Gojo & Company operates a group of microfinance institutions in the developing world with the goal of providing financial access for all. Founder Taejun Shin offers an overview of the challenges faced by microfinance in its quest for fuller financial inclusion.

* * *

Gojo & Company was founded in pursuit of an overarching vision: a world in which everyone has an opportunity to overcome their fate and attain a better life. To this end, the company’s first mission is to be a “private-sector World Bank” providing financial access for everyone in developing countries.

The company’s name harks back to the early credit unions known as gojo-ko , established by the agricultural pioneer, economist, and philosopher Ninomiya Sontoku (1787–1856). The Gojo of our company name is not a person but a term referring to the five Confucian virtues of benevolence, righteousness, propriety, wisdom, and integrity. While many professional firms have their founders’ names, I chose to use Gojo in place of a personal name because I wanted to identify the company with the ideals to which it is committed, not with a single individual.

Gojo is a holding company that operates a group of subsidiary microfinance institutions in the developing world. As of April 2017, our microfinance institutions (MFIs) in Cambodia, Sri Lanka, and Myanmar have a total of 320 employees providing face-to-face financial services to more than 40,000 customers. By 2030, we hope to expand those services to at least 100 million people in 70 countries as part of our quest for worldwide financial inclusion.

In the following section, I offer a brief explanation of microfinance and the challenges it faces, followed by an inside glimpse into Gojo and a look into the future of our enterprise.

What Is Microfinance?

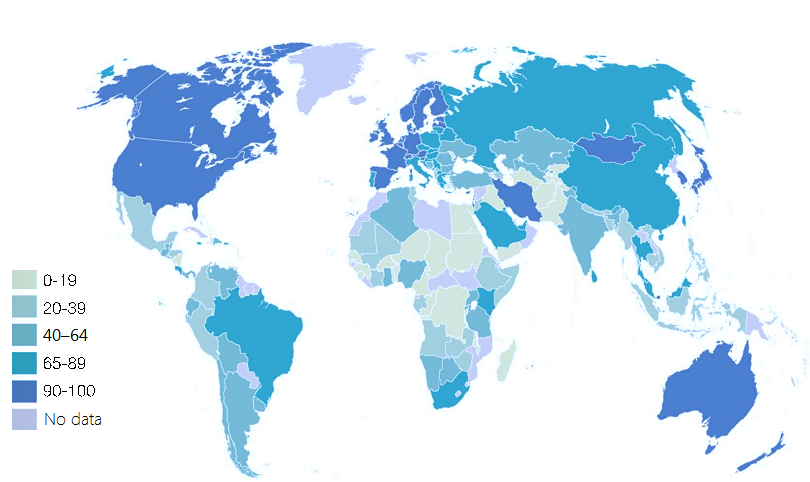

In its Global Financial Development Report 2014 , the World Bank estimated that at least 2.5 billion of the world’s 7.3 billion people (about 50% of adults) had no bank account whatsoever. Of these, the vast majority are low-income individuals living in developing countries.

Figure 1. Adults with an Account at a Formal Financial Institution, 2014 (%)

In countries like Japan, where access to financial services is taken for granted, it is difficult for people to grasp the difficulties this situation poses. Without such financial services, saving money is risky, and enrolling in health insurance programs is difficult or sometimes impossible. Anyone undertaking a project or launching a business would need to raise all the cash he or she would require in advance. For many, the only available choice is to turn to informal financial services, which often charge extremely high fees and interest rates.

Microfinance institutions exist to fill this gap. MFIs provide a range of financial services to low-income individuals in developing countries, including small loans (microcredit), small-deposit accounts (microsavings), and small-scale insurance schemes (microinsurance).

How do MFIs help? Let us take the example of a woman in a developing country who is struggling to make ends meet by hand-sewing and selling apparel. A sewing machine would vastly improve her productivity, but since she barely earns enough to support herself on a day-to-day basis, she cannot hope to save up enough to invest and escape from the cycle of poverty. If, on the other hand, she can obtain a loan of a hundred dollars or so to buy the sewing machine, she can boost her production dramatically, repay the loan with interest, and still have money left over. This is where MFIs come in. The number of institutions providing such services in the developing world (counting only those with at least a few million dollars in assets) is now estimated at more than 1,000.

