- Article

- Industry, Business, Technology

The Importance of Climate-Related Information Disclosure

May 8, 2020

The Sustainable Development Goals offer a sweeping vista of the biggest economic, social, and environmental challenges humanity must overcome if it seeks to continue enjoying current levels of prosperity. For businesses, aligning their activities with the SDGs is no longer a concern for the CSR department alone; many are giving their highest priority to the SDGs, tapping into their strengths and mapping out a long-term vision in recognition of the opportunities they offer for enhancing corporate value.

This is clear from the results of the questionnaire survey conducted by the Tokyo Foundation for Policy Research. Although responses naturally varied as to which of the 17 goals were of greatest interest and how they were being approached, a high percentage of respondents expressed interest in Goal 13—“Take urgent action to combat climate change and its impacts”—and were taking concrete action. This may be attributable to the fact that companies had already been disclosing their climate-related information for many years and that key global climate initiatives were launched around the announcement of the SDGs, facilitating efforts to enhance corporate value through greater disclosures.

In the following, I will examine the kind of environmental reporting that is likely to bolster corporate value from my vantage point as a senior manager of CDP—an international NGO promoting the disclosure of environmental informational from early 2000 in response to investor requests—with reference to the SDGs and other recent climate-related developments, such as the announcement of tools like Science Based Targets and RE100, the signing of the Paris Agreement, and the establishment of the Task Force on Climate-related Financial Disclosures (TCFD).

Disclosure of Environmental Information

Established in Britain in 2000, CDP is an international NGO that operates a global information disclosure system to monitor environmental impact for investors, businesses, local and national governments, and public organizations. It was launched in response to investor requests for fuller disclosures of climate-related information from major corporations, to whom questionnaires were sent. The responses were compiled into reports that were provided to investors, governments, and responding companies. When launched, the organization was called the Carbon Disclosure Project, reflecting its initial focus on greenhouse gas emissions. Its activities have since expanded to cover other environmental areas, such as water security and forest-risk commodities, and its official name was changed to CDP.

