- Article

- Tax & Social Security Reform

Tokyo Foundation Policy Dialogue on Japanese and US Economic and Tax Policy

November 1, 2017

The Tokyo Foundation hosted a policy dialogue on “ Japanese and US Economic and Tax Policy” on August 2, inviting top economists from the two countries. The following is a summary of the panelists’ presentations, compiled by Senior Fellow Shigeki Morinobu.

* * *

US Tax Reform: Prospects and Roadblocks

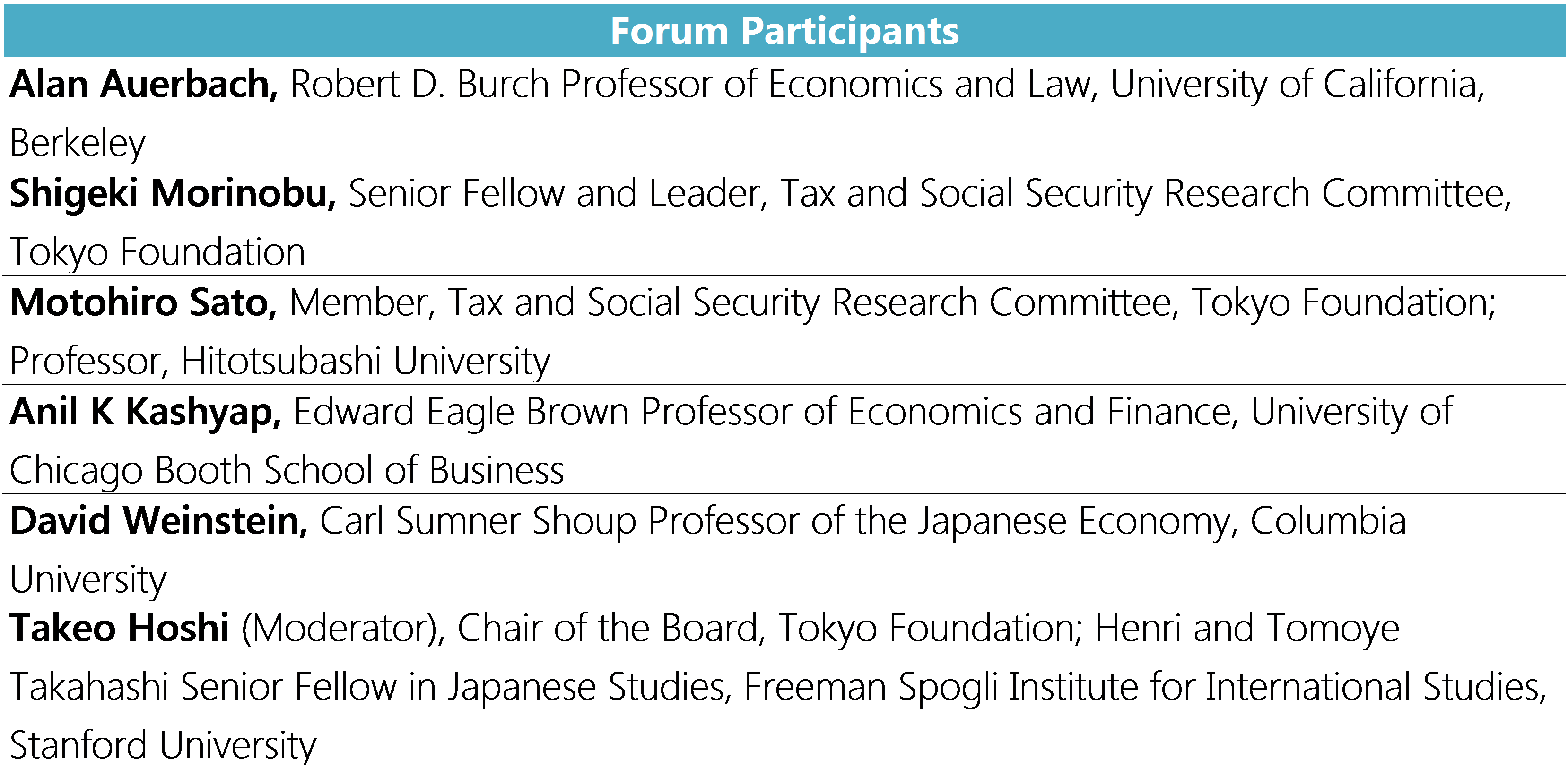

Alan Auerbach

The forum opened with a keynote address (click to read transcript) by Alan Auerbach, the Robert D. Burch professor of economics and law at the University of California, Berkeley. He outlined President Donald Trump’s tax reform plan announced in June, which calls for lowering the highest tax rate for personal income (including business income) from the 39.6% to 35% and slashing corporate taxes from 35% to 15%; shifting from a worldwide taxation system to a territorial system that exempts foreign income; abolishing the inheritance tax; and eliminating various personal income tax deductions. Noticeably missing from the announced reform plan was the implementation of a destination-based cash-flow tax, which was developed by Auerbach and advocated by a number of Republican legislators.