Making Microcredit Pay

Before the advent of MFIs, low-income individuals in the developing world had nowhere to turn for financial help except village moneylenders, who tended to charge usurious interest rates—often in excess of 200%. To understand why banks refused to lend to the poor, we need to do some rough calculations.

Even in developing countries, bank officers need to have attained a certain level of education to do their jobs, and as a result, their starting pay is generally no less than around $200 a month. In order to cover various overhead costs and earn a profit, banks expect their local loan officers to bring in four or five times their monthly salaries, or roughly $1,000 a month. If we assume a monthly interest rate of 2%, a loan officer needs to secure $50,000 in loans in order to bring in $1,000.

If the average loan were, say, only $200, each officer would need to have 250 clients. To rigorously screen this many clients and then call on them on a weekly or monthly basis to collect payment would be impossible. Yet without such rigorous screening and follow-up, a considerable percentage of these clients could be expected to default on their loans. This explains why banks have not lent to the poor. And the refusal of reputable lenders to provide microfinancing is what allowed local moneylenders to charge such exorbitant interest rates.

However, the advent of pioneering MFIs like Grameen Bank revolutionized the finance sector in large areas of the developing world by making credit available to the poor at previously unheard of interest rates. At the heart of their success was a model that leveraged the power of the community to boost efficiency and slash default rates.

The basic method involved lending to a homogeneous “solidarity group” consisting of about five borrowers jointly responsible for repayment. Since each member of the group was subject to screening and monitoring by the others, this made it possible for the MFI to weed out unreliable borrowers with a minimum of screening to confirm that the applicants met the minimum qualifications. This method succeeded in slashing the time it took loan officers to evaluate applications, resulting in a dramatic reduction in processing costs. Aided by the MFI's team-building efforts, such groups learned to support one another and pay their loans very reliably.

Another way MFIs have minimized their default rate is to have borrowers gather at a community center or similar meeting place to repay their loans en masse. Apart from streamlining the work of loan officers and improving productivity, this is a great motivator for borrowers, since anyone who fails to show up or pay up at the meetings risks losing the confidence of his or her fellow villagers.

Thanks to a combination of methods like these, MFIs worldwide have managed to maintain a default rate of less than 3% on average.

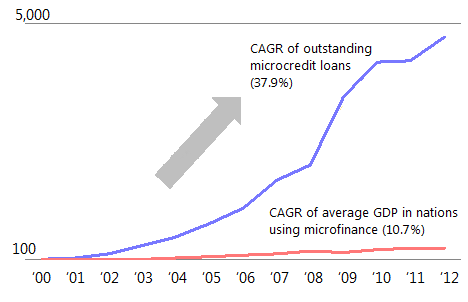

In developing countries where government bond yields hover around 10%, MFIs are able to provide loans to the poor at annual percentage rates of about 30%—a fraction of the previously usurious rates—and have been able to maintain a recurring profit margin of more than 10%. As a result, the outstanding balance of microcredit loans has soared since 2000. As of 2012, growth in microfinance was three times the average growth in gross domestic product among the countries where microfinance has taken hold.

Figure 2. Indexed Growth in Microcredit and Average GDP, 2000–2012

In recent years, the trend has been away from traditional solidarity lending. One reason for this is that collective responsibility, if rigorously applied, can lead to the exclusion of the people most in need of help or those who have trouble communicating with other villagers. That said, most MFIs continue to draw from a common toolkit of methods designed to leverage the power of the community in various ways.

Another common feature of microfinance is that the overwhelming majority of borrowers are women. To some degree, this may reflect a deliberate policy of empowering women, but it also relates to the perception that women have less mobility than men and are much less likely to abscond in the event that they run into repayment problems. Gojo & Company is no exception in this regard. In Cambodia, approximately 90% of our borrowers are female, and in Myanmar and Sri Lanka, practically all of our customers are women.