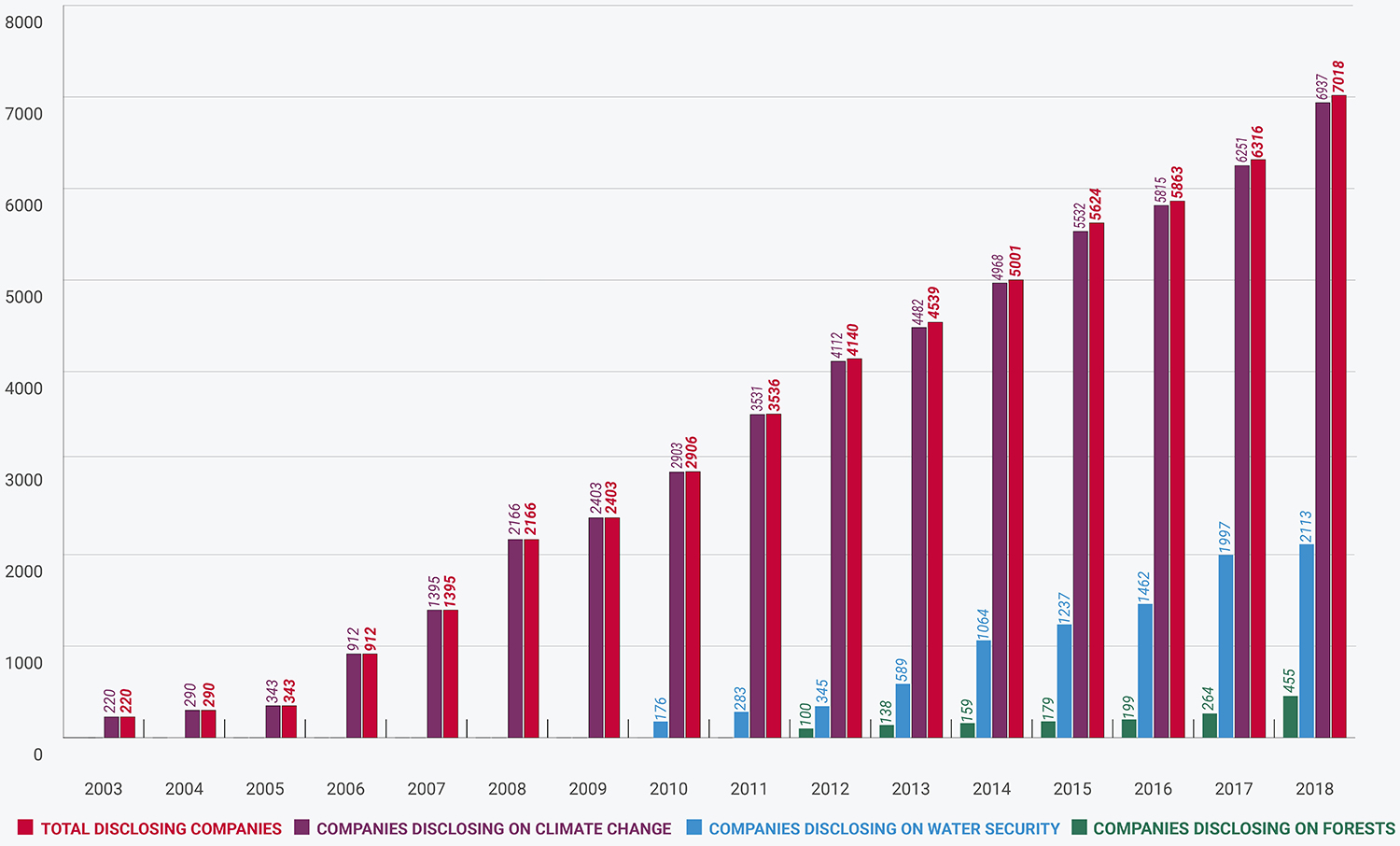

At the start, there were few investors signing the CDP request for climate information, and the number of companies responding with data was very limited as well. Believing that “You can’t manage what you don’t measure,” CDP has been expanding the number of institutional investor signatories and responding businesses over the years. During the 2018 disclosure cycle, some 7,000 companies in 90 countries provided environmental data, as requested by over 650 investor signatories (Figure 1).

Figure 1. Growth in Disclosing Companies since 2003

Source: CDP

The CDP’s growth over the past two decades has been in step with the growing global recognition of the importance of environmental data disclosure. In addition to its investor initiatives, in 2003 the CDP launched a supply chain scheme in which information is requested from the suppliers of major purchasing companies. In 2010, it broadened the scope of its questionnaires to cover not only carbon emissions but also water security, which has a major impact on the environment. In 2011, a CDP cities program was launched, requesting responses not just from companies but also from local and state governments. In 2012, a third questionnaire was added focusing on four commodities (timber, palm oil, soy, and cattle products) that have a major impact on deforestation. By collecting and summarizing the responses of companies and local governments regarding their environmental efforts and by assigning scores, CDP is promoting global improvements in corporate and local government engagement. Figure 2 shows the key items covered in the CDP’s three questionnaires.

