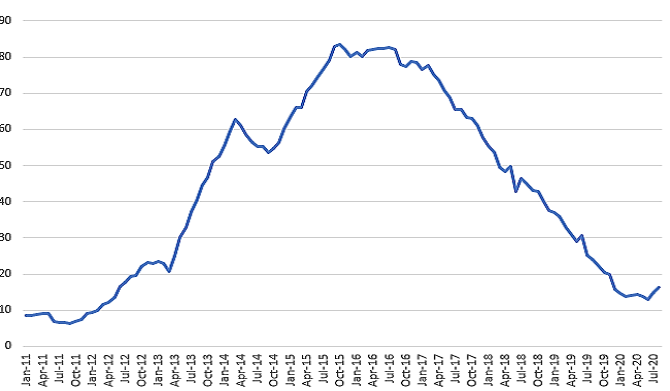

In fact, the main thrust of the YCC program was to shift to a “war of attrition” with 2% inflation as a medium-term goal[3] while gradually normalizing monetary policy by scaling back BOJ bond purchases in order to prevent dysfunction in Japan’s financial markets. We can see this shift clearly in the annual increase in the BOJ’s holdings of long-term JGBs, which ultimately dropped to well below ¥20 trillion from a peak of over ¥80 trillion. However, instead of publicly acknowledging this shift toward monetary normalization, the BOJ carried it out by stealth.

Annual Increase in BOJ Holdings of Government Bonds

(¥ trillion)

Lingering Distortions

As we have seen, the BOJ’s monetary policy underwent a course change four years ago, when it stealthily shifted from a “shock and awe” strategy to a “war of attrition.” Abe acknowledged as much during Diet questioning in June 2019, when he explained that “while achieving 2-percent inflation was one target, our real goal was full employment, and from that standpoint, our policies, monetary policy included, have achieved their objectives.”

However, the after-effects of Abenomics cannot be dismissed. Even leaving aside the negative impact of prolonged ultra-low interest rates on the earnings of Japan’s private financial institutions (particularly regional banks) and the looming issue of how to exit from quantitative easing, the BOJ’s aggressive mobilization of unconventional monetary policy in the service of Abenomics has distorted the central bank’s functions in troubling ways.

One problem it has created is a focus on yen depreciation and stock appreciation as policy goals. As I explained earlier, the BOJ’s QQE program was originally conceived as a strategy for quickly jump-starting inflation by weakening the yen and boosting share prices. When hopes for achieving the 2% target faded, the Abe government decided to play up the effect of Abenomics on the exchange rate and stock market as evidence of its success. As a result, the markets now look to the BOJ to intervene whenever the yen climbs and stocks fall past a certain point.

In the past, the BOJ would have responded to such pressures by pushing interest rates even deeper into negative territory, but it has been burned by the experience of January 2016. Instead, the central bank has resorted to ever-expanding purchases of exchange-traded-funds. This practice, whose efficacy has yet to be assessed, has continued despite numerous warnings centering on three issues: (1) the challenge of negotiating an exit, given that ETFs (unlike government bonds), have no maturity date; (2) potential distortion of the stock market’s price formation mechanism; and (3) possible adverse effects on corporate governance.[4] As a result, while gradually normalizing its monetary policy with respect to the conventional tools of interest rates and money supply, the BOJ has grown increasingly reliant on the unorthodox tool of ETF purchases, resulting in a deviant approach to monetary easing.

The second problem pertains to the BOJ’s communication with the public and the financial markets. I have already described how the central bank portrayed the YCC program as a further escalation of quantitative easing—even though it was actually a movement toward normalization. That was only the first of several occasions on which the BOJ said one thing and did another. For example, BOJ communications following the fall 2019 monetary policy meetings (including official reports and Kuroda’s press conferences) strongly implied that the central bank intended to step up monetary easing, fueling a mood of nervous expectation among market participants. But the additional purchases never took place.

Part of the problem was doubtless the bank’s reluctance to admit that it was retreating from QQE without achieving the program’s objective of 2% inflation within two years. But another factor appears to have been the influence of the “reflationists” that the prime minister appointed to the Policy Board. In order to satisfy these board members, who are constantly agitating for further monetary expansion (especially quantitative easing), the BOJ has been obliged to put an expansionary spin on its public statements.

Major market participants are aware of these dynamics, and for this reason no serious confusion has resulted so far. But one cannot overstate the importance of maintaining total market confidence in the BOJ’s communications, particularly in the event of a situation necessitating a major policy shift.

COVID-19 Response

Since the spring of this year, the BOJ has taken a number of steps in response to the economic shock of the COVID-19 pandemic. Leaving aside emergency measures to stabilize markets (including coordination to enhance US dollar liquidity and an expansion of the quotas on ETF and real estate investment trust purchases), the main components of the BOJ’s response has been (1) removal of the previous annual limit of “about ¥80 trillion” on JGB purchases and (2) “funds-supplying operations” to facilitate financing for hard-hit businesses in coordination with a government program to promote unsecured, interest-free loans.