Traditional Microfinance versus Commercial Financing

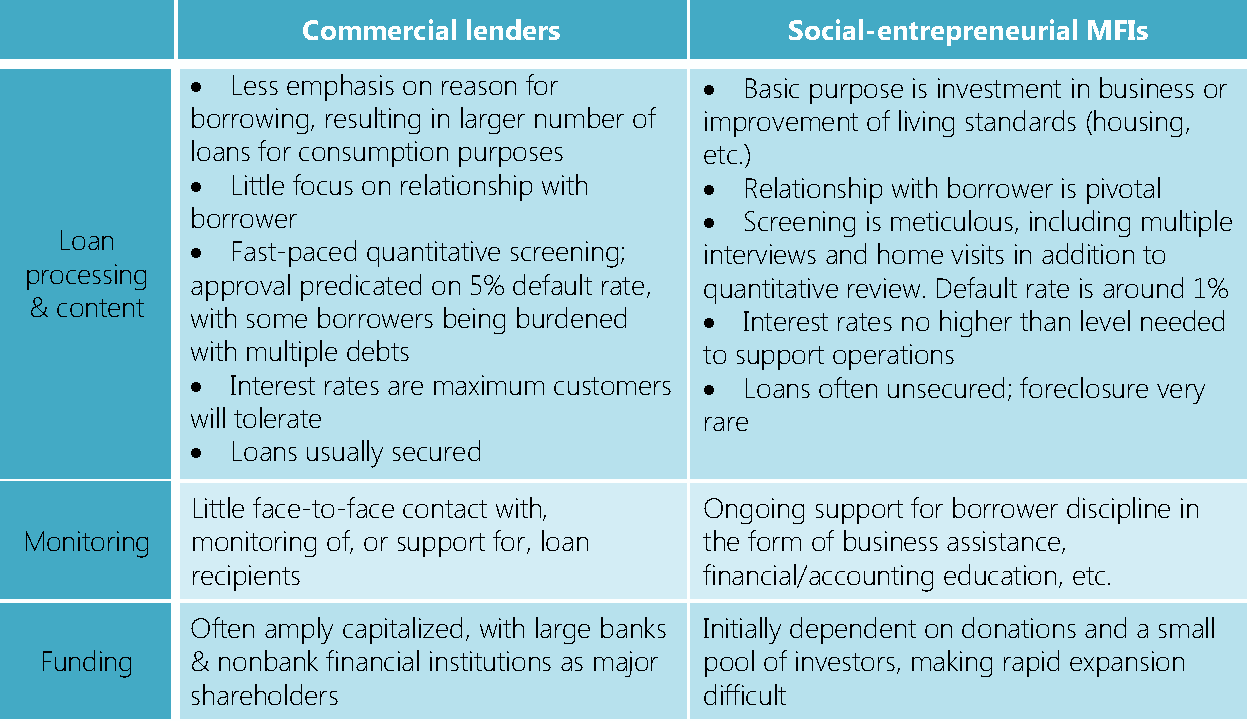

Although the line separating MFIs from consumer lenders has blurred in recent years, it is still possible to distinguish between social-enterprise-style MFIs on the one hand and consumer-financing and commercially oriented MFIs on the other.