Figure 2. Main Disclosure Topics in the Three Questionnaires

Source: CDP

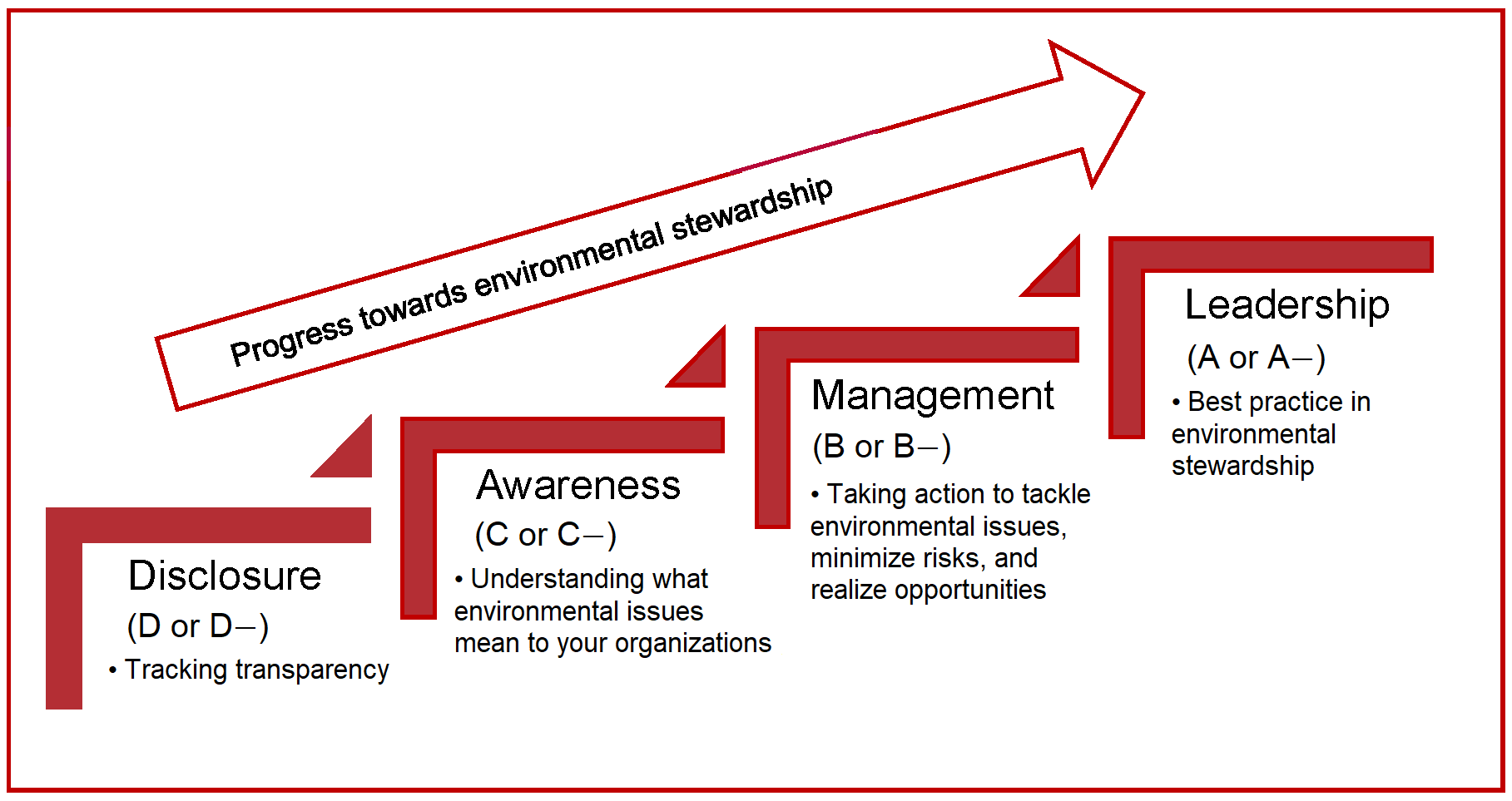

As shown in Figure 3, CDP aims to incentivize companies by scoring their progress toward environmental stewardship; a D score means that a company recognizes the need for disclosure, C companies are those that are aware of risks and opportunities, B means they are able to manage environmental risks and impacts, and A indicates that the company is at the stage of leadership and can resolve environmental issues independently.