The DBCFT, though, is what the United States really needs. The advantages of this “border adjustment” tax include the fact that (1) companies will be able to immediately deduct the total amount of their capital investments as an expenseーinstead of depreciating such assets over the course of their useful lifeーsince the tax base of the corporate tax will be cash flow; (2) deductions on interest income from corporate tax payments can be eliminated; and (3) the practice of retaining profits in foreign countries with lower tax rates can be prevented, as corporations will be taxed not by where they keep their profits but by where they earn them. The DBCFT is essentially a combination of a subtraction-method value-added tax and a payroll deduction (that is, a tax credit for the social insurance tax) and has been proposed as an alternative to a VAT, whose introduction in the United States has been highly contentious.

Of corporate assets held abroad, the share claimed by intellectual property and other intangible assets has been rising in recent years, and the profits generated by such assets have correspondingly been increasing. Compared to manufacturers, IT companies have an easier time moving operations to different locations. Given the current high corporate tax rate and the worldwide taxation system in place in the United States, many US firms have resorted to corporate inversion strategies to lower their tax burden, resulting in the “lockout” of corporate profits outside the United States.

Many have identified the DBCFT as a solution to these issues, as it lowers the incentive to transfer profits and production offshore, and helps to prevent inversion and the ensuing lockout effect.

There are problems to be overcome, though. One is the concern that the introduction of the DBCFT could trigger changes in the exchange rate, offsetting the benefits of the tax. Another is that certain industries will be adversely affected when deductions on interest income are abolished. From an international perspective, moreover, the anticipated shifting of profits and production back to the United States could have a negative impact on countries that had hitherto been the beneficiaries of corporate inversion, and the European Union has suggested that the border adjustment tax may represent an infringement of World Trade Organization rules. Financial markets, too, are wary of the impact the tax may have on foreign exchange rates.

The Trump administration’s June 27 tax reform plan consequently did not include the DBCFT, and it made no mention of the interest income deductionーa result, no doubt, of confusion in the White House and a hurried response made in the absence of adequate debate.

Keeping the DBCFT off the tax reform plan will leave government without the anticipated increase in tax revenues. If the proposed cuts in corporate taxes are implemented in the absence such new sources of revenue, massive fiscal deficits would result. Thus the reform plan may be on a smaller scale than advertised and implemented on a limited-time basis. This may thus not be the time for a sweeping overhaul of the tax system.

In fact, depending on the results of the 2018 midterm elections, the administration may give up its tax reform plan and focus instead on implementing protectionist tariffs.

Issues in Japan’s Income Tax

Shigeki Morinobu (click to view presentation materials)

The income tax base in Japan is much smaller than in the United Statesーonly about one-half, according to the two countries’ tax statistics. This weakens the tax’s income redistribution function and is a major factor behind the polarization of the middle class. The biggest reason for the small size of Japan’s income tax base is that the pension system is only marginally taxed.

In concrete terms, pension premium payments, along with the investment of funds, are tax-deductible; benefits are also largely untaxed, thanks to generous deductions. The United States employs a payroll tax, so there are no deductions when paying into the system, resulting in a much broader tax base. France and Germany levy a tax on benefits. Taxes on pensions in Japan are the lowest among the industrial democracies; the tax base needs to be broadened so that taxes can play a bigger role in redistributing income, not only between the rich and poor but also between generations. Political courage will be needed to undertake reforms, though, given the prioritization of the interests of the elderly under Japan’s “silver democracy.”

Corporate Income Tax Reform in Japan

Motohiro Sato (click to view presentation materials)

Japan’s corporate tax confronts a changing economic environment brought on by globalization, as nations are now competing with one another to attract corporate investments and assets by slashing their tax rates. Japan has lowered its corporate tax rate to below 30%, but companies are forced to pay two local taxes, which have actually driven up the total corporate tax burden. Japan will thus need to overhaul its system of corporate taxation if it seeks to remain competitive as a destination for business investments.

The cut in the corporate tax rate was accompanied by an enhancement of the pro forma taxation standard. While both the pro forma taxーbased on a company’s size rather than earningsーand the consumption tax are value-added taxes, the former applies only to large businesses and is more distortive. It would be a better idea to turn it into a local consumption tax that is levied on all companies. R&D tax incentives, too, need to be reexamined, as multinationals resort to “cherry picking” behavior, undertaking R&D in countries with the most generous incentives. The Trump tax plan includes an overhaul of the corporate tax; it may be time for Japan, too, to consider revising the tax base, such as by shifting the focus of corporate tax from income to cash flow.