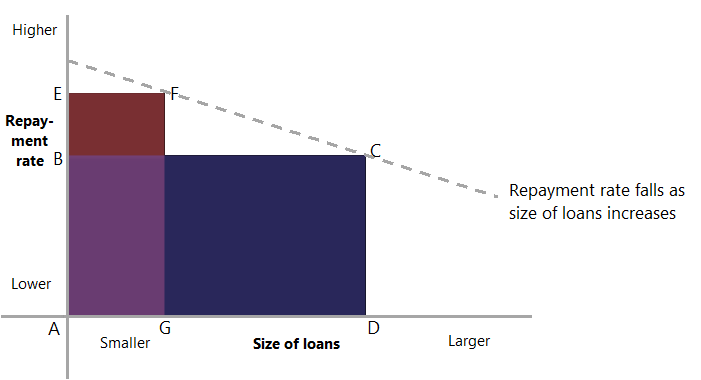

As I understand it, the most basic difference between the two types of institutions is the time frame in which they operate. Commercially oriented finance companies structure their lending policies with the aim of maximizing short-term earnings, given their customers’ income and the probability of default. From this standpoint, a company may actually do better to offer bigger loans than their customers need, even though this increases the risk of default. Many customers, especially those with little understanding of interest and its impact, assume that a bigger loan is a better loan, and profit-oriented lenders will often take advantage of their ignorance, persuading them to take out large loans, whose repayment burden they may later regret. Bigger loans translate into lower repayment rates, but up to a certain size, they will generate higher net earnings for the lender. Figure 3 schematically illustrates the relationship between size of loans and revenue after loan loss, with the area inside the rectangles indicating revenue after loan loss. The rectangle set off by points ABCD represents the optimal situation for commercial lenders from the standpoint of profitability maximization.

Figure 3. Size of Loans, Repayment Rate, and Lender Profits

In Japan, for example, consumer finance firms operate on the premise of a 5% default rate, which is to say that one out of 20 borrowers is expected to default each year. This may be a viable business model, albeit predicated on the financial misfortune of one in 20 customers.

MFIs that operate on a social-enterprise model are oriented to maximizing long-term gains by supporting the sustained growth of their customers’ economic activities. With this in mind, they screen applicants carefully and lend appropriate amounts to minimize the likelihood of default. (The income from such loans is represented by the rectangle AEFG in Figure 3.) Because of their emphasis on the long-term health and growth of their customers’ enterprises, such MFIs also devote considerable time and effort to building strong relationships with customers and providing them with financial education and business support.

Where interest rates are concerned, commercially oriented lenders tend to impose the maximum rate the clients can bear, given their circumstances. And as we have seen, this can sometimes mean annual rates in excess of 100% in countries where the poor have little choice.

Banco Compartamos of Mexico, which, in 2007, became the first MFI to undertake an IPO, has since come under sharp criticism from the microfinance community for going commercial and charging its customers interest rates in excess of 60%. IFC and Accion, reputable investors in the field, were shareholders that questioned the bank’s objectives. Responding to such criticism, the chairman of Compartamos argued that, in order to solve the problem of financial inclusion, the industry must generate profits quickly and attract more funders. I have had discussions with the bank chairman and found that the issue does not lend itself to simple answers.

Finally, with regard to scale, commercial MFIs tend to be more heavily capitalized, often backed by big equity investments from larger commercial institutions, such as regional banks and leasing companies. With a few exceptions, such as Grameen Bank, traditional MFIs are smaller in scale. The main reason for this is probably that the history of modern microfinance in most countries goes back only about two decades. An MFI that enjoys the backing of a financially powerful organization is at an advantage in terms of early growth, and the gap naturally tends to widen as time goes on, sometimes crowding out smaller-scale MFIs.

Commercial banks and leasing companies are usually listed in the local stock market, as opposed to family-owned businesses or partnerships. Such companies are often under intense pressure to manage their investments in a way that maximizes shareholder wealth over the short term. When such a company controls a major interest in an MFI, the organization can easily succumb to commercialization.

The table below summarizes the key differences between social-entrepreneurial MFIs and commercial lenders.

Commercial Microcredit Lenders and Social-Entrepreneurial MFIs

Challenges Facing the Microfinance Sector

I have been visiting various developing countries since 2009, and I have identified three basic problems in the microfinance sector.

The first is a lack of sufficient funds. As noted above, some 2 billion adults around the world lack financial access. Providing quality services for all these people would require an infusion of several hundred billion dollars.

The second problem is a lack of high-level managerial talent. In developing countries in particular, the most talented young people tend to be tracked into elite educational programs and recruited by global corporations. The fact is that even some of the best MFIs are being run by people lacking discipline and strong management skills.