Figure 3. Illustration of Scoring Levels

Source: CDP

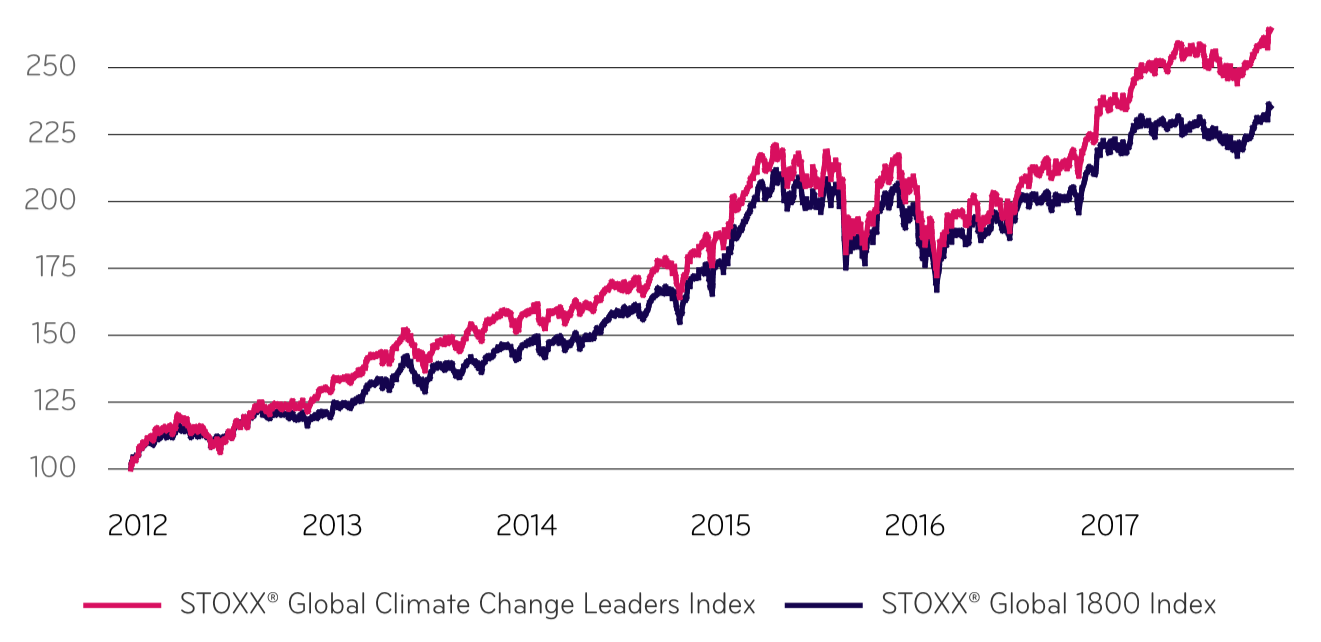

Figure 4, meanwhile, shows that of the 1,800 companies contained in the Global 1800 STOXX Index, those that have earned an A score from the CDP and are thus included in the Global Climate Change Leaders Index have seen their share prices outperform the benchmark index by 12% over a five-year period. The market clearly regards sustainable business practices as a positive feature.

Figure 4. A-List Companies Outperform Global STOXX Index

Source: STOXX website, https://www.stoxx.com/document/Indices/Factsheets/2017/October/SXCCLEG.pdf.