Trump’s Tax Reform Plan

Anil K Kashyap of the University of Chicago noted that the White House is seriously short-staffed, preventing it from communicating effectively with members of Congress and thwarting efforts to implement comprehensive tax reforms. He believed that the Trump tax reform proposal would consequently turn out to be rather fragmented, consisting largely of repealing or lowering the alternative minimum tax.

David Weinstein of Columbia University added that the US administration is in a state of chaos and that the business community is growing uneasy about the direction of tax reform. The introduction of a destination-based cash-flow tax would deal a blow to importers but be a boon for exporters. While its impact may be adjusted over time through currency fluctuations, there is no telling how long this will actually takeー3 years, 5 years, or even 10 yearsーand this uncertainty is fueling uneasiness in the corporate sector.

Exchange Rate Fluctuations

During the Q&A session, a questioner raised the point that the introduction of a DBCFTーat a rate of 20%ーmay trigger exchange rate adjustment of as much as 25% and largely offset any benefits of the tax. Auerbach replied that there was general consensus among economists that the DBCFT would have an impact on foreign exchange rates but that there was disagreement on the extent of the adjustment, adding that he himself believed that such adjustments would end within five years.

On the question of whether Trump’s tax cut plan is likely to be coupled with such measures as the elimination of tax breaks to make up for lost revenue, the Berkeley economist said that such efforts at revenue neutrality and fiscal responsibility were unlikely. With midterm elections coming up in 2018, some legislators with Tea Party backing may object to what will likely lead to a bigger federal deficit, but such criticism is expected to be limited.

As to how Congress will respond to Trump’s protectionist trade policy, Weinstein recalled that while Republicans have traditionally advocated free trade, trade friction between Japan and the United States was at its peak during Republican administrations. There is no telling, therefore, whether a Republican-controlled Congress would effectively stop the White House from implementing protectionist measures.

The policy dialogue with Auerbach and other leading US economists left the author with the impression that a border adjustment tax (which is levied on imports but not on exports) requires a broad institutional framework. Japan’s consumption tax is border adjusted by customs officials, who painstakingly either collect duties on imports or refund the amount charged on exports under a licensing system. Were the United States to adopt a DBCFT, it would need to establish a similar system.

Another important point is the need to patiently and persuasively explain to consumers and businesses how the tax burden would shift under a border adjustment tax. Inasmuch as it is a value-added-tax, an invoice system would be needed to smoothly transfer the tax burden at each transaction stage until it is ultimately borne by the consumer.

The debate over whether or not the DBCFT is an infringement of WTO rules is likely to focus on imports, rather than exports. The WTO stipulates that domestic taxesーlevied either directly or indirectlyーon imports must not be higher than those applied to comparable items produced domestically. While domestic products would be subject to the DBCFT as well, the price of imports includes the cost of labor, which, in the case of domestically produced items, can be written off. Might this be regarded as a contravention of the rule prohibiting discriminatory taxation? In the United States, no distinction is made between direct and indirect taxes; rather, taxes are either on income or consumption. This fact further obscures the question of whether or not the DBCFT is consistent with WTO provisions.

-

- Robert D. Burch Professor of Economics and Law, University of California, Berkeley

- Alan J. Auerbach

- Alan J. Auerbach

-

-

- RESEARCH DIRECTOR

- Shigeki Morinobu

- Shigeki Morinobu

- Areas of Expertise

-

- Tax and fiscal policy

- local finances

- Research Program

-

- The History of Japan’s Consumption Tax: An Archive of Key Events and Documents ( –2021)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan (2021–2022)

- Digitalization of the Economy and International Taxation(-2024)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan 2

-

-

-

- RESEARCH DIRECTOR

- Motohiro Sato

- Motohiro Sato

- Areas of Expertise

-

- Local public finance

- Optimal taxation theory, tax reform

- Social security, health economics

-

-

- Edward Eagle Brown Professor of Economics and Finance, Booth School of Business, University of Chicago

- Anil K Kashyap

- Anil K Kashyap

-

- Carl S. Shoup Professor of the Japanese Economy, Columbia University

- David E. Weinstein

- David E. Weinstein

-

- Chair of the Board, Tokyo Foundation

- Takeo Hoshi

- Takeo Hoshi

Featured Content

-

Funding the Policies to Boost Japan’s Birthrate

Funding the Policies to Boost Japan’s Birthrate

-

CSR in Japan: Unique Features and Recent Trends

CSR in Japan: Unique Features and Recent Trends

-

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

-

Japanese Honeybee

Japanese Honeybee

-

Democracy in Crisis: Lessons from Japanese History

Democracy in Crisis: Lessons from Japanese History