I myself was an investment professional specializing in private equity and provided management consulting services to companies in which the fund had invested. Armed with this background, I cannot but feel that traditional MFIs could augment their organizational capabilities more rapidly if they had the benefit of talented, well-trained local personnel serious about improving microfinance management.

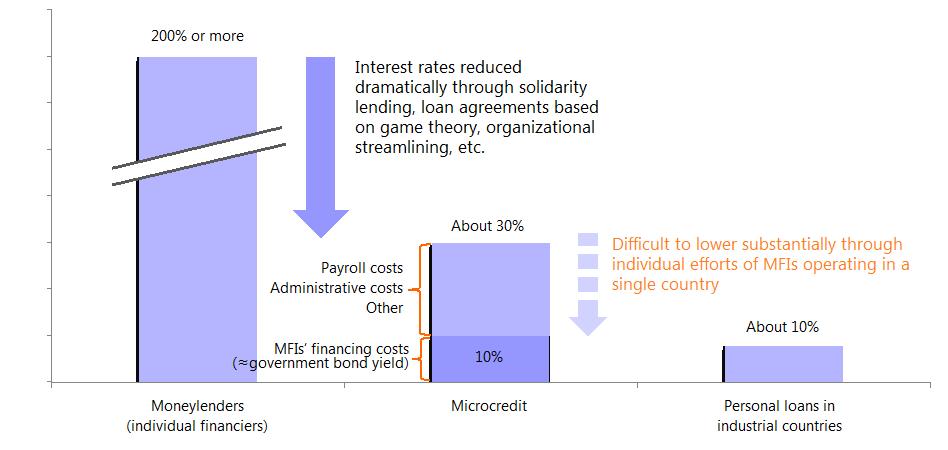

Third, personally speaking, there is no getting around the fact that even socially oriented microfinance services remain quite costly. To be sure, 30% interest is a vast improvement over 200%, which was common before the advent of microfinance, but it is still unaffordable for some people. When people living in remote and impoverished rural areas are struggling to build a business to supplement their meager household incomes, the burden of keeping up with interest payments can push them over the edge.

Figure 4. Rough Comparison of Interest Rates in Developing Countries

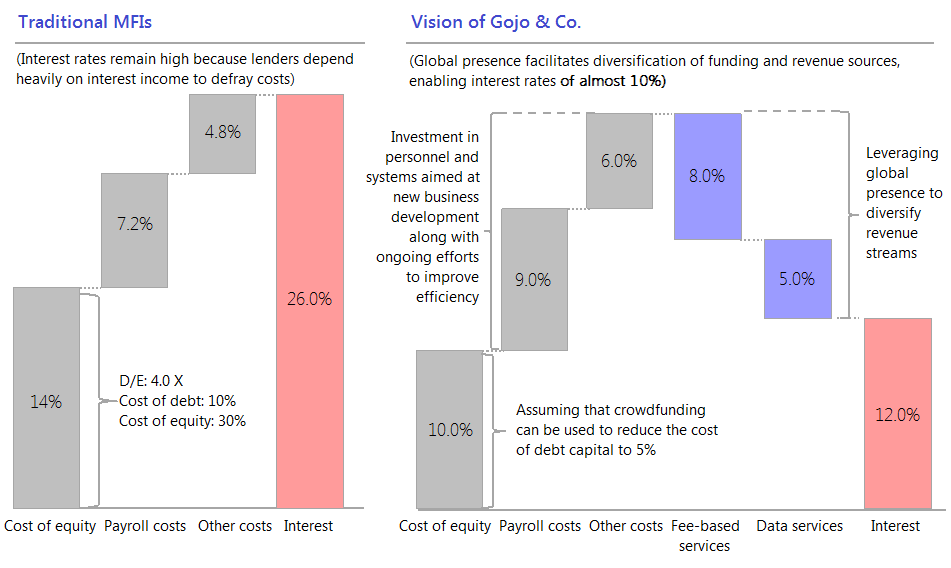

MFIs face many hurdles in lowering interest rates below 30%. The first is the high cost of financing their own operations. In developing countries, where government bond yields often hover around 10%, the weighted average cost of funding a company’s lending operations via equity, debt, and deposits runs to around 15%. The second problem is the relatively high labor and administrative costs of small-scale lending, a burden that no amount of rationalization and streamlining can offset. Finally, many MFIs depend almost exclusively on interest income from the loans they provide in order to defray these costs.