Two Disclosure Schemes

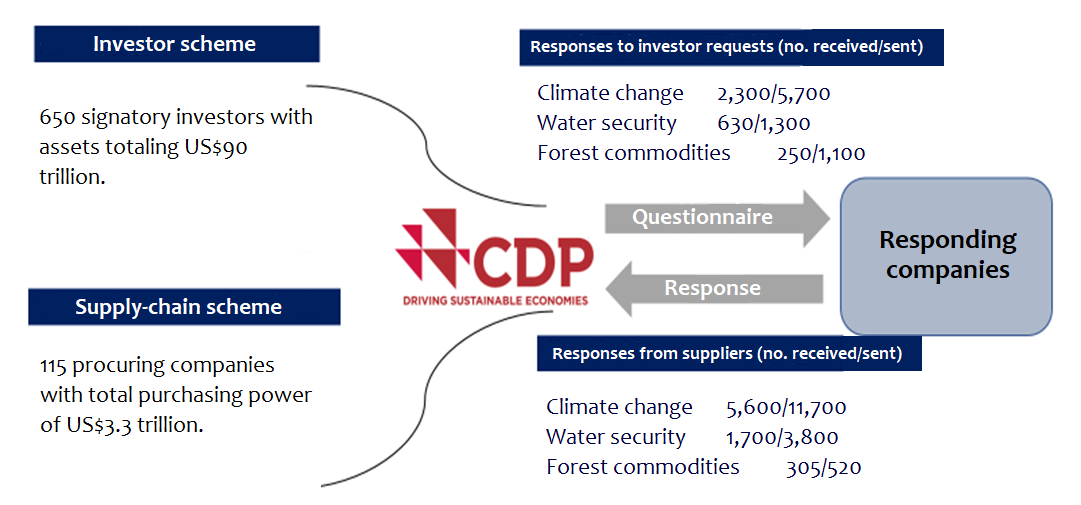

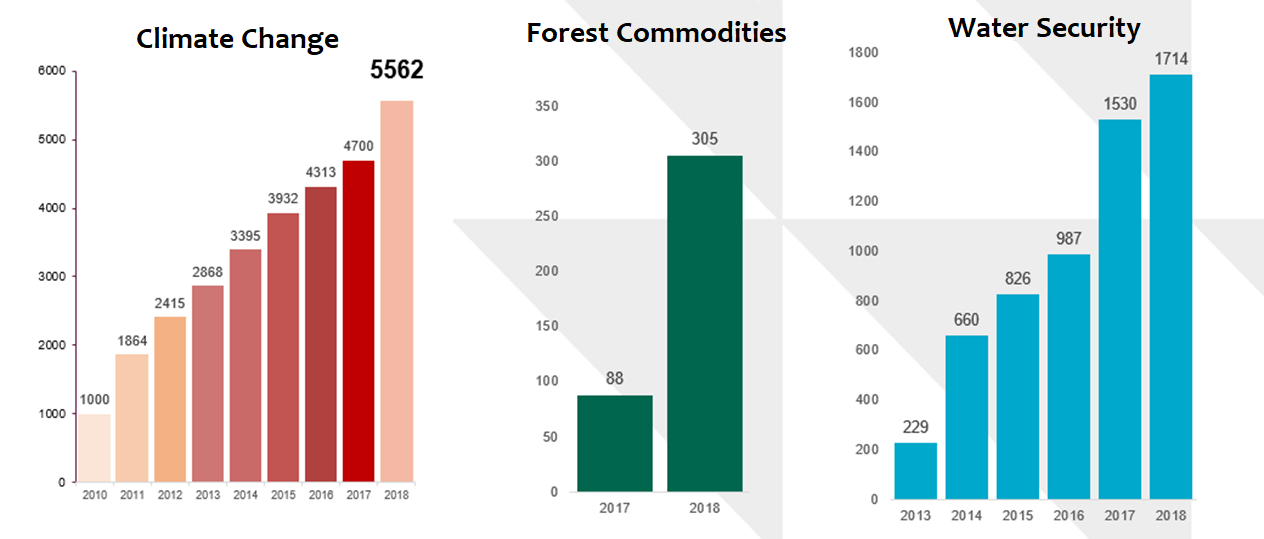

As mentioned above, the CDP has two disclosure schemes—one to facilitate investment decisions and, since 2008, another to aid procurement and supply chain decisions. Figure 5 shows the response status of the two schemes in the domains of climate change, water security, and forest commodities during the 2018 disclosure cycle.

Figure 5. The CDP’s Two Schemes during the 2018 Disclosure Cycle

Source: CDP

The top half of the figure shows the responses to information disclosure requests from investors and the bottom half gives the status of responses to questions from procuring entities. Requests for climate-related information from investors were met by 2,300 companies, while more than double that number—5,600—responded to questionnaires about the supply chain. The number of responding companies in the supply chain scheme was also much higher in the case of water security and forest commodities.

The total purchasing power of the 115 procuring companies in the 2018 disclosure cycle exceeded US$3.3 trillion, but the total assets of the 650 investors was much higher at approximately US$90 trillion. It appears, though, that respondents were more motivated to complete the questionnaire for the former than the latter. Inasmuch as the CDP seeks to create a better world through disclosure, the prominence of the supply chain scheme will no doubt grow in the years ahead.

Encouraging Fuller Disclosure throughout the Supply Chain

Many suppliers receive disclosure requests from multiple purchasing organizations—sometimes from over 30. As we have seen, the higher the number of requests, the greater the inclination to accommodate those requests. In such cases, using the CDP disclosure format can substantially reduce the reporting burden, since a single report can meet a full range of requests.

The purchasing organizations in the CDP supply chain program belong to a variety of industries, from retail, autos, and finance, to machinery, electric power, electric appliances, chemicals, and consulting. Participating Japanese companies include Kao, Nissan, Toyota, Honda, Ajinomoto, Fujitsu, Mitsubishi Motors, Bridgestone, Sekisui Chemical, and NEC. In addition to private companies, such government bodies as the US General Services Administration and Japan’s Ministry of the Environment participate as purchasing members, underlining the importance of supply chain management.