The announcement of these measures led quite a few critics to opine that the BOJ had waded so far into the quagmire of ultra-expansionary monetary policy that it would never find its way out. But my own assessment is that it has not veered much from its previous course, which was oriented toward gradual normalization with long-term stability in mind. With yields on long-term JGBs hovering around zero, the actual value of the bonds purchased by the BOJ has scarcely increased at all despite the removal of the ¥80 trillion limit.[5]

As for the program to facilitate corporate financing, the BOJ doubtless considers this a smart move. First, unlike quantitative easing, the financing of loans to pandemic-hit businesses can be expected to yield clear and concrete benefits by averting bankruptcies and protecting jobs. Second, because the recipients are financial institutions, and their loans are guaranteed by the central government, this program—unlike the BOJ’s purchase of long-term JGBs and ETFs—does not expose the central bank to market risks that could ultimately fall on the nation’s taxpayers.[6] Third, the program has the effect of contributing to normalization of the BOJ’s interest rates: Thanks in part to the 0.1% interest attached to funding for loans to pandemic-hit businesses, the “basic balance,” to which a +0.1% rate applies, has risen to more than ¥200 trillion, dwarfing the roughly ¥5 trillion negative-rate balance. The role of the negative interest rate policy is gradually shrinking to insignificance.

Post-Abe Trends

It is too soon to predict the direction of monetary policy during the cabinet of Prime Minister Yoshihide Suga, Abe’s successor, but I would expect little change for now. Given current business conditions, the BOJ will naturally want to maintain its expansionary monetary policy. If the government decides to rev up its loan program for struggling businesses, the BOJ’s “coronavirus operations” will doubtless expand as well. Even so, there is a good possibility that it will maintain its current course toward normalization of monetary policy with an eye to long-term goals. (Even with the fiscal deficit growing, long-term interest rates are unlikely to jump anytime soon.)

At the same time, the distorting effect that Abenomics exerted on monetary policy is likely to linger. For example, Suga is said to share Abe’s enthusiasm for keeping the yen weak and share prices high, which suggests that the BOJ could again come under pressure to counter any tendency toward yen appreciation and declining stock prices. And while Suga may well avoid appointing reflationists to the Policy Board, it will be some time before the impact of that shift is felt.

[1] Theoretically, the only constraint on the use of negative interest rates is the existence of cash. If interest goes too far into negative territory, the depositor can get a more favorable rate—i.e., 0%—by withdrawing the funds in the form of cash. It is thought that the Japanese economy’s relatively heavy reliance on cash limits the extent to which it can marshal negative interest rates as a policy tool. This is one of the arguments for promoting the transition to a cashless society. See Kenneth Rogoff, The Curse of Cash, Princeton University Press, 2016.

[2] For my detailed comments on the assessment, see Hideo Hayakawa, “Nichigin no sokatsuteki kensho o yomitoku” (Deciphering the BOJ’s Comprehensive Assessment), Fujitsu Research Institute, Opinion (online column), October 5, 2016, https://www.fujitsu.com/jp/group/fri/column/opinion/201610/2016-10-2.html.

[3] Subsequently, in its quarterly Outlook for Economic Activity and Prices, the BOJ kept pushing back the target date for achieving 2% inflation and finally dropped any mention of a time frame. Additionally, in 2017, the BOJ repeatedly stressed the idea that ultra-low interest rates would gradually improve the economy’s growth potential and, over the long run, lead to price growth in a “high-pressure economy.”

[4] See Keiichi Omura, “ETF kai-ire no kozai” (Pluses and Minuses of ETF Purchasing), in Nihon Keizei Shinbun Sha, ed., Kuroda Nichigin: Chokanwa no keizei bunseki (Kuroda’s Bank of Japan: Economic Analyses of Ultra-loose Monetary Policy), 2016.

[5] Even after annual purchases had dropped to between ¥10 trillion and ¥15 trillion, the BOJ had retained the previous limit of “about ¥80 trillion,” most likely to avert an adverse market reaction and to appease the “reflationists.” (Paradoxically, some observers have concluded that the BOJ took advantage of the COVID-19 crisis to get rid of the onerous ¥80 trillion limit.)

[6] As I have noted elsewhere, one of the serious issues surrounding the BOJ’s unconventional monetary easing policy is whether the central bank, which is not accountable to voters, should be able to pursue policies that might add to the national burden in the future.

-

-

- SENIOR FELLOW(–FY2024)

- Hideo Hayakawa

- Hideo Hayakawa

- Areas of Expertise

-

- Japanese economy

- monetary and fiscal policy

- economic thought

-

Featured Content

-

Haiku: The Heart of Japan in 17 Syllables

Haiku: The Heart of Japan in 17 Syllables

-

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

Japan’s Population Decline and the Gijinkoku Visa’s Pathway to Settlement without Adequate Screening

-

Rice Grown in Rice Terraces

Rice Grown in Rice Terraces

-

Abalone

Abalone

-

Can Japanese Corporations Change?

Can Japanese Corporations Change?