Given these structural constraints, not even the most efficient MFI is capable of lowering its interest rates to less than about 20%. Granted, from a cost viewpoint, a 20% rate in a developing country is roughly equivalent to a 6% rate in Japan or other developed countries. Still, we believe we can and should do better.

Overturning the Status Quo in Microfinance

Gojo & Company has embraced the mission of overturning the status quo in microfinance and ultimately bringing down the overall price of financial services through two basic strategies: (1) having our own well-managed MFIs in each country, and (2) diversifying our revenue streams by creating new services that leverage our global presence. Let us examine these strategies in greater detail.

Establishing our own well-managed MFIs in each country

Since founding Gojo & Company three years ago, we have set up MFI subsidiaries in three countries—Cambodia, Sri Lanka, and Myanmar. We post employees to these local subsidiaries or else arrange for frequent visits to keep management on track and to promote continuous improvement. We use a variety of methods to expand our business operations, including acquisition of local businesses and partnerships with recently established MFIs.

It is very unusual for any financial institution to successfully expand its retail business overseas over such a short term. This applies to not only microfinance but major Western and Japanese banks as well. A major Bangladeshi MFI has attempted to expand its operations in a number of other developing countries, but so far all of its efforts have ended in failure.

The basic problem is that the business of retail banking and lending is fundamentally local in character and as such requires an approach carefully tailored to the local context. Designing and implementing such a customized approach is not something at which the typical financial institution excels—as I will explain in detail later.

Furthermore, the challenge for MFIs is greater than for most. Generally speaking, differences in local lifestyle and behavior become more pronounced as one moves down the income ladder. A certain level of income affords a person the opportunity to travel to various places, meet diverse people, learn different languages, and access a variety of information; low income restricts such opportunities. In the process of setting up and overseeing MFIs in three developing countries, I have become keenly aware of the fact that operations in each locale require a different approach to lending, personnel, and other aspects of business in order to succeed.

In short, the expansion of retail banking to other countries requires a deep understanding of local culture and society and an all-out effort to tailor one’s operations and organization accordingly. Unfortunately, larger institutions have shown themselves unwilling or unable to do this. They insist on using the original company name and cling stubbornly to the business practices of their own countries, in many cases installing a management team consisting almost entirely of their own compatriots. This is scarcely a recipe for success.

That financial institutions would find it difficult to unlearn the methods to which they are accustomed is no surprise. Among the traditional strengths of the finance industry are its detailed manuals and policies and its technocratic managers who excel at applying those rules. This breed of manager tends to be very good at getting things done on schedule according to an established blueprint, but they are often less adept at rethinking their business processes from square one.

However, we believe that Gojo is uniquely positioned to break through these structural constraints.

A Gojo, we do not insist that each of our local subsidiaries adopt our name. To begin with, it is totally unnecessary. In addition, such a name change tends to put off the employees of an organization that has changed ownership. Some may even regard it as a mark of neocolonialism. When Gojo expands through mergers or acquisitions, the subsidiaries and partners keep their original names, logos, and local management teams. On the other hand, we spend ample time searching for the kind of partners we can trust to work with hand-in-glove.

Part of my job is to remain on hand as a local management consultant for as long as it takes to get the management of a subsidiary on a secure footing. I worked with the staff in Cambodia for a full year to turn the local office around. In my experience, a typical organization has to solve about 300 problems before it can become a best-practices company. I led some of the problem solving to show how it can be done. The problems I dealt with ranged from such mundane issues as minimizing redundancy and wasted time by monitoring the daily activities of employees to more abstract matters, such as company mission and vision. Together we set to work on all of these issues, and once I saw that the local team was well on their way, I passed the baton.