Under the supply chain program, purchasing members can currently register up to 500 suppliers from whom information is requested. While there is considerable overlap among those suppliers, the number of respondents should continue to rise with the expansion of procurers, so long as the response rate does not decrease drastically. (Rates are unlikely to fall, since suppliers will be under greater pressure to submit a response in the face of duplicate disclosure requests from a larger membership.) Figure 6 shows the increases in the number of responding companies in the CDP supply chain program. When the climate change supply chain program started in 2008, there were 19 purchasing members, which increased to 115 in 2018 and to over 125 in 2019. The water security program began in 2013 and currently has more than 40 purchasing members, while that for forest commodities was launched in 2017 and has 14 members today.

Figure 6. Supplier Engagement to Date

Source: CDP

There is growing awareness among companies interested in contributing to a sustainable society that they must shoulder part of the responsibility for addressing social issues in the supply chain. The supply chain emissions of greenhouse gasses, for example, are usually much bigger than a company’s own emissions—an average of around 5.5 times larger for all industries, according to the CDP’s Global Supply Chain Report 2019. Achieving dramatic reductions in GHG emissions will obviously require cuts throughout the supply chain.

Key Climate Change Initiatives

Sustainable Development Goals

Announced in September 2015, the SDGs are a call to collectively address pressing social, environmental, and economic challenges facing humanity and the planet. Efforts to address those challenges also represent huge business opportunities; the World Business Council for Sustainable Development estimates that the SDGs will create 380 million new jobs and boost the global economy by US$12 trillion annually.

The SDGs can help companies establish a long-term vision for social engagement, enabling them to enhance their corporate and brand value through their main business activities and contribute to creating shared value (CSV). To survive in an environment with fewer growth sectors, businesses need to shift their thinking from CSR to CSV, mapping out long-term strategies that focus on the sustainable goals that simultaneously promise to be economically viable.

Although specific climate change targets are spelled out in Goal 13 of the SDGs, climate action will have a major bearing on other goals as well, such as efforts to eliminate hunger and promote clean water.

Paris Agreement

The Paris Agreement was adopted in December 2015—the same year as the SDGs—with the goal of holding the increase in the global average temperature to below 2°C above pre-industrial levels (and pursuing efforts to limit the increase to 1.5°C). Unlike the 1997 Kyoto Protocol, which assigned targets only to developed countries, the Paris accord sought binding commitments from all parties, including China, India, and other emerging and developing countries. Although achieving the 2°C goal will be difficult—to say nothing of the 1.5°C target—with the nationally determined contributions announced thus far, the agreement was nonetheless significant for bringing all countries of the world together to address one of the biggest challenges facing humankind and the planet. (In this regard, the decision by US President Donald Trump to withdraw was extremely disappointing).

Science Based Targets

The Science Based Targets initiative (SBTi) is a framework under which businesses set ambitious, medium-term (5 to 15 years) emission reduction targets using sectoral models to hold the rise in global temperature below 2°C from pre-industrial levels, as outlined in the science-based proposal of the Intergovernmental Panel on Climate Change (IPCC). Each company sets its own targets and submits them to the SBTi for validation. The initiative is a collaborative undertaking among the CDP, the World Wide Fund for Nature, the World Resources Institute, and the United Nations Global Compact. Following the release of the IPCC’s Special Report on Global Warming that warned of severe consequences of a failure to prevent global warming exceeding 1.5°C, the SBTi has announced major updates to help companies align their targets with the most ambitious trajectory and achieve net-zero emissions by the middle of this century.

As of May 2019, 554 companies worldwide have submitted their reduction targets to the SBTi, and more than 210 have been approved. In Japan, 76 companies have made commitments with support from the Ministry of the Environment, with 42 approved. In addition to establishing dramatic reduction targets for Scope 1 and 2 emissions occurring directly and indirectly (via purchased electricity, etc.), respectively, from business operations, companies are urged to embrace ambitious targets for Scope 3 (value chain, both upstream and downstream) emissions if they exceed 40% of the total. More companies are adopting dramatic reductions throughout the supply chain by sharing their longer-term targets with their suppliers (Figure 7).

Figure 7. Science Based Targets

Source: CDP

RE100

RE100 is an initiative led by the Climate Group in partnership with CDP that brings together major companies committed to sourcing 100% renewable electricity globally by 2050, at the latest. As of March 2019, 166 companies have made a commitment to go “100% renewable,” including 17 from Japan (such as Sony and Ricoh). Participating companies—limited to those that are considered “influential”—come from a broad spectrum of industries, including manufacturing and finance. Apple and Microsoft are already close to sourcing 100% of their global electricity consumption from renewables.

Task Force on Climate-related Financial Disclosures

The Task Force on Climate-related Financial Disclosures (TCFD) is a private-sector initiative established in 2015 by the Financial Stability Board (FSB), then chaired by Bank of England Governor Mark Carney, in response to a G20 request for greater financial market stability. When its Recommendations report was release in June 2017, about 100 companies and financial institutions adopted the information disclosure structure aimed at better informing financial markets and investors. That number had surpassed 600 as of March 2019 as support for voluntary risk disclosures has spread rapidly.

The aim of the TCFD is to achieve integrated corporate disclosure of climate-related information and mainstream financial data, since investors, in making financial decisions, need to understand how climate-related risks and opportunities could affect future cash flows, assets, and liabilities.

The TCFD framework consists of the four core elements of (1) governance, (2) strategy, (3) risk management, and (4) metrics and goals (Figure 8). This is basically in line with the CDP climate change questionnaire, but there are some new elements, so the CDP made a few additions and revisions in 2018 so that disclosure through the CDP questionnaires will be aligned with the recommendations of the TCFD.

Figure 8. The TCFD Framework

Source: TCFD

Specifically, the CDP questionnaire added such items as the monitoring of climate-related issues and the processes by which companies identify, assess, and manage those issues (governance), as well as the financial impact of a business’s strategy, risk management, and metrics and targets. In addition, the CDP’s questionnaire has transitioned to a more sector-specific approach, initially incorporating questions for 15 of the 22 sectors outlined by the TCFD in the 2018 questionnaire and eventually moving to all 22 sectors between 2020 and 2022. Additional items relating to carbon pricing have been added, and scenario analysis has been incorporated as an aspect of strategic planning.

The TCFD divides climate-related risks into those accompanying the (1) transition to a lower-carbon economy (policy and legal, technology, market, and reputation) and (2) both acute and chronic physical risks (increased severity of typhoons and floods; changes in precipitation patterns, rising mean temperatures, and rising sea levels). It also identifies five categories of climate-related opportunities for management reform through climate change mitigation and adaptation measures (in the areas of resource efficiency and cost savings, the adoption of low-emission energy sources, the development of new products and services, access to new markets, and building resilience along the supply chain). Companies are also called upon to analyze and disclose the impact of physical damage and planned responses on their cash flow, income statement, and balance sheet in terms of both risks and opportunities.

Enhancing Corporate Value through Disclosure

When a company begins using CSV approaches in responding to societal issues and climate-related risks and opportunities, such responses will need to be assessed with the same tools as those used to gauge its other business activities, including for their financial impact, to properly measure corporate value. The TCFD recommendations clearly express such expectations with respect to climate-related responses from the investors’ point of view. In this following, I will describe the key points of the disclosure requirements of the TCFD and other climate-related initiatives and recommendations, elucidating how such disclosures can help enhance corporate value.

Governance: Top management is shown taking the lead in integrating climate-related responses into the company’s management strategy. Also important is to clearly delineate the functions and respective roles of the management team.

Strategy, risk management, and metrics and targets: While these elements have previously been included in CDP questionnaires, companies should aim for greater clarity in indicating how they impact on cash flow, income statement, and balance sheet, including in estimates.

Integration of financial and nonfinancial information: The main goal of the TCFD is to facilitate management and investment decisions by integrating financial information with climate-related disclosures of strategy, risk management, and metrics and targets. Annual and other mainstream reports should therefore contain impact assessments in line with the TCFD recommendations and the guidance announced by the Climate Disclosure Standards Board (CDSB) and Sustainability Accounting Standards Board (SASB).