During this process, I did not ask for rigid adherence to the business principles espoused in industrial economies. However, the one thing I did insist on was creating an organization capable of resolving problems as quickly as possible. My impression is that the world’s best companies share certain basic structural features. All display, in their culture, organization, and personnel, a strong orientation to identifying and analyzing issues, formulating appropriate responses, and sticking with those measures until the issues are solved. I would go so far as to say that a company’s success or failure hinges more than anything on its problem-solving culture and systems.

Another major factor in a “people business” (a business whose success depends largely on the quality of employees) like microfinance is the way its employees interact with the customers. This means that for any MFI, regardless of its location, enhancing employee satisfaction and performance is a key to business success. We place great emphasis on improving employee satisfaction and have instituted a variety of measures toward that end. As a result, the employee turnover for all our subsidiaries combined is about 10%. This is an excellent rate, given that 20%–30% is fairly standard for financial firms in the developing world.

Diversifying our revenue streams by creating new services that leverage our global presence

Businesses in the retail financial sector rely almost entirely on economies of scale to boost profitability. Once a company gets big enough, head-office expenses and system costs become easier to cover, and the profit margin can grow. Securing capital will be facilitated, moreover, if it has deposits on hand from which it can draw funds. In addition, by expanding one’s business internationally, a potential will emerge for economies of scope; there are opportunities that are available only when one has headquarters in a number of different countries. For example:

— Customer data: Most financial institutions have access to reliable customer data from only one country. Gojo is developing its capacity to generate comparable data from multiple countries and will be able to market such data to international organizations and research centers that require it.

— Marketing: In the microfinance industry, local employees typically meet directly with customers once a month to collect payment. It should be possible to use such meetings to conduct market research; for example, product samples can be handed out to customers and, a month later, their opinions and impressions can be collected. Even at our present scale of operations, we could earn tens of thousands of dollars annually by selling data gathered from 300 customers in three countries to Japanese and other makers of consumer products.

— International remittances: At present, transferring funds abroad is both expensive and time consuming, primarily because the financial institutions of different countries use different systems, and linking those systems takes time and money. Gojo can build an integrated system that will allow international remittances to be completed at the same speed and cost as domestic transfers.

— P2P funding platform: While Kiva, Lendahand, and some other companies currently provide platforms for crowdfunding of low-income entrepreneurs, these organizations must spend a huge amount of time and effort compiling information about the businesses that they list on their site, since they have no way of observing them firsthand. With operations in multiple countries and an integrated system, Gojo should be able to build an effective crowdfunding platform with a minimum of effort. This in turn should help us lower the cost of capital compared with traditional MFIs.

Figure 5. Microfinance Business Cost Structures (as percentage of loans outstanding; rough estimate)

In this way, we hope to reduce microfinance interest rates by diversifying revenue streams and lowering the cost of capital. Put simply, in the long run, we want to earn revenue by selling information and collecting other fees instead of depending exclusively on the interest our customers pay us. It will take time to achieve this vision, but I believe that if we begin sowing the seeds now, we can bring these business ideas to fruition one by one.

Future Challenges: Sustained Funding and Human Resources

If Gojo can deploy its current business model worldwide, it will be on its way to helping realize the vision of financial inclusion for all of humanity. Achieving this goal will require no advanced technology—merely the will and creativity to bring it about.

However, two things are essential to the growth of our business going forward: sustained funding and talented personnel to run our local operations.

In the two years since its founding, Gojo has raised $13 million through equity financing. However, to extend our services to 100 million people in 70 countries by 2030, we will need at least $5 billion in capital. Since accumulating this much through earnings alone is unrealistic, we have no choice but to supplement our income through ongoing fundraising efforts. Needless to say, we will also need to raise many times that amount through deposits and loans.

High-caliber human resources are particularly important to a people-oriented business like microfinance. Talented managers are hard to find in any country. We need to create an organization that attracts and nurtures top talent with a commitment to our vision and mission.

Gojo & Company will need to surmount many obstacles to achieve its ambitious goal of creating a private-sector World Bank by 2030. We are committed to the task, though, and are willing to work diligently to achieve our dream of financial inclusion for all.