Scenario analysis: Scenario analysis enables an organization to strategically plan for future developments that are shrouded in uncertainty. Mapping out potential future outcomes also entails the disclosure of their preconditions. Existing scenarios for transition and physical risks, such as those published by the International Energy Agency, as well as the Asian-Pacific Integrated Model (AIM) of the Shared Socioeconomic Pathways (SSP) may be used to assess global, long-term risks and opportunities.

Science Based Targets: Ambitious, longer-term targets are required to achieve net zero emissions, as called for by the Science Based Targets initiative, by the middle of this century.

Carbon pricing: A carbon pricing system is indispensable when quantifying climate-related responses in economic terms. Disclosures should be made of internal carbon pricing mechanisms and participation in carbon markets.

Procurement and supply of renewable energy: A dramatic reduction in carbon emissions requires a decision to eliminate the use of fossil fuels and the adoption of a long-term, innovative plan for a transition to renewable energy, as advocated under the RE100 initiative. A good model to follow may be companies like the BT (formerly British Telecom) Group and Microsoft, which share their renewable energy targets with businesses in their supply chain.

Sector-specific responses: Because impacts and solutions vary depending on sector (industry), sector-specific disclosures will also be required. The TCFD provides supplemental guidance for four nonfinancial groups (energy; transportation; materials and buildings; and agriculture, food, and forest products) and the financial sector (banks, insurance companies, asset owners, and asset managers), and the list of sector-specific disclosure items will likely grow going forward.

Supplier engagement: There is greater room for reductions in supply chain emissions than in Scope 1 and 2 emissions—an average of 5.5 times more across all industries. A vision spanning the entire supply chain is thus required, with suppliers being informed of medium- to long-term targets and encouraged to set their own science-based targets, thereby creating a cascading effect of lowered emissions.

Judging by recent climate initiatives and the recommendations of the TCFD, companies can expect to raise their corporate value by focusing their disclosure efforts on the above nine items. They should first shore up their governance structure and then clarify their climate-related strategies, the risks and opportunities they face, and their metrics and targets—from both a long-term and economic (integration with financial data) perspective. A long-term perspective entails utilizing the disclosure mechanism to clearly outline a sustainable, future vision and a brand-building direction. Enhanced corporate value will result from the implementation of such activities throughout the supply chain.

Governance had been a prominent element of the CDP questionnaire even before the TCFD issued its recommendations. The questionnaire also incorporates long-term goals like science-based targets and the use of renewable energy. There are new elements, though, that emerged following the TCFD recommendations—notably integration with financial disclosures—and these were added to the CDP questionnaire in 2018. So today, responding to the CDP questionnaire covers all the climate-related issues raised by the TCFD, SBTi, RE100, and SDGs.

As shown above, progress made to date in climate-related areas far surpass those of other issues covered by the SDGs, both in terms of the disclosure demands of investors and the measures implemented by companies. This is obviously an area, therefore, that can contribute to improving corporate value.

In addition to further promoting climate-related disclosures, CDP is also working to build broader momentum in its two other domains of water security and forest commodities. The call for the disclosure of environmental information by CDP in 2003 has become increasingly significant in the wake of subsequent global initiatives and recommendations. Companies whose influence has greatly grown due to globalization and other changes need to play a leading role in promoting understanding of and participation in disclosures that can not only enhance corporate value but also create a more sustainable world.

Disclosure is a powerful springboard for change. It can motivate companies to draft long-term strategies for ambitious emission reductions and adopt other measures for a sustainable and prosperous future for individuals, society, and the planet as a whole. In fact, it might be our only hope in a modern, highly developed society, in which economic activity plays such a central role. Disclosure is the path that all recent climate-related initiatives and recommendations, as well as the SDGs, urge us to follow.

Ken’ichiro (Ken) Yamaguchi is a senior manager (supply chain) at CDP Worldwide Japan and partner of Megawatt-X, an online, renewable assets transaction platform. He joined the Bank of Tokyo after graduating from Keio University’s Faculty of Economics in 1982 and moved to JP Morgan in 1991, participating as vice-president in launching the financial products business in Japan. He joined Tokyo Mitsubishi International PLC (UK) in 1998 as executive director, established Petro Diamond Risk Management in 2003 (UK), serving as president and COO, and joined Deutsche Bank in 2010 as director of commodity sales. He received a master’s degree in environment and sustainability from Birkbeck, University of London, in 